At first glance there’s not too much to celebrate so far, as the first month of 2015 is now sealed and inscribed in the annals of history.

At first glance there’s not too much to celebrate so far, as the first month of 2015 is now sealed and inscribed in the annals of history.

It was another January that disappointed those who still believe in or talk about the magical “January Effect.”

I can’t deny it, but I was one of those who was hoping for a return to that predictable seasonal advance to start the new year. To come to a realization that it may not be true isn’t very different from other terribly sad rites of passage usually encountered in childhood, but you never want to give up hoping and wishing.

It was certainly a disappointment for all of those thinking that the market highs set at the end of December 2014 would keep moving higher, buoyed by a consumer led spending spree fueled by all of that money not being spent on oil and gas.

At least that was the theory that seemed to be perfectly logical at the time and still does, but so far is neither being borne out in reality nor in company guidance being offered in what is, thus far, a disappointing earnings season.

Who in their right mind would have predicted that people are actually saving some of that money and using it to pay down debt?

That’s not the sort of thing that sustains a party.

What started a little more than a month ago with a strongly revised upward projection for 2015 GDP came to an end with Friday’s release of fourth quarter 2014 GDP that was lower than expected and, at least in part validated the less than stellar Retail Sales statistics from a few weeks ago that many very quick to impugn at the time.

When the week was all said and done neither an FOMC Statement release nor the latest GDP data could rescue this January. Despite a 200 point gain heading into the end of the week in advance of the GDP data, and despite a momentary recovery from another 200 point loss heading into the close of trading for the week fueled by an inexplicable surge in oil prices, the market fell 2.7% for the week. In doing so it just added to the theme of a January that breaks the hearts of little children and investors alike and now leaves markets about 5% below the highs from just a month ago.

Like many, I thought that the January party would get started in earnest along with the start of the earnings season. While not expecting to see much tangible benefit from reduced energy costs reflected in the past quarter, my expectation was that the good news would be contained in forward guidance or in upward revisions.

Silly, right? But if you used common sense and caution think of all of the great things you would have missed out on.

While waiting for earnings to bring the party back to life the big surprise was something that shouldn’t have been a surprise at all for all those who take an expansive view of things. I don’t get paid to be that broad minded, but there are many who do and somehow no one seemed to have taken into consideration what we all refer to as “currency crosswinds.”

Hearing earnings report after earnings report mention the downside to the strong dollar reminded me that it would have been good to have been warned about that sort of thing earlier, although did we really need to be told?

Every asset class is currently in flux. It’s not just stocks going through a period of heightened volatility. Witness the moves seen in Treasury rates, currencies, precious metals and oil and it’s pretty clear that at the moment there is no real safe haven, but there is lots of uncertainty.

A quick glance at the S&P 500’s behavior over the past month certainly shows that uncertainty as reflected in the number of days with gap openings higher and lower, as well as the significant intra-day reversals seen throughout the month.

A quick glance at the S&P 500’s behavior over the past month certainly shows that uncertainty as reflected in the number of days with gap openings higher and lower, as well as the significant intra-day reversals seen throughout the month.

I happen to like volatility, but it was really a party back in 2011 when there was tremendous volatility but at the end of the day there was virtually no net change in markets. In fact, for the year the S&P 500 was unchanged.

If you’re selling options in doesn’t get much better than that, but 2015 is letting the party slip away as it’s having difficulty maintaining prices as volatility seeks to assert itself as we have repeatedly found the market testing itself with repeated 3-5% declines over the past 6 weeks.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories.

If you were watching markets this past Friday afternoon what was turning out to really be a terrible day was mitigated by the performance of the highest priced stock in the DJIA which added nearly 60 points to the index. That notwithstanding, the losses were temporarily reversed, as has been the case so often in the past month, by an unexplained surge in oil prices late in the trading session.

When it appeared as if that surge in oil prices was not related to a fundamental change in the supply and demand dynamic the market reversed once again and compounded its losses, leaving only that single DJIA component to buck the day’s trend.

So far, however, as this earnings season has progressed, the energy sector has not fared poorly as a result of earnings releases, even as they may have floundered as oil prices themselves fell.

Sometimes lowered expectations can have merit and may be acting as a cushion for the kind of further share drops that could reasonably be expected as revenues begin to see the impact of lower prices.

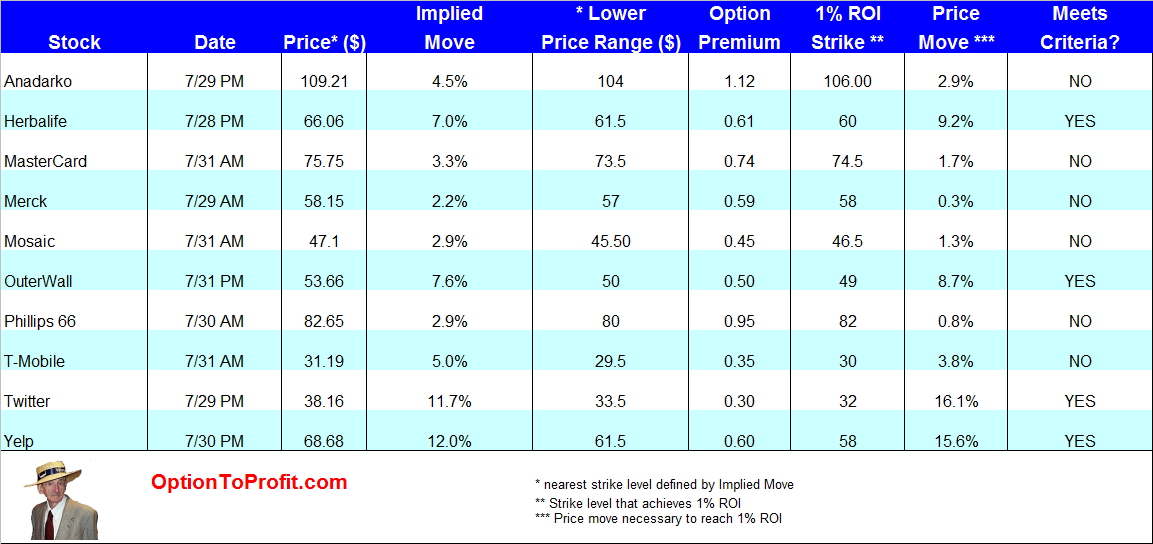

That may change this coming week as Exxon Mobil (NYSE:XOM) reports its earnings before the week begins its trading. By virtue of its sheer size it can create ripples for Anadarko (NYSE:APC) which reports earnings that same day, but after the close of trading.

Anadarko is already well off of the lows it experienced a month ago. While I generally don’t like establishing any kind of position ahead of earnings if the price trajectory has been higher, I would consider doing so if Exxon Mobil sets the tone with disappointing numbers and Anadarko follows in the weakness before announcing its own earnings.

While the put premiums aren’t compelling given the implied move of about 5%, I wouldn’t mind taking ownership of shares if in risk of assignment due to having sold puts within the strike range defined by the option market. As with some other recent purchases in the energy sector, if taking ownership of shares and selling calls, I would consider using strike prices that would also stand to benefit from some share appreciation.

Although I may not be able to tell in a blinded taste test which was an Anadarko product and which was a Keurig Green Mountain Coffee (NASDAQ:GMCR) product, the latter does offer a more compelling reason to sell puts in advance of its earnings report this week.

Frequently a big mover after the event, there’s no doubt that under its new CEO significant credibility has been restored to the company. Its relationship with Coca Cola (NYSE:KO) has certainly been a big part of that credibility, just as a few years earlier its less substantive agreement with Starbucks (NASDAQ:SBUX) helped shares regain lost luster.

The option market is predicting a 9.3% price move next week and a 1.5% ROI can be attained at a strike price outside of that range, but if selling puts, it would be helpful to be prepared for a move much greater than the option market is predicting, as that has occurred many times over the past few years. That would mean being prepared to either rollover the put contracts or take assignment of shares in the event of a larger than expected adverse move.

While crowd sourcing may be a great thing, I’m always amused when reading some reviews found on Yelp (NYSE:YELP) for places that I know well, especially when I’m left wondering what I could have possibly repeatedly kept missing over the years. Perhaps my mistake was not maintaining my anonymity during repeated visits making it more difficult to truly enjoy a hideous experience.

Yet somehow the product and the service endures as it seeks to remove the unknown from experiences with local businesses. But it’s precisely that kind of unknown that makes Yelp a potentially interesting trade when earnings are ready to be announced.

The option market has implied a 12% price move in either direction and past earnings seasons have shown that those shares can easily move that much and more. For those willing to take the risk, which apparently is what is done whenever going to a new restaurant without availing yourself of Yelp reviews, a 1% ROI can be attained by selling weekly put contracts at a strike level 16% below Friday’s closing price.

While the market didn’t perform terribly well last week, technology was even worse, which has to bring International Business Machines (NYSE:IBM) to mind. As the worst performer in the DJIA over the past 2 years it already knows what it’s like to under-perform and it hasn’t flown beneath anyone’s critical radar in that time.

However, among big and old technology it actually out-performed them all last week and even beat the S&P 500. With more controversy certain for next week as details of the new compensation package of its beleaguered CEO were released after Friday’s close, in an attempt to fly beneath the radar, shares go ex-dividend.

While there may continue being questions regarding the relevance of IBM and how much of the company’s performance is now the result of financial engineering, that uncertainty is finally beginning to creep into the option premiums that can be commanded if seeking to sell calls or puts.

With shares trading at a 4 year low the combination of option premium, dividend and capital appreciation of shares is recapturing my attention after years of neglect. If CEO Ginny Rometty can return IBM shares to where they were just a year ago she will be deserving of every one of the very many additional pennies of compensation she will receive, but she had better do so quickly because lots of people will learn about the new compensation package as trading resumes on Monday.

Also going ex-dividend this week are 2 very different companies, Pfizer (NYSE:PFE) and Seagate Technology (NASDAQ:STX), that have little reason to be grouped together, otherwise.

After a recent 6% decline, Pfizer shares are now 6% below their 4 year high, but still above the level where I have purchased shares in the past.

The drug industry has heated up over the past few months with increasing consideration of mergers and buyouts, even as tax inversions are less likely to occur. Even those companies whose bottom lines can now only be driven by truly blockbuster drugs have heightened interest and heightened option premiums associated with their shares which are only likely to increase if overall volatility is able to maintain at increased levels, as well.

Following its recent price retreat, its upcoming dividend and improving option premiums, I’m willing to consider re-opening a position is Pfizer shares, even at its current level.

Seagate Technology, after a nearly 18% decline in the past month was one of those companies that reported a significant impact of currency in offering its guidance for the next quarter, while meeting expectations for the current quarter.

While I often like to sell puts in establishing a Seagate Technology position, with this week’s ex-dividend event, there is reason to consider doing so with the purchase of shares and the sale of calls, as the premium is rich and lots of bad news has already been digested.

I missed an opportunity to add eBay (NASDAQ:EBAY) shares a few weeks ago in advance of earnings, as eBay was one of the first to show some currency headwinds. However, as has been the case for nearly a year, the story hasn

‘t been the business it has been all about activists and the saga of its profitable PayPal unit.

After an initial move higher on announcement of a standstill agreement with Carl Icahn, the activist who pushed for the spin-off of PayPal, shares dropped over the succeeding days back to a level just below from where they had started the process and again in the price range that I like to consider adding shares.

From now until that time that the PayPal spin-off occurs or is purchased by another entity, that’s where the opportunity exists if using eBay as part of a covered call strategy, rather than on the prospects of the underlying business. However, after more than a month of not owning any shares of a company that has been an almost consistent presence in my portfolio, it’s time to bring it back in and hopefully continue serially trading it for as long as possible until the fate of PayPal is determined.

Finally, Yahoo (NASDAQ:YHOO) reported earnings this past week, but took a page out of eBay’s playbook from earlier in the year and used the occasion to announce significant news unrelated to earnings that served to move shares higher and more importantly deflected attention from the actual business.

With a proposed tax free spin off of its remaining shares of Alibaba (NYSE:BABA) many were happy enough to ignore the basic business or wonder what of value would be left in Yahoo after such a spin-off.

The continuing Yahoo – Alibaba umbilical cord works in reverse in this case as the child pumps life into the parent, although this past week as Alibaba reported earnings and was admonished by its real parent, the Chinese government, Yahoo suffered and saw its shares slide on the week.

The good news is that the downward pressure from Alibaba may go on hiatus, at least until the next lock-up expiration when more shares will hit the market than were sold at the IPO. However, until then, Yahoo option premiums are reflecting the uncertainty and offer enough liquidity for a nimble trader to respond to short term adverse movements, whether through a covered call position or through the sale of put options.

Traditional Stocks: eBay

Momentum Stocks: Yahoo

Double Dip Dividend: International Business Machines (2/5), Pfizer (2/4), Seagate Technology (2/5)

Premiums Enhanced by Earnings: Anadarko (APC 2/2 PM), Keurig Green Mountain (2/4 PM), Yelp (2/5 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.