I like to end each week taking a look at the upcoming week’s economic calendar just to have an idea of what kind of curveballs may come along. It’s a fairly low value added activity as once you know what is in store for the coming week the best you can do is guess about data releases and then further guess about market reactions.

I like to end each week taking a look at the upcoming week’s economic calendar just to have an idea of what kind of curveballs may come along. It’s a fairly low value added activity as once you know what is in store for the coming week the best you can do is guess about data releases and then further guess about market reactions.

Just like the professionals.

That’s an even less productive endeavor in August and this summer we don’t even have much in the way of extrinsic factors, such as a European banking crisis to keep us occupied in our guessing. In all, there have been very few catalysts and distractions of late, hearkening back to more simple times when basic rules actually ruled.

In the vacuum that is August you might believe that markets would be inclined to respond to good old fundamentals as histrionics takes a vacation. Traditionally, that would mean that earnings take center stage and that the reverse psychology kind of thinking that attempts to interpret good news as bad and bad news as good also takes a break.

Based upon this most recent earnings season it’s hard to say that the market has fully embraced traditional drivers, however. While analysts are mixed in their overall assessment of earnings and their quality, what is clear is that earnings don’t appear to be reflective of an improving economy, despite official economic data that may be suggesting that is our direction.

That, of course, might lead you to believe that discordant earnings would put price pressure on a market that has seemingly been defying gravity.

Other than a brief and shallow three day drop this week and a very quickly corrected drop in May, the market has been incredibly resistant to broadly interpreting earnings related news negatively, although individual stocks may bear the burden of disappointing earnings, especially after steep runs higher.

But who knows, maybe Friday’s sell off, which itself is counter to the typical Friday pattern of late is a return to rational thought processes.

Despite mounting pessimism in the wake of what was being treated as an unprecedented three days lower, the market was able to find catalysts, albeit of questionable veracity, on Thursday.

First, news of better than expected economic growth in China was just the thing to reverse course on the fourth day. For me, whose 2013 thesis was predicated on better than expected Chinese growth resulting from new political leadership’s need to placate an increasingly restive and entitled society, that kind of news was long overdue, but nowhere near enough to erase some punishing declines in the likes of Cliffs Natural Resources (CLF).

That catalyst lasted for all of an hour.

The real surprising catalyst at 11:56 AM was news that JC Penney (JCP) was on the verge of bringing legendary retail maven Allen Questrom back home at the urging of a newly vocal Bill Ackman. The market, which had gone negative and was sinking lower turned around coincident with that news. Bill Ackman helped to raise share price by being Bill Ackman.

Strange catalyst, but it is August, after all. In a world where sharks can fall out of the sky why couldn’t JC Penney exert its influence, especially as we’re told how volatile markets can be in a light volume environment? Of course that bump only lasted about a day as shares went down because Bill Ackman acted like Bill Ackman.The ensuing dysfunction evident on Friday and price reversal in shares was, perhaps coincidentally mirrored in the overall market, as there really was no other news to account for any movement of stature.

With earnings season nearly done and most high profile companies having reported, there’s very little ahead, just more light volume days. As a covered option investor if I could script a market my preference would actually be for precisely the kind of market we have recently been seeing. The lack of commitment in either direction or the meandering around a narrow range is absolutely ideal, especially utilizing short term contracts. That kind of market present throughout 2011 and for a large part of 2012 has largely been missing this year and sorely missed. Beyond that, a drop on Fridays makes bargains potentially available on Mondays when cash from assigned positions is available.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend and Momentum, with no “PEE” selections this week. (see details).

For an extended period I’ve been attempting to select new positions that were soon to go ex-dividend as a means to increase income, offset lower option premiums and reduce risk, while waiting for a market decline that has never arrived.

This week, I’m more focused on the two selections that are going ex-dividend this coming week, but may have gotten away after large price rises on Thursday.

Both Cliffs Natural Resources and Microsoft (MSFT) were beneficiaries of Chinese related news. In Cliffs Natural’s case it was simply the perception that better economic news from China would translate into the need for iron ore. In Microsoft’s case is was the introduction of Microsoft Office 365 in China. Unfortunately, both stocks advanced mightily on the news, but any pullback prior to the ex-dividend dates would encourage me to add shares, even in highly volatile Cliffs, with which I have suffered since the dividend was slashed.

A bit more reliable in terms of dividend payments are Walgreens (WAG), Chevron (CVX) and Phillips 66 (PSX).

Although I do like Walgreens, I’ve only owned it infrequently. However, since beginning to offer weekly options I look more frequently to the possibility of adding shares. Despite being near its high, the prospect of a short term trade in a sector that has been middling over the past week, with a return amplified by a dividend payment, is appealing.

Despite being near the limit of the amount of exposure that I would ordinarily want in the Energy Sector, both Chevron and Phillips 66 offer good option premiums and dividends. The recent weakness in big oil makes me gravitate toward one of its members, Chevron, however, if forced to choose between just one to add to my portfolio, I prefer Phillips 66 due to its greater volatility and enhanced premiums. I currently own Phillips 66 shares but have them covered with September call contracts. In the event that I add shares I would likely elect weekly hedge contracts.

If there is some validity to the idea that the Chinese economy still has some life left in it, Joy Global (JOY), which is currently trading near the bottom of its range offers an opportunity to thrive along with the economy. Although the sector has been relatively battered compared to the overall market, option premiums and dividends have helped to close that gap and I believe that the sector is beginning to resemble a compressed spring. On a day when Deere (DE) received a downgrade and Caterpillar was unable to extend its gain from the previous day, Joy Global moved strongly higher on Friday in an otherwise weak market.

Oracle (ORCL) is one of the few remaining to have yet reported its earnings and there will be lots of anticipation and perhaps frayed nerves in advanced for next month’s report, which occurs the day prior to expiration of the September 2013 contract.

You probably don’t need the arrows in the graph above to know when those past two earnings reports occurred. Based Larry Ellison’s reaction and finger pointing the performance issues were unique to Oracle and one could reasonably expect that internal changes have been made and in place long enough to show their mark.

Fastenal (FAST) is just a great reflection of what is really going on in the economy, as it supplies all of those little things that go into big things. Without passing judgment on which direction the economy is heading, Fastenal has recently seemed to established a lower boundary on its trading range after having reported some disappointing earnings and guidance. Trading within a defined range makes it a very good candidate to consider for a covered option strategy

What’s a week without another concern about legal proceedings or an SEC investigation into the antics over at JP Morgan Chase (JPM)? While John Gotti may have been known as the “Teflon Don,” eventually after enough was thrown at him some things began to stick. I don’t know if the same fate will befall Jamie Dimon, but he has certainly had a well challenged Teflon shell. Certainly one never knows to what degree stock price will be adversely impacted, but I look at the most recent challenge as just an opportunity to purchase shares for short term ownership at a lower price than would have been available without any legal overhangs.

Morgan Stanley (MS), while trading near its multi-year high and said to have greater European exposure than other US banks, continues to move forward, periodically successfully testing its price support.

With any price weakness in JP Morgan or Morgan Stanley to open the week I would be inclined to add both, as I’ve been woefully under-invested in the Finance sector recently.

While retailers, especially teen retailers had a rough week last week, Footlocker (FL) has been a steady performer over the past year. A downgrade by Goldman Sachs (GS) on Friday was all the impetus I needed and actually purchased shares on Friday, jumping the gun a bit.

Using the lens of a covered option seller a narrow range can be far more rewarding than the typical swings seen among so many stocks that lead to evaporation of paper gains and too many instances of buying high and selling low. Some pricing pressure was placed on shares as its new CEO was rumored a potential candidate for the CEO at JC Penney. However, as that soap opera heats up, with the board re-affirming its support of their one time CEO and now interim CEO, I suspect that after still being in limbo over poaching Martha Stewart products, JC Penney will not likely further go where it’s unwelcome.

Finally, Mosaic (MOS) had a good week after having plunged the prior week, caught up in the news that the potash cartel was falling apart. Estimates that potash prices may fall by 25% caused an immediate price drop that offered opportunity as basically the fear generated was based on supposition and convenient disregard for existing contracts and the potential for more rationale explorations of self-interest that would best be found by keeping the cartel intact.

The price drop in Mosaic was reminiscent of that seen by McGraw Hill FInancial (MHFI) when it was announced that it was the target of government legal proceedings for its role in the housing crisis through its bond ratings. The drop was precipitous, but the climb back wonderfully steady.

I subsequently had Mosaic shares assigned in the past two weeks, but continue to hold far more expensively priced shares. I believe that the initial reaction was so over-blown that even with this past week’s move higher there is still more ahead, or at least some price stability, making covered options a good way to generate return and in my case help to whittle down paper losses on the older positions while awaiting some return to normalcy.

Traditional Stocks: Fastenal, Footlocker, JP Morgan, Morgan Stanley, Oracle

Momentum Stocks: Joy Global, Mosaic

Double Dip Dividend: Chevron (ex-div 8/15), Phillips 66 (ex-div 8/14), Walgreen (ex-div 8/16)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may be become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The over-riding objective is to create a healthy income stream for the week with reduction of trading risk.

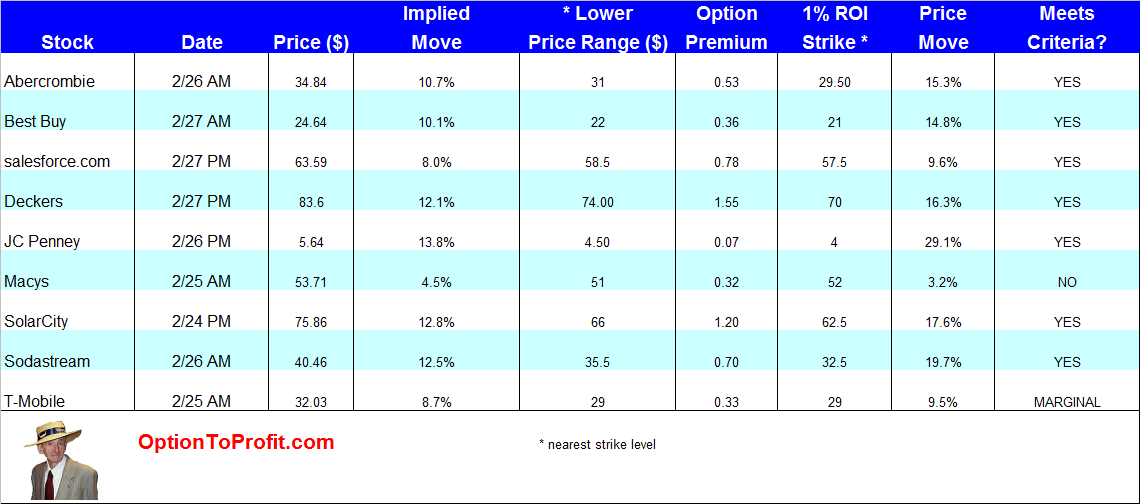

While most of the more meaningful companies in the S&P 500 have already reported earnings and new earnings season is barely 7 weeks away, there’s still time to profit from remaining earnings reports coming this week.

While most of the more meaningful companies in the S&P 500 have already reported earnings and new earnings season is barely 7 weeks away, there’s still time to profit from remaining earnings reports coming this week. The table may be used as a guide for determining which of these selected companies meet the risk-reward parameters that an individual sets, understanding that re-assessments need to be made as prices and, therefore, strike prices and their premiums may change.

The table may be used as a guide for determining which of these selected companies meet the risk-reward parameters that an individual sets, understanding that re-assessments need to be made as prices and, therefore, strike prices and their premiums may change. Things aren’t always as they seem.

Things aren’t always as they seem. Generally, when you hear the words “perfect storm,” you tend to think of an unfortunate alignment of events that brings along some tragedy. While any of the events could have created its own tragedy the collusion results in something of enormous scale.

Generally, when you hear the words “perfect storm,” you tend to think of an unfortunate alignment of events that brings along some tragedy. While any of the events could have created its own tragedy the collusion results in something of enormous scale.

To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.

To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.