It’s said that George Eastman, founder of Eastman Kodak (EKDKQ), was quite methodical as he approached the end of his life and was prepared to put his escape plan into action.

It’s said that George Eastman, founder of Eastman Kodak (EKDKQ), was quite methodical as he approached the end of his life and was prepared to put his escape plan into action.

“My work here is done” may be a very logical way to approach any kind of transition, although it doesn’t have to be taken to the extreme that Eastman felt was appropriate under his circumstances. Be prepared, but don’t be crazy.

I’ve been transitioning a portfolio for almost a month in anticipation of the market taking a break and perhaps giving back some of its gains; maybe even a lot of its gains.

Doing so has made me much less fun to be around, but circumstances do change and being prepared for plausible scenarios means having exit strategies and surviving to see them do as planned until it’s time to exit the exit strategy. Once my work is done I can’t wait to get back to work.

I for one was glad to see the first quarter of 2013 come to an end. Fortunately, as a covered option seller, my remaining life span may not be sufficient to see another opening yearly quarter such as this past one, as the last such period was in 1987.

You may or may not remember how that year ended, but let’s just say that a single day 500 point drop back then was a lot more meaningful than it would be today.

I wasn’t prepared back then, in fact, that was the last time I used a margin account. I may end up being wrong this time around, but in watching markets for a number of years, both as a casual observer and as an active participant it’s reasonably clear that the good times don’t just keep rolling.

Selling covered calls is a great strategy when applied methodically, but it does meet its match in markets that just do nothing other than going higher. Hopefully April will usher in some greater variety in outcomes, as the past few weeks, despite having established records in both the Dow Jones and S&P 500 have been showing some signs of tentative behavior.

Part of being a less fun person has meant initiating fewer new positions each week. The first step to creating an environment that wouldn’t entice me to spend money on new positions was to cut off the funding just like you might with any addict. Luckily, most stock traders won’t resort to petty crime and pawning the belongings of loved ones to feed the habit, although that margin account can be very appealing and the answer to an easy fix.

I cut off my flow of funds by moving from weekly to extended weekly or monthly options. Longer contracts means less weekly contracts available to be assigned and less opportunity for new weekly cash to be available to “feed the beast.”.

Unfortunately, I also curtailed my cash flow by some unseemly timing in the purchase of new positions this past quarter, such as Petrobras (PBR) and Cliffs Natural Resources (CLF) that are sitting awaiting opportunities to have call contracts written against them.

The next part of the transition was focusing on reliable dividend paying stocks. The kind your grandfather would feel comfortable owning. Last week, all new positions went ex-dividend last week or this coming week. They’re not very exciting to own, but dividends, especially when their ensuing share price reduction is partially offset by option premiums are especially welcome.

Keeping more cash in reserve, moving away from “Momentum” positions, longer contracts and seeking near term dividends is the exit strategy and my transition is nearly complete.

Now comes the waiting and the period of self-doubt, which includes wondering when it’s time to abandon a thesis. In the meantime, increasing cash reserves doesn’t mean a total prohibition against finding potential new opportunities. After all, being prepared doesn’t have to take you to extremes. Once you’ve reached a crazy state of preparedness it’s hard to turn around to see the light.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend or Momentum categories, with no selections in the “PEE” category, as earnings season begins anew on April 8, 2013 (see details). Additionally, as in previous weeks there is a greater emphasis on stocks that offer monthly contracts only, eschewing the usual preference for the relatively higher ROI of weekly options for the guarantee of premiums for a longer period in order to ride out any turbulence.

Some of this week’s selections are stocks that I already own but may consider adding to existing positions. One such stock is Deere (DE) which left me somewhat exasperated this past Thursday, the final day of a holiday shortened trading week.

At almost precisely noon shares of Deere dropped by about $1.40 in about 8 minutes, taking it from the realm of stocks poised for assignment. The plunge happened while the market was stable and most other heavy machinery and equipment makers were actually going higher. There was no news to account for the sudden and sustained drop. Neither in real time nor hours after.

Caterpillar (CAT) is one of the stocks that has an ignominious reputation during this record setting quarter. It was among the worst performers of the quarter and was routinely tagged as a laggard on those days that the broad market performed well. I recently purchased shares having waited all quarter for them to reach the price point that was very kind to me in 2012. It accompanied Deere for a small portion of the former’s inexplicable retreat but recovered sufficiently to avoid being tagged yet again.

Bristol Myers Squibb (BMY) and Medtronic (MDT) fit into two ongoing themes. Looking for near term dividend paying shares and belonging to the broadly defined healthcare sector. While healthcare has been the leading sector for the trailing year, I think there are still short term opportunities, even with a specter of a declining market. While both Bristol Myers and Medtronic have had significant advances lately, the combination of dividend and premium continue to make it appealing.

MetLife (MET), also a recent holding, fits into my broad definition of “healthcare” if you stretch that definition to an extreme. Part of my positive outlook for its shares is related to what I believe will be growth in its home insurance business. Of course, I rarely think in terms of fundamentals and certainly don’t have a long term perspective on its shares, but it is well positioned to maintain price stability even in a stock market of reduced stability.

Wells Fargo (WFC) and JP Morgan (JPM) are two very different banks. JP Morgan goes ex-dividend this week and has been beleaguered with domestic attacks from elected officials and international attacks as Cyprus may or may not add risk to global banks, such as JP Morgan.

On the other hand, Wells Fargo is as pure of a domestic play as you can find at a size that still makes it “too big to fail.” With news of improving real estate sales all over the country the Wells Fargo money machine is poised to re-create the glory days that so abruptly ended 5 years ago.

I’ve been looking for an excuse to purchase Lowes (LOW) for the past few weeks and have watched its price show some mild erosion during that time

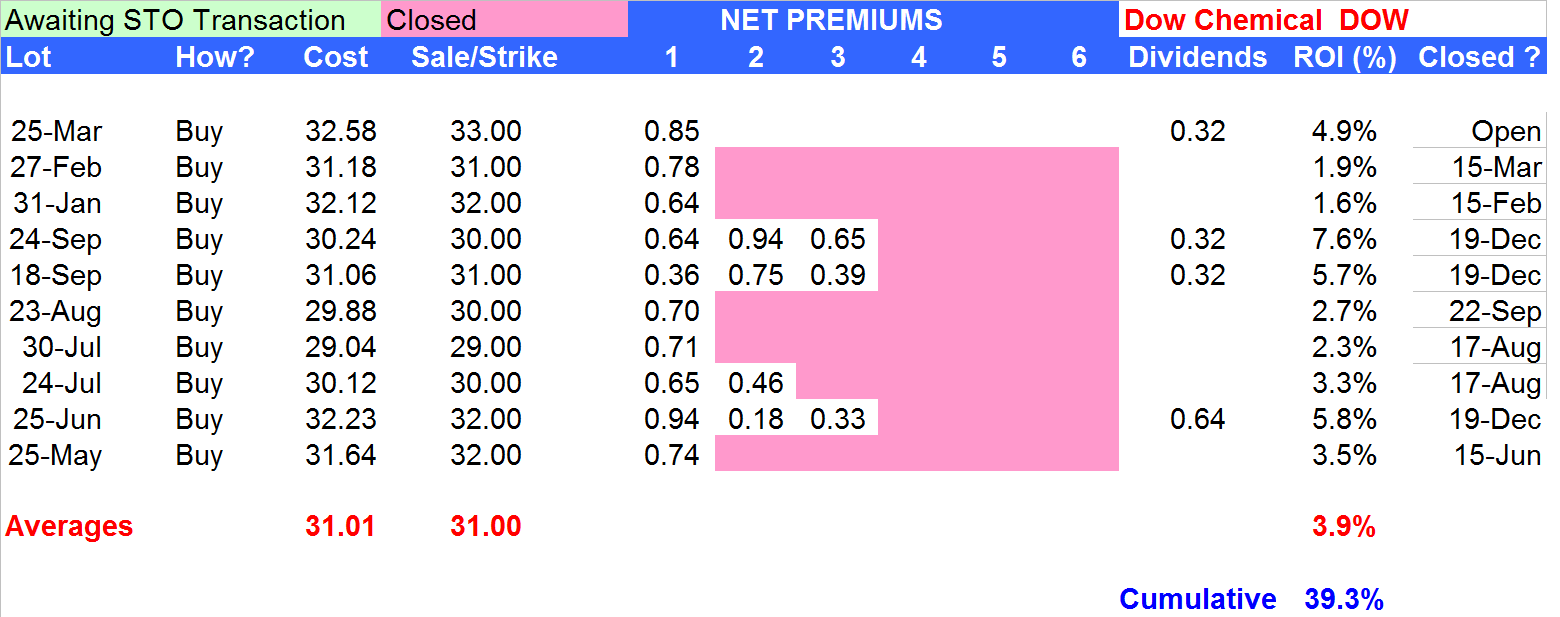

Dow Chemical (DOW) has been one of my favorite stocks for a long time. I purchased additional shares last week to capture its dividend and after looking at its performance over the past 10 months feel guilty thinking that it’s a “boring” stock.

Dow Chemical (DOW) has been one of my favorite stocks for a long time. I purchased additional shares last week to capture its dividend and after looking at its performance over the past 10 months feel guilty thinking that it’s a “boring” stock.

In fact, it’s been absolutely the poster child for what makes a covered call strategy a successful one. While its stock price has virtually remained unchanged since May 2012, the active cycle of buying shares, selling calls, assignment, buy shares, etc.. has resulted in a nearly 40% ROI.

Finally, Western Refining (WNR) is a company whose shares I briefly owned recently at a much lower price. It was one that got away during the uni-directional market of the first quarter. Its price has come down a bit and I think may now be at its “new normal” making it perhaps an antidote to Petrobras in a sector that has some catching up to do.

Traditional Stocks: Caterpillar, Deere, Dow Chemical, JP Morgan, Lowes, MetLife, Wells Fargo

Momentum Stocks: Western Refining

Double Dip Dividend: Bristol Myers (ex-div 4/3), JP Morgan (ex-div 4/3), Medtronic (ex-div 4/3)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Some of the stocks mentioned in this article may be viewed for their past performance utilizing the Option to Profit strategy.