To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.

To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.

This was an interesting week.

It started with the always interesting CEO of Overstock.com (OSTK) congratulating Steve Cohen, the CEO of SAC Capital, on his SEC indictment and invoking a reference to Star Wars to describe Cohen’s darkness, at least in Patrick Byrne’s estimations.

It ended with The New York Post, a one time legitimate newspaper suggesting that JC Penney (JCP) had lost the support of CIT (CIT), the largest commercial lender in the apparel industry, which is lead by the charisma challenged past CEO of The NYSE (NYX) and Merrill Lynch, who reportedly knows credit risk as much as he knows outrageously expensive waiting room and office furniture.

The problem is that if CIT isn’t willing to float the money to vendors who supply JC Penney, their wares won’t find their way into stores. Consumers like their shopping trips to take place in stores that actually have merchandise.

At about 3:18 PM the carnage on JC Penney’s stock began, taking it from a gain for the day to a deep loss on very heavy volume, approximately triple that of most other days.

Lots of people lost lots of money as they fled for the doors in that 42 minute span, despite the recent stamp of approval that George Soros gave to JC Penney shares. His money may not have been smart enough in the face of yellow journalism fear induced selling.

The very next morning a JC Penney spokesperson called the New York Post article “untrue.” It would have helped if someone from CIT chimed in and set the record straight. While the volume following the denial was equally heavy, very little of the damage was undone. As an owner of shares, Thane’s charisma would have taken an incredible jump had he added clarity to the situation.

So someone is lying, but it’s very unlikely that there will ever be a price to be paid for having done so. Clearly, either the New York Post is correct or JC Penney is correct, but only the New York Post can hide behind journalistic license. In fact, it would be wholly irresponsible to accuse the article of promoting lies, rather it may have recklessly published unfounded rumors.

By the same token, if the JC Penney response misrepresents the reality and is the basis by which individuals chose not to liquidate holdings, the word “criminal” comes to my mind. I suppose that JC Penney could decide to create a “Prison within a Store” concept, if absolutely necessary, so that everyday activities aren’t interrupted.

For the conspiracy minded the publication of an article in a “reputable” newspaper in the final hour of trading, using the traditional “unnamed sources” is problematic and certainly invokes thoughts of the very short sellers demonized by Patrick Byrne in years past.

Oh, and in between was the release of the FOMC meeting minutes, which produced a big yawn, as was widely expected.

I certainly am not one to suggest that Patrick Byrne has been a fountain of rational thought, however, it does seem that the SEC could do a better job in allaying investor concerns about an unlevel playing field or attempts to manipulate markets. Equally important is a need to publicly address concerns that arise related to unusual trading activity in certain markets, particularly options, that seem to occur in advance of what would otherwise be unforeseen circumstances. Timing and magnitude may in and of themselves not indicate wrongdoing, but they may warrant acknowledgement for an investing public wary of the process. A jury victory against Fabrice Tourre for fraud is not the sort of thing that the public is really looking for to reinforce confidence in the process, as most have little to no direct interaction with Goldman Sachs (GS). They are far more concerned with mundane issues that seem to occur with frequency.

Perhaps the answer is not closer scrutiny and prosecution of more than just high profile individuals. Perhaps the answer is to let anyone say anything and on any medium, reserving the truth for earnings and other SEC mandated filings. Let the rumors flow wildly, let CEOs speak off the top of their heads even during “quiet periods” and let the investor beware. By still demanding truth in filings we would still be at least one step ahead of China.

My guess is that with a deluge of potential misinformation we will learn to simply block it all out of our own consciousness and ignore the need to have reflexive reaction due to fear or fear of missing out. In a world of rampantly flying rumors the appearance of an on-line New York Post article would likely not have out-sized impact.

Who knows, that might even prompt a return to the assessment of fundamentals and maybe even return us to a day when paradoxical thought processes no longer are used to interpret data, such that good news is actually finally interpreted as good news.

I conveniently left out the monthly Employment Situation Report that really ended the week, but as with ADP and the FOMC, expectations had already been set and reaction was muted when no surprises were in store. The real surprise was the lack of reaction to mildly disappointing numbers, perhaps indicating that we’re over the fear of the known.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories. (see details).

One of last week’s earnings related selections played true to form and dropped decidedly after earnings were released. Coach (COH) rarely disappoints in its ability to display significant moves in either direction after earnings and in this case, the disappointment was just shy of the $52.50 strike price at which I had sold weekly puts. However, with the week now done and at its new lower price, I think Coach represents a good entry point for new shares. With its newest competitor, at least in the hearts of stock investors, Michael Kors (KORS) reporting earnings this week there is a chance that Coach may drop if Kors reports better than expected numbers, as the expectation will be that it had done so at Coach’s expense. For that reason I might consider waiting until Tuesday morning before deciding whether to add Coach to the portfolio.

Although I currently own two higher priced lots of its shares, I purchased additional shares of Mosaic (MOS) after the plunge last week when perhaps the least known cartel in the world was poised for a break-up. While most people understand that the first rule of Cartel Club is that no one leaves Cartel Club, apparently that came as news to at least one member. The shares that I purchased last week were assigned, but I believe that there is still quite a bit near term upside at these depressed prices. While theories abound, such as decreased fertilizer prices will lead to more purchases of heavy machinery, I’ll stick to the belief that lower fertilizer prices will lead to greater fertilizer sales and more revenue than current models might suggest.

Barclays (BCS) is emblematic of what US banks went through a few years ago. The European continent is coming to grips with the realization that greater capitalization of its banking system is needed. Barclays got punished twice last week. First for suggesting that it might initiate a secondary offering to raise cash and then actually releasing the news of an offering far larger than most had expected. Those bits of bad news may be good news for those that missed the very recent run from these same levels to nearly $20. Shares will also pay a modest dividend during the August 2013 option cycle, but not enough to chase shares just for the dividend.

Royal Dutch Shell (RDS.A) released its earnings this past Thursday and the market found nothing to commend. On the other hand the price drop was appealing to me, as it’s not every day that you see a 5% price drop in a company of this caliber. For your troubles it is also likely to be ex-dividend during the August 2013 option cycle. While there is still perhaps 8% downside to meet its 2 year low, I don’t think that will be terribly likely in the near term. Big oil has a way of thriving, especially if we’re at the brink of economic expansion.

Safeway (SWY) recently announced the divestiture of its Canadian holdings. As it did so shares surged wildly in the after hours. I remember that because it was one of the stocks that I was planning to recommend for the coming week and then thought that it was a missed opportunity. However, by the time the market opened the next morning most of the gains evaporated and its shares remained a Double Dip Dividend selection. While its shares are a bit higher than where I most recently had been assigned it still appears to be a good value proposition.

Baxter International (BAX) recently beat earnings estimates but wasn’t shown too much love from investors for its efforts. I look at it as an opportunity to repurchase shares at a price lower than I would have expected, although still higher than the $70 at which my most recent shares were assigned. In this case, with a dividend due early in September, I might consider a September 17, 2013 option contract, even though weekly and extended weekly options are available.

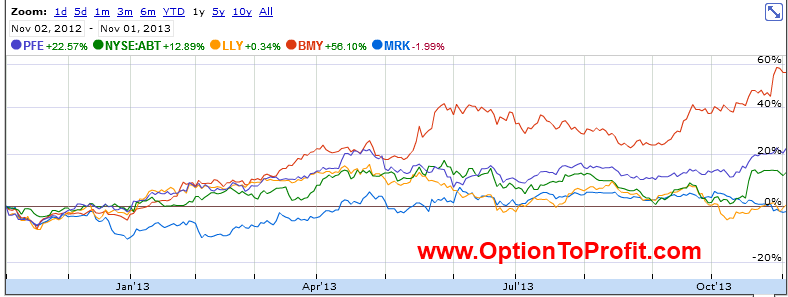

I currently own shares of Pfizer (PFE), Abbott Labs (ABT) and Eli Lilly (LLY) in addition to Merck (MRK), so I tread a little gingerly when considering adding either more shares of Merck or a new position in Bristol Myers Squibb (BMY), while I keep an eye of the need to remain diversified. Both of those, however, have traded well in their current price range and offer the kind of premium, dividend opportunity and liquidity that I like to see when considering covered call related purchases. As with Baxter, in the case of Merck I might consider selling September options because of the upcoming dividend.

Of course, to balance all of those wonderful healthcare related stocks, following its recent price weakness, I may be ready to add more shares of Lorillard (LO) which have recently shown some weakness. The last time its shares showed some weakness I decided to sell longer term call contracts that currently expire in September and also allow greater chance of also capturing a very healthy dividend. As with some other selections this month the September contract may have additional appeal due to the dividend and offers a way to collect a reasonable premium and perhaps some capital gains while counting the days.

Finally, Green Mountain Coffee Roasters (GMCR) is a repeat of last week’s earnings related selection. I did not sell puts in anticipation of the August 7, 2013 earnings report as I thought that I might, instead selecting Coach and Riverbed Technology (RVBD) as earnings related trades. Inexplicably, Green Mountain shares rose even higher during that past week, which would have been ideal in the event of a put sale.

However, it’s still not to late to look for a strike price that is beyond the 13% implied move and yet offers a meaningful premium. I think that “sweet spot” exists at the $62.50 strike level for the weekly put option. Even with a 20% drop the sale of puts at that level can return 1.1% for the week.

The announcement on Friday afternoon that the SEC was charging a former Green Mountain low level employee with insider trading violations was at least a nice cap to the week, especially if there’s a lot more to come.

Traditional Stocks: Barclays, Baxter International, Bristol Myers Squibb, Lorillard, Merck, Royal Dutch Shell, Safeway

Momentum Stocks: Coach, Mosaic

Double Dip Dividend: Barclays (ex-div 8/7)

Premiums Enhanced by Earnings: Green Mountain Coffee Roasters (8/7 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Trying to listen to the President put forth some statistics regarding the employment situation in the United States this past week was difficult, as my attention was captured by the festive holiday backdrop.

Trying to listen to the President put forth some statistics regarding the employment situation in the United States this past week was difficult, as my attention was captured by the festive holiday backdrop.

Some things are just unappreciated until they’re gone.

Some things are just unappreciated until they’re gone.