Jan232015

Jul272014

More and More Earnings

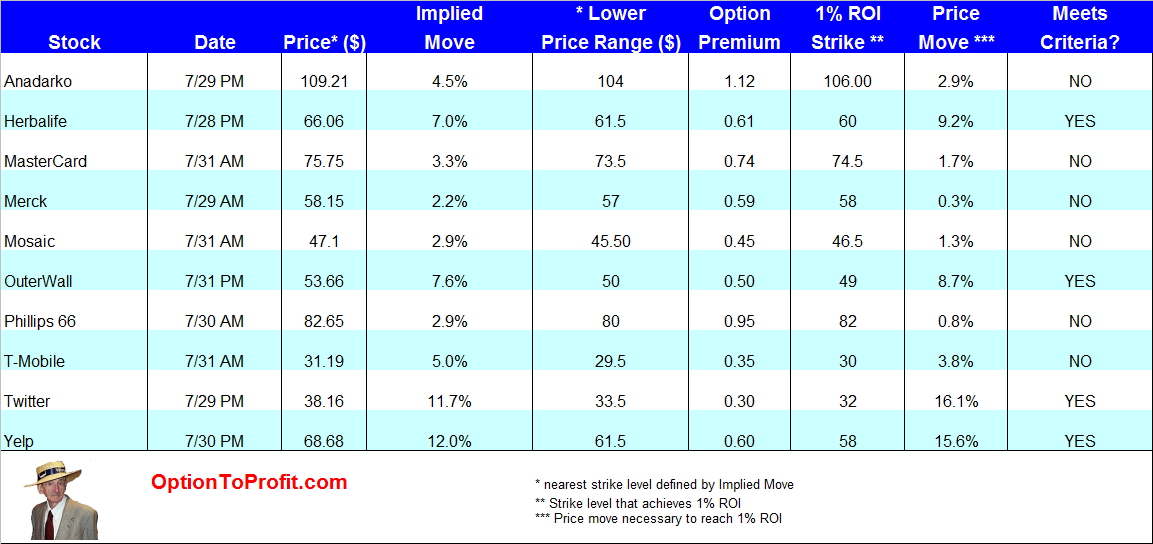

After last week’s deluge of 150 of the S&P 500 companies reporting their earnings this week is a relatively calm one.

For all of its gyrations last week, including the sell-off on Friday, if you simply looked at the market’s net change you would have thought that it was a quiet week as well.

The initial week of earnings season did see seem promise coming from the financial sector. Last week was a mixed one, as names such as Facebook (FB) and Amazon (AMZN) went in very different directions and the initial responses to earnings didn’t necessarily match the final result, such as in the case of NetFlix (NFLX).

While some of the sell-off on Friday may be attributed to the announcement of additional European Council sanctions against Russia and perhaps even the late in the session downgrade of stocks and bonds by Goldman Sachs (GS), earnings had gotten most of the week’s attention.

The coming week offers another opportunity to consider potential trades that can profit regardless of the direction of share price movements, as long as they stay reasonably close to the option market’s predictions of their trading range in response to those reports.

In line with my own tolerance for risk and my own definition of what constitutes a suitable reward for the risk, I prefer the consideration of trades that can return at least 1% for the sale of a weekly put option at a strike level that is below the lower boundary defined by the option market’s assessment. Obviously, everyone’s risk-reward profile differs, but I believe that consistent application or standardizing criteria by individual investors is part of a discipline that can make such trades less anxiety provoking and less tied to emotional factors.

Occasionally, I will consider the outright purchase of shares and the sale of calls, rather than the sale of puts for such trades, but that is usually the case if there is also the consideration of an upcoming ex-dividend date, such as will be the case with Phillips 66 (PSX). Additionally, doing so would most likely be done if I had no hesitancy regarding the ownership of shares. In contrast, often when I sell puts I have no real interest in owning the shares and would much prefer expiration or the ability to roll over those contracts if assignment appeared likely.

This coming week there again appear to be a number of stocks deserving attention as the reward may be well suited to the level of risk, thanks to the option premiums that are enhanced before earnings are released.

As often is the case the stocks that are most likely to be able to deliver a 1% or greater premium at a strike level outside of the implied move range are already volatile stocks, whose volatility is even greater in response to earnings. While at first glance an implied move of 12%, as is the case for Yelp (YELP) may seem unusually large, past history shows that concerns for moves of that magnitude are warranted.

Among the companies that I am considering this coming week are Anadarko (APC), Herbalife (HLF), MasterCard (MA), Mosaic (MOS), Merck (MRK), Outerwall (OUTR), Phillips 66, T-Mobile (TMUS), Twitter (TWTR) and Yelp.

These potential trades are entirely based upon what may be a discrepancies between the implied price movement and option premiums that will return the desired premium. Generally, I don’t think very much about those issues that may have relevance prior to considering a purchase of shares. The focus is entirely on numbers and whether the risk-reward proposition is appealing. Issues such as whether people are tweeting enough or whether a company is based upon a pyramid strategy can wait until the following week. Hopefully, by that time I would be freed from the position and would be less interested in those issues.

Deciding to pull the trigger is often a function of the prevailing price dynamic. My preference when selling put contracts is to do so if shares are falling in price in advance of earnings. For example, last week I did not sell puts on Facebook (FB), as its shares rose sharply prior to earnings. In that case, that represented a missed opportunity, however.

Compared to the previous week’s close of trading when the market had a sizable gain, this past Friday there were widespread losses, perhaps resulting in a different dynamic as the coming week begins its trading.

While I would rather not take ownership of shares, there must be a realization that doing so may be inevitable or may require additional actions in order to prevent that unwanted outcome, such as rolling the put option forward, if possible.

If there is a large decline in share price well beyond that lower boundary, the investor should be prepared for an extended period of needing to juggle that position in order to avoid assignment while awaiting some price recovery. I have some positions, that I’ve done so for months. The end result may be satisfactory, but the process can be draining.

The table may be used as a guide for determining which of this week’s stocks meet risk-reward parameters. Re-assessments should be made as share prices option premiums and strike levels may change.

The table may be used as a guide for determining which of this week’s stocks meet risk-reward parameters. Re-assessments should be made as share prices option premiums and strike levels may change.

While the list can be used in executing trades before the release of earnings, there may also be opportunity to consider trades following earnings. I typically like to consider those trades if a stock moved higher before earnings and then plunged afterward, if in the belief that the response was an over-reaction to the news. In such cases there may be an opportunity to sell put options whose premiums will still see some enhancement as a reflection of the strong negative sentiment taking shares lower.

Ultimately, if large price movements are either anticipated or have already occurred there is usually some additional opportunity that arises with the perceived risk at hand. If the risk isn’t realized, or if the risk is managed appropriately, the reward can be very addictive.

May102014

Weekend Update – May 11, 2014

A few hundred years ago Sir Isaac Newton is widely credited with formulating the Law of Universal Gravitation.

A few hundred years ago Sir Isaac Newton is widely credited with formulating the Law of Universal Gravitation.

In hindsight, that “discovery” shouldn’t really be as momentous as the discovery more than a century earlier that the sun didn’t revolve around the earth. It doesn’t seem as if it would take an esteemed mathematician to let the would know that objects fall rather than spontaneously rise. Of course, the Law is much more complex than that, but we tend to view things in their most simplistic terms.

Up until recently, the Law of Gravity seemed to have no practical implications for the stock market because prices only went higher, just as the sun revolved around the earth until proven otherwise. Additionally, unlike the very well defined formula that describe the acceleration that accompanies a falling object, there are no such ways to describe how stocks can drop, plunge or go into free fall.

For those that remember the “Great Stockbroker Fallout of 1987,” back then young stockbrokers could have gone 5 years without realizing that what goes up will come down, fled the industry en masse upon realizing the practical application of Newton’s genius in foretelling the ultimate direction of every stock and stock markets.

The 2014 market has been more like a bouncing ball as the past 10 weeks have seen alternating rises and falls of the S&P 500. Only a mad man or a genius could have predicted that to become the case. It’s unlikely that even a genius like Newton could have described the laws governing such behavior, although even the least insightful of physics students knows that the energy contained in that bouncing ball is continually diminished.

As in the old world when people believed that the world was flat and that its exploration might lead one to fall off the edge, I can’t help but wonder what will happen to that bouncing ball in this flat market as it deceptively has come within a whisker of even more records on the DJIA and S&P 500. Even while moving higher it seems like there is some sort of precipice ahead that some momentum stocks have already discovered while functioning as advance scouts for the rest of the market.

With earnings season nearing its end the catalyst to continue sapping the energy out of the market may need to come from elsewhere although I would gladly embrace any force that would forestall gravity’s inevitable power.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories.

As a past customer, I was never enamored of Comcast (CMCSA) and jumped at the first opportunity to switch providers. But while there may be some disdain for the product and especially the service, memories of which won’t easily be erased by visions of a commercial showing a comedian riding along in a service truck, you do have to admire the company’s shares.

Having spent the past 6 months trading above $49 it has recently been range bound and that is where the appeal for me starts. It’s history of annual dividend increases, good option premiums and price stability adds to that appeal. While there is much back story at present in the world of cable providers and Comcast’s proposed purchase of Time Warner Cable (TWC) may still have some obstacles ahead, the core business shouldn’t be adversely impacted by regulatory decisions.

Also, as a one time frequent customer of Best Buy (BBY), I don’t get into their stores very often anymore. Once they switched from a perpendicular grid store layout to a diagonal one they lost me. Other people blame it on Amazon (AMZN), but for me it was all about the floor plan. But while I don’t shop there very much anymore it’s stock has been a delight trading at the $26 level.

Having had shares assigned for the fourth time in the past two months I would like to see a little bit of a price drop after Friday’s gain before buying shares again. However, with earnings coming up during the first week of the June 2014 option cycle you do have to be prepared for nasty surprises as are often delivered. There’s still more time for someone to blame cold weather on performance and this may be the retailer to do so. WIth that in mind, Best Buy may possibly be better approached through the sale of put options this week with the intent of rolling over if in jeopardy of being assigned shares prior to the earnings release.

There’s barely a week that I don’t consider buying or adding shares of Coach. I currently own shares purchased too soon after recent earnings and that still have a significant climb ahead of them to break even. However, with an upcoming dividend during the June 2014 cycle and shares trading near the yearly low point, I may be content with settling in with a monthly option contract, collecting the premium and dividend and just waiting for shares to do what they have done so reliably over the past two years and returning to and beyond their pre-earnings report level.

Mosaic (MOS) is another one of those companies that I’ve owned on many occasions over the years. Most recently I’ve been a serial purchaser of shares as its share price plunged following announcement of a crack in the potash cartel. Still owning some more expensive shares those serial purchases have helped to offset the paper losses on the more expensive shares. Following a recent price pullback after earnings I’m ready to again add shares as I expect Mosaic to soon surpass the $50 level and stay above there.

Dow Chemical (DOW) is also a company whose shares I’ve owned with frequency over the years, but less so as it moved from $42 to $50. Having recently decided that $48 was a reasonable new re-entry point that may receive some support from the presence of activist investors, the combination of premiums, dividends and opportunity for share appreciation is compelling.

Holly Frontier (HFC) has become a recent favorite replacing Phillips 66 (PSX) which has just appreciated too much and too fast. While waiting for Phillips 66 to return to more reasonable levels, Holly Frontier has been an excellent combination of gyrating price movements up and down and a subsequent return to the mean. Because of those sharp movements its option premium is generally attractive and shares routinely distribute a special dividend in addition to a regular dividend that has been routinely increased since it began three years ago.

The financial sector has been weak of late and we’ve gotten surprises from JP Morgan (JPM) recently with regard to its future investment related earnings and Bank of America (BAC) with regard to its calculation error of capital on its books. However, Morgan Stanley (MS) has been steadfast. Fortunately, if interested in purchasing shares its steadfast performance hasn’t been matched by its share price which is now about 10% off its recent high.

With its newly increased dividend and plenty of opportunity to see approval for a further increase, it appears to be operating at high efficiency and has been trading within a reasonably tight price range for the past 6 months, making it a good consideration for a covered option trade and perhaps on a serial basis.

Since I’ve spent much of 2014 in pursuit of dividends in anticipation of decreased opportunity for share appreciation, Eli Lilly (LLY) is once again under consideration as it goes ex-dividend this week. With shares trading less than 5% from its one year high, I would prefer a lower entry price, but the sector is seeing more interest with mergers, acquisitions and regulatory scrutiny, all of which can be an impetus for increasing option premiums.

Finally, it’s hard to believe that I would ever live in an age when people are suggesting that Apple (AAPL) may no longer be “cool.” For some, that was the reason behind their reported purchase of Beats Music, as many professed not to understand the synergies, nor the appeal, besides the cache that comes with the name.

Last week I thought there might be opportunity to purchase Apple shares in order to attempt to capture its dividend and option premium in the hope for a quick trade. As it work turn out that trade was never made because Apple opened the week up strongly, continuing its run higher since recent earnings and other news were announced. I don’t usually chase stocks and in this case that proved to be fortuitous as shares followed the market’s own ambivalence and finished the week lower.

However, this week comes the same potential opportunity with the newly resurgent Microsoft (MSFT). While it’s still too early to begin suggesting that there’s anything “cool” about Microsoft, there’s nothing lame about trying to grab the dividend and option premium that was elusive the previous week with its competition.

Microsoft has under-performed the S&P 500 over the past month as the clamor over “old technology” hasn’t really been a path to riches, but has certainly been better than the so-called “new technology.” Yet Microsoft has been maintaining the $39 level and may be in good position to trade in that range for a while longer. It neither needs to obey or disregard gravity for its premiums and dividends to make it a worthwhile portfolio addition.

Traditional Stocks: Comcast, Dow Chemical, Holly Frontier

Momentum: Best Buy, Coach, Morgan Stanley, Mosaic

Double Dip Dividend: Microsoft (5/13 $0.28), Eli Lilly (5/13 $0.49)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Jan122014

Weekend Update – January 12, 2014

Confusion Reigns.

Confusion Reigns.

January is supposed to be a very straightforward month. Everyone knows how it’s all supposed to go.

The market moves higher and the rest of the year simply follows. Some even believe it’s as simple as the first five trading days of the year setting the tone for the remainder still to come.

Since the market loves certainty, the antithesis of confusion, the idea of a few days or even a month ordaining the outcome of an entire year is the kind of certainty that has broad appeal.

But with the fifth trading day having come to its end on January 8th, the S&P 500 had gone down 11 points. Now what? Where do we turn for certainty?

To our institutions, of course, especially our central banking system which has steadfastly guided us through the challenges of the past 6 years. The year started with some certainty as Federal Reserve Chairman nominee Janet Yellen was approved by a vote that saw fewer negative votes cast than when her predecessor Ben Bernanke last stood for Senate approval, although there were far fewer total votes, too. On a positive note, while there was voting confusion among political lines, there was only certainty among gender lines.

While Dr. Yellen’s confirmation was a sign to many that a relatively dovish voice would predominate the FOMC, even as some more hawkish governors become voting members this year, the announcement that Dr. Stanley Fischer was being nominated as Vice-Chair sends a somewhat different message and may embolden the more hawkish elements of the committee.

That seems confusing. Why would you want to do that? But then again, why would you have pulled the welcome mat out from under Ben Bernanke?

Then on Friday morning came the first Employment Situation Report of the new year and no one was remotely close in their guesses. Nobody was so pessimistic as to believe that the fewest new jobs created in 14 months would be the result.

But the real confusion was whether that was good news or bad news. Did we want disappointing employment statistics? How would the “new” Federal Reserve react? Would they step way from the taper or embrace it as hawks exert their philosophical position?

More importantly, how is a January Rally supposed to take root in the remaining 14 trading days in this kind of muddled environment?

Personally, I like the way the year has begun, there’s not too much confusion about that being the case, despite my first week having been mediocre. While the evidence is scant that the first five days has great predictive value, there is evidence to suggest that there is no great predictive value for the remainder of the year if January ends the month lower. I like that because my preference is alternating periods of certainty and confusion, as long as the net result remains near the baseline. That is a perfect scenario for a covered option strategy and also tends to increase premiums as volatility is enhanced.

I prefer to think of it as counter-intuitive rather than confusing.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

There’s not much confusion when it comes to designating the best in large retail of late. Most everyone agrees that Macys (M) has been the best among a sorry bunch, yet even the best of breed needed to announce large layoffs in order to get a share price boost after being range bound. However, this week the embattled retail sector seems very inviting despite earnings disappointments and the specter of lower employment statistics and spending power.

Finding disappointments among retailers isn’t terribly difficult, as even Bed Bath and Beyond (BBBY), which could essentially do nothing wrong in 2013 more than made up for that by reporting its earnings report. While earnings themselves were improved, it was the reduced guidance that seems to have sent the buyers fleeing. There was no confusion regarding how to respond to the disappointment, yet its plummet brings it back toward levels where it can once again be considered as a source of option premium income, in addition to some opportunity for share appreciation.

L Brands (LB) shares are now down approximately 12% in the past 6 weeks. It is one of those stocks that I’ve owned, but have been waiting far too long to re-own while waiting for its price to return to reasonable levels. Like Bed Bath and Beyond it offered lower guidance for the coming quarter after heavy promotions that are likely to reduce margins.

Target (TGT) has had enough bad news to last it for the rest of the year. While it recently reported that it sales had been better than expected prior to the computer card data hack, it also acknowledged that there was a tangible decline in shopping activity in its aftermath. Its divulging that as many as 70 million accounts may have been compromised, it seemed to throw all bad news into the mix, as often incoming CEOs do with write-downs, so as to make the following quarter look good in comparison. For its part, Target, recovered nicely on Friday from its initial price decline and has been defending the $62.50 line that I believe will be a staging point higher.

Sears Holdings (SHLD) on the other hand doesn’t even pretend to be a ret

ailer. The promise of great riches in its real estate holdings is falling on deaf ears and its biggest proponent and share holder, Eddie Lampert, has seen his personal stake reduced amid hedge fund redemptions. Shares plummeted after reporting disappointing holiday sales. What’s confusing about Sears Holding is how there is even room for disappointment and how the Sears retail business continues, as it has recently been referred to as a “national tragedy.”

But I have a soft spot in my heart for companies that suffer large event driven price drops. Not that I believe there is sustainable life after such events, but rather that there are opportunities to profit from other people like me who smell an opportunity and add support to the share price. However, my time frame is short and I don’t necessarily expect investor largesse to continue.

I did sell puts on Sears Holding on Friday, but would not have done so if the event and subsequent share plunge had been earlier in the option cycle. Sears Holdings, only offers monthly options and in this case there is just one week left in that cycle. If faced with the possibility of assignment I would hope to be able to roll the puts options forward, but do have some concerns about a month long exposure, despite what would likely be an attractive premium.

While there’s no confusion about the nature of its products, Lorillard’s (LO) recent share decline, while not offering certainty of its end, does offer a more reasonable entry point for a company that offers attractive option premiums even when its very healthy dividend is coming due. Like Sears Holdings, Lorillard only offers monthly option contracts, but in this case I have no reservations about holding shares for a longer time period if not assigned.

Conoco Phillips (COP) has been eclipsed in my investing attention by the enormous success of its spin-off Phillips 66 (PSX), but had never fallen off my radar screen. While waiting for evidence that the same will occur to Phillips 66 through its own subsequent spin-off of Phillips 66 Partners (PSXP), my focus has returned to the proud parent, whose shares appear to be ready for some recovery. However, with a dividend likely during the February 2014 option cycle, I don’t mind the idea of shares continuing to run in place and generate option income in a serial manner.

Perhaps not all retailers are in the same abysmal category. Lowes (LOW), while not selling much in the way of fashions or accessories and perennially being considered an also ran to Home Depot, goes ex-dividend this week and has traded reliably at its current level, making it a continuing target for a covered option strategy. I’ve owned in 5 times in 2013, usually for a week or two, and wonder why I hadn’t owned it more often. Following its strong close to end the week I would like to see a little giveback before making a purchase. Additionally, since the ex-dividend date is on a Friday, I’m more likely to consider selling an option expiring the following week or even February, so as to have a greater chance of avoiding early assignment of having sold an in the money option.

Whole Foods (WFM) also goes ex-dividend this week, but its paltry dividend alone is a poor reason to consider share ownership. However, its inexplicable price drop after having already suffered an earnings related drop makes it especially worthy of consideration. While I already own more expensively priced shares and often use lesser priced additional lots in a sacrificial manner to garner option premiums to offset paper losses, I’m inclined to shift the emphasis on share gain over premium at this price level. Reportedly Whole Foods sales suffered during the nation wide cold snap and that may be something to keep in mind at the next earnings report when guidance for the next quarter is offered.

Although earnings season will be in focus this week, especially with big money center banks all reporting, I have no earnings selections this week. Instead, I’m thinking of adding shares of Alcoa (AA) which had fared very nicely after being dis-invited from membership in the DJIA and not so well after leading off earnings season on Thursday.

While I typically am niot overly interested in longer term oiutlooks, CEO Klaus Kleinfeld’s suggestion that demand is expected to increase strongly in 2014 could help to raise Alcoa’s margins. Even a small increase would be large on a percentage basis and could easily be the fuel for shares to continue their post DJIA-explusion climb.

Finally, I was a bit confused as Verizon’s (VZ) shares took off mid-day last week and took it beyond the range that I thought my shares wouldn’t be assigned early in order to capture the dividend. In the absence of news the same didn’t occur with shares of AT&T which was also going ex-dividend the next day and other cell carriers saw their shares drop. In hindsight, the drop in shares the next day, well beyond the impact of dividends, was just as confusing. Where there is certainty, however, is that shares are now more reasonably priced and despite their recent two day gyrations trade with low volatility compared to the market, making them a good place to park money for the defensive portion of a portfolio.

Traditional Stocks: Bed Bath and Beyond, Conoco Phillips, L Brands, Lorillard, Target, Verizon

Momentum Stocks: Alcoa, Sears Holdings

Double Dip Dividend: Lowes (ex-div 1/17), Whole Foods (ex-div 1/14)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Oct132013

Weekend Update – October 13, 2013

This week I’m choosing “risk on.”

This week I’m choosing “risk on.”

For about 6 months I’ve been overly cautious, having evolved from a fully invested trader to one starting most weeks at about 40% cash reserves and maintaining about 25-30% by week’s end after initiating new positions.

Despite the belief that something untoward was right around the corner, the desire for current income through the purchase of stocks and the sale of options has been strong enough to temper the heightened caution on an ongoing basis for much of the past half year.

With uncertainty permeating the market’s mood, eased by late last week’s glimmer of hope that perhaps a short term debt ceiling increase may be at hand, “risk on” isn’t the most likely of places to find me playing with my retirement funds, but that’s often where it’s the most interesting, especially if the risk is one of perception more than one of probability.

While we may all have different operational definitions of what constitutes “risk” I consider beta, upcoming known market or stock moving events, the unknown, past price history and relative performance. Tomorrow the formula may be entirely different, as may tolerance for risk or willingness to burn down the cash reserves.

However, trying to dispassionately look at the current market and all of the talk about a correction, one metric that I’ve been using for the past few months reminds me that we’re doing just fine and that risk is still tolerable, even in the context of uncertainty.

Although I continue to believe that we can’t just keep moving higher, I’m not quite as dour when seeing that we are essentially at the same levels the S&P 500 stood on May 21, 2013 and June 18, 2013.

Those dates reflect relative high points, each of which gave way to the FOMC minutes or a press conference by Federal Reserve Chairman Bernanke.

In fact, we’re actually at a higher level than either of those two previous peaks, now trailing only the all time high of September 18, 2013 by less than 1.5%. So all in all, not too bad, especially since that 50 Day Moving Average that was breached by the S&P 500 earlier in the week was quickly remedied and the 200 Day Moving Average remains relatively distant.

From May 21 to June 5, then from June 18 to June 24, August 2 to 27 and finally September 19 to October 6, we have gone down a combined 16.7% in a cumulative trading period of 13 weeks or the equivalent of a quarter.

What more do you want? Armageddon?

For the past few months I’ve been focusing increasingly on new positions that have been trading below the May and June highs and preferably under-performing the S&P 500 at the same time. However, within that framework I’ve focused increasingly on near term dividend paying stocks and those more likely to fall into the “Traditional” category, typically low beta and attempting to avoid any known short term risk factors.

That has meant fewer “Momentum” positions and fewer earnings related trades. But up until Friday’s continuation of the hope induced rally, I had a number of “Momentum” stocks on my radar, all of which I had already owned and anticipated being assigned, but ripe for re-purchase in the pursuit of risk heightened premiums, but with less risk than readily apparent.

As it turned out Abercrombie and Fitch (ANF) got caught up in The Gaps’ same stores problem and whip-sawed in trading and I ultimately rolled over the position. Meanwhile, Mosaic (MOS) fell as investors were somehow surprised that Potash (POT) adjusted its guidance downward to reflect lower prices stemming from a collapse of the cartel.

As it would turn out Phillips 66 (PSX) was assigned, but soared, making it too expensive for repurchase, but that can change very quickly.

This week there are two deadlines. One is the end of the October 2013 option cycle, but the other is October 17, 2013, which Treasury Secretary Jack Lew proclaimed to be the day after which none of his “tricks” would be able to sustain the Treasury’s count and be able to pay our bills.

In a word? That’s when we would see the United States go into default on its obligations.

Under Senate questioning last week Lew acquitted himself quite well and demonstrated that he wasn’t very patient with regard to suffering fools. Uncharacteristically there appeared to be less self-aggrandizing statements in the form of questions coming from the committee members.

It may not be entirely coincidental that minutes after Lew’s appearance, House Speaker Boehner’s office announced that the Speaker would be making a statement reflecting upcoming meetings with the Administration, reflecting the possibility of some agreement.

For those that remember past such budgetary crises, you’ll recall that the market typically reacted to the hopes and then crashed along with the dashed hopes, in an eerily rhythmic manner.

On Saturday morning, word came from Eric Cantor (R-VA) that President Obama rejected the House offer. Unusually, GOP leadership skipped the opportunity to step up to the microphone to push their version of righteousness.

This week, in anticipation of the possibility of dashed hopes as may come from an appearing setback, my definition of “risk on” includes positions already trading at depressed levels.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

For dividend lovers this week offers Footlocker (FL), Colgate (CL) and Caterpillar (CAT). All under-performing the S&P 500 YTD.

Colgate, however, is higher than its June 2013 high and has a surprisingly high beta, despite the perceived sedate nature of being a consumer defensive stock. Perhaps that combination makes it a “risk on” position for me. Coupled with a dividend that is lower than the overall S&P 500 average it may not readily appear to be worth the time, but then again, how much additional downside should accrue from a US default?

I already own two lots of Footlocker and three is generally my limit, as it precluded including Mosaic in this week’s recommendations. Footlocker doesn’t report earnings until the December 2013 option cycle, so a little bit of risk is removed, although in the world of retail you are always at risk for any of your competitors that may still report monthly comparison data, just look at the pall created by The Gap (GPS) and L Brands (LTD) this past week.

While a pall was created by L Brands and it is higher than those referenced high points it is now down a tantalizing 10% in a week’s time. I’ve already owned shares on five separate occasions this year and have been waiting for an opportunity to do so again. It is a generally reliably trading stock that had simply climbed too far and for a month’s time traveled only in a single direction. That’s rarely sustainable. The combination of premium and dividend makes L Brands worthy of consideration in a sector that has been challenged of late. The lack of weekly options makes ownership less stressed by day to day events for those otherwise inclined to like weekly options.

Not to be outdone, Joy Global (JOY) is a stock that’s been worth owning on 7 distinct occasions this year. It has consistently traded in tight range and has been able to find its way home if temporarily wandering. High beta, well underperforming the S&P 500 and lower than both of the two earlier market high points continues to make it an appealing short term selection, especially with earnings still so far off in the future.

I’ve been waiting to add shares of Caterpillar for a while, having owned it only four times in 2013, as compared to nine occasions in 2012. However, the upcoming dividend makes another purchase more likely. Despite the thesis advanced by short seller Jim Chanos against Caterpillar, it has, thus far continued to maintain its existence in a tight trading range, making it an excellent covered option candidate.

JP Morgan Chase (JPM) reported its earnings this past Friday and reported a loss for the first time under Jamie Dimon’s watch. Regardless of your position on the merits of the myriad of legal and regulatory cases which have resulted in spectacular legal fees and fines, JP Morgan has acquitted itself nicely on the bottom line. While there is still unknown, but tangible punishment ahead, for which shareholders are doubly brutalized, I think a sixth round of share ownership is warranted at this price level.

Williams Sonoma (WSM) was one of the first stocks that I purchased specifically to attempt to capture its dividend and have it partially underwritten by an option premium. It fell a bit by the wayside as weekly options appeared on the scene. However, as uncertainty creeps into the market there is a certain comfort that comes from a monthly or even longer term option contract. WHile it has come down nearly 15% in the past two months and is now priced lower than during the May and June market highs, Williams Sonoma’s dirty little secret is that it has still outperformed the S&P 500 YTD by a whisker.

SanDisk (SNDK) had its eulogy written many years ago when flash memory was written off as being simply a commodity. Always volatile, especially in response to earnings, which have seen plunges on each of those last two occasions, now may not be the time to believe that “the third time is a charm,” although I do. Despite that, my participation, if any, would be in the sale of out of the money puts, as the options market is implying a move of approximately 7% and that may not be aggressive enough, given past history.

FInally, Align Technology (ALGN) reports earnings this week. In the business of making orthodontic therapy so easy that even a monkey could do it, the company’s prospects have significantly improved as its treatment solutions are increasingly geared toward children. That’s important because their traditional customer base, adults, views orthodontic treatment as discretionary and, therefore, represents an economically sensitive purchase. But most anyone with kids knows that orthodontic treatment isn’t discretionary at all. It can be as close to life and death as you would like to experience. This kind of orthodontic care represents a new profit center for many dental offices and a boon to Align Technology. While I expect good earnings numbers, shares have already had a 13% price decline in the past two weeks. I would most likely consider entering a position by means of selling out of the money puts. In this case for a single week’s position, if unassigned, as much as a 12% price drop could still yield a 1.3% ROI, as the options market is implying a 9% earnings related move.

Traditional Stocks: JP Morgan, L Brands, Williams Sonoma

Momentum Stocks: Joy Global

Double Dip Dividend: Caterpillar (ex-div 10/17), Colgate (ex-div 10/18), Footlocker (ex-div 10/16)

Premiums Enhanced by Earnings: Align Technology (10/17 PM), SanDisk (10/16 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.