I’m not really certain what persuaded markets to do as they did this past week.

I’m not really certain what persuaded markets to do as they did this past week.

Given the very wide range of interpretations for what caused the various ups and downs during trading it seems like no one really had any clue of what was going on and influencing trading, although that didn’t stop anyone from trying to explain it all.

With this earnings season having essentially concluded and the new one still two weeks away and with absolutely nothing seeming ready to implode or explode in the world, the market found itself in a vacuum and having to decide its own fate, while simultaneously being sucked along by whatever unexplainable momentum existed on any particular day.

That momentum changed daily and often saw intra-day swings, as well, with optimism being generally something reserved for the mornings and pessimism to end the trading sessions.

Like a child without guidance it’s hard to know what to do when nothing is happening around you other than random events. Add to that some native hyperactivity and you have a formula for unexplainable actions.

I think that may be the source of some of the confusion exhibited this past week. There were simply no guideposts and nothing to react to or against. Not even a Federal Reserve Chairman’s wayward words. When you are left to be alone with your thoughts and you begin to delve into your introspective mode anything may come out from the other end.

Observations, though were easy to make and of course every casual observation led to interpretations and conclusions regarding what each event meant for the market’s future.

Momentum stocks suddenly had the brakes put on them. The observations about momentum stocks was unending, but always led to the same conclusion.

That signals a top.

The NASDAQ, as a result was suffering disproportionately. That signals a top.

The less than successful post-IPO trading of King Digital Entertainment (KING) and others signals a top.

And so on and on. Without a doubt the emphasis was on all of the negative signs being exhibited and the negative outcomes that could be the only possible results to come.

I can’t be accused of being a unrepentant bull and have certainly been more cautious than has been warranted over the past year, but when you hear a cacophony of warnings about being at the top it may be time to see what lies even higher. When one of my favorite CNBC shows, Street Signs, begins the session with a segment “Should your clients be in Momentum Stocks,” that reinforces my unfounded opinion.

In some cases the vacuum leads you to a very specific place and offers no ability for fine tuning your destination to suit your needs or the environment. However, at least next week the vacuum may be disrupted as we do have some potentially market moving events as the European Central Bank chimes in and the Employment Situation Report is released. Both of those have had a recent and more lengthy history, respectively, of being market advancers.

Of course, late reports on Friday of increasing numbers of Russian troops appearing on the Ukraine borders may be just the thing to break that vacuum, in which case, maybe all of those warnings about Momentum stocks may turn out to be right, but for the wrong reasons.

Still, right is right.

Interestingly, when the story of potential conflict in Crimea first broke some weeks ago, also on a Friday afternoon, the market ceded significant gains heading into the close. The repeat of the story, with the same timing produced no identifiable reaction going into the close of trading.

Or as the Russian army may say by Monday morning, “Might is right.”

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend and Momentum categories, with no “PEE” selections this week (see details).

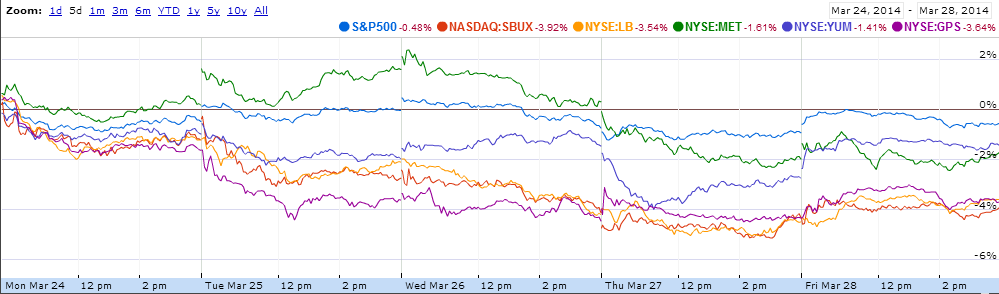

This past week, while not being one that saw a large overall drop in the market did see some under-performance of the broader S&P 500, which dropped 0.48%, as compared to the narrower DJIA which gained 0.12%. That gap was narrowed considerably by the S&P 500’s strong performance on Friday, bettering the DJIA by 0.10%.

While there was certainly some price givebacks among the higher flying momentum stocks, there was also some selling in more esteemed and established names, such as Starbucks (SBUX), YUM Brands (YUM), L Brands (LB), Lowes (LOW) and The Gap (GPS), among others.

Starbucks, for example, was down about 4% for the week. However, even prior to this week it had under-performed the S&P 500 YTD and could hardly be in the same category as those truly high flying and low earning entities. Yet, in the absence of any meaningful news Starbucks was among those suffering out of proportion this week and returning to a more reasonable entry price for a new position.

Starbucks, for example, was down about 4% for the week. However, even prior to this week it had under-performed the S&P 500 YTD and could hardly be in the same category as those truly high flying and low earning entities. Yet, in the absence of any meaningful news Starbucks was among those suffering out of proportion this week and returning to a more reasonable entry price for a new position.

Much of the above could also be said about L Brands. A consistent performer in a sector that is consistently challenging, L Brands’ 3.5% drop this past week simply bring

s it back to a more agreeable entry point. While I do like this company as part of a covered option strategy, its available strike prices and having only monthly options available makes me most interested either before a dividend date or when the entry price is close to one of the available strike prices in order to optimize the option premium obtained. While I would like to see shares still drop a bit further the drops this week may be the only invitation forthcoming.

YUM Brands is a perennial favorite of mine and consistently is punished for any news that may be interpreted as rocking the boat. Generally, this has meant any news regarding a downturn in the Chinese economy. However, YUM has shown itself to be resilient, as consumers want to keep consuming, even if the economy falters. Eating can be every bit as addictive as a smartphone game. This time YUM introduced an expanded menu concept for China and the reaction was swift and negative although there was recovery to end the week.

The fact that YUM Brands offers its dividend the following week and has now put some space between the ex-dividend date and its scheduled earnings report makes it an appealing proposition, potentially using the monthly contract rather than a weekly or expanded weekly option.

The Gap has a bad habit of still reporting monthly same store sales, a practice that many other retailers have abandoned. They usually do so near the end of the first week of each month. The stock always seems to react wildly after those reports, alternating between elation and grave despair, but not in a predictable pattern. Too bad, but it’s that seizure like movement that helps to support its option premiums that are often very attractive, particularly as it trades in a price range. Like YUM Brands, The Gap will go ex-dividend the following week and may warrant the sale of a longer option contract.

MetLife (MET) has been getting whipsawed a bit of late as its fate rises or falls along with the direction of interest rates. Like a number of other stocks it has fallen and may represent a relative value, although I would still like to see it still lower. However, its option premium does offer some cushion in the event of further interest rate liability. as interest rate increases become a more near reality, as Janet Yellen may have h��inted, MetLife’s fortunes should rise along with rates.

Lowes was the� best performing of this group of weekly laggards. It too had a little bit of a rebound in Friday’s trading and could stand to come down some more, but it has been a consistently reliable performer in the $48 range when used as part of a covered option strategy. While at or near that range there aren’t too many headwinds ahead to knock shares out of that trading range.

Bristol Myers Squibb (BMY) slid the previous week along with the more clearly obvious biotechnology stocks. I purchased shares last week that are at risk for being assigned early this coming week due to the upcoming ex-dividend date. While I will still be satisfied with the return if that does occur, I am likely to want to add more shares, both to capture dividend and to capture share appreciation, as selling in shares was really unwarranted and any fallout from Congressional inquiry of drug pricing is still far off. Until then, there is opportunity to recover from that recent drop.

Granted, the preceding were all fairly boring. Despite my belief that “Momentum” may not be as dead as “experts” may have you believe, I’m not even remotely tempted to explore the real high fliers, such as Tesla (TSLA), SolarCity (SCTY) and NetFlix (NFLX), among others. I have my own “Momentum” stocks and they offer me all of the excitement that I need, want or can deal with.

Despite their strong performance on Friday, even as the market lost steam in the final hours, I’m ready to look at and possibly own Abercrombie and Fitch (ANF), Best Buy (BBY) and Las Vegas Sands (LVS), again.

After a one week period of ownership of Best Buy, in order to capture its dividend, I’m ready to own shares again as it seems to be comfortable trading at the $26 level. While it’s easy to disparage the company has having lived beyond its useful age and perhaps being an anachronism, it continues to be a significant part of our lives and our spending. It’s recent price drops after disappointing earnings have provided multiple opportunities to find entry points, especially as it trades in a horizontal pattern as it has for the past two months. For anyone trying to generate option premium income there’s no better pattern to do so than the one that Best Buy has recently been following.

Abercrombie and Fitch is a frequent portfolio holding and would be a charter member of the “Dysfunctional Stock Fund.” Somehow, despite everyone saying that it no longer sells anything fashionable and that it has one of the worst CEOs imaginable, it just continues to be a serial profit generator when used in a covered call strategy. It is now trading near the top of the range where I would rush in to buy shares, but if it can give up some of the previous week’s late gains, I’m ready to deal with the dysfunction again. Profits ,make dysfunction much more tolerable.

Las Vegas Sands and its Chairman, Sheldon Adelson are now embroiled in the on-line gaming controversy pitting himself against other major industry players. If not for that subject, surely Ad�elson would find other controversies for his own entertainment. But this week as he met with political leaders to press his case the entire sector under-performed the market, with Las Vegas Sands running in the middle of that pack. Having fallen about 10% in the past 3 weeks, if I were a gambling man I might take odds that this was about as low as shares were going to go without me on board.

�Finally, while so much attention is being focused on Herbalife (HLF) it seems that the real shame should be heaped on the private education group. Whether looking at their graduation rates, student loan defaults or other measures, one has to wonder about their rightful place in society, as long as some deference is given to the occasional successful graduate who can be identified on the basis of appearing in a television commercial touting the wonders of the particular educational model offered by Apollo and others.

But, as with any disdain I may have for smoking, that do�esn’t mean that trying to exploit the stock is above me. In this case, an always volatile Apollo Education Group (APOL) and one perennially subject to bad news that may move shares, reports

earnings this week.

With an implied price move of 11.7% a 1% ROI may be generated even if shares fall as much as 16%. That’s the kind of risk-benefit proposition that even Sheldon Adelson may be willing to� embrace.

Traditional Stocks: L Brands, Lowes, MetLife, Starbucks, The Gap, YUM Brands

Momentum Stocks: Abercrombie and Fitch, Best Buy, Las Vegas Sands

Double Dip Dividend: Bristol Myers Squibb (4/2)

Premiums Enhanced by Earnings: Apollo

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.