For those of a certain age, you may or may not recall that Marvin Gaye’s popular song “What’s Going On?” was fairly controversial and raised many questions about the behavior of American society both inside and outside of our borders during a time that great upheaval was underway.

The Groucho Marx character Rufus T. Firefly said “Why a four-year-old child could understand this report. Run out and find me a four-year-old child, I can’t make head or tail of it.”

While I could never answer that seminal question seeking an explanation for everything going on, I do know that the more outlandish Groucho’s film name, the funnier the film. However, that kind of knowledge has proven itself to be of little meaningful value, despite its incredibly high predictive value.

That may be the same situation when considering the market’s performance following the initiation of interest rate hikes. Despite knowing that the market eventually responds to that in a very positive manner by moving higher, traders haven’t been rushing to position themselves to take advantage of what’s widely expected to be an upcoming interest rate increase.

In hindsight it may be easy to understand some of the confusion experienced 40 years ago as the feeling that we were moving away from some of our ideals and fundamental guiding principles was becoming increasingly pervasive.

I don’t think Groucho’s pretense of understanding would have fooled anyone equally befuddled in that era and no 4 year old child, devoid of bias or subjectivity, could have really understood the nature of the societal transformation that was at hand.

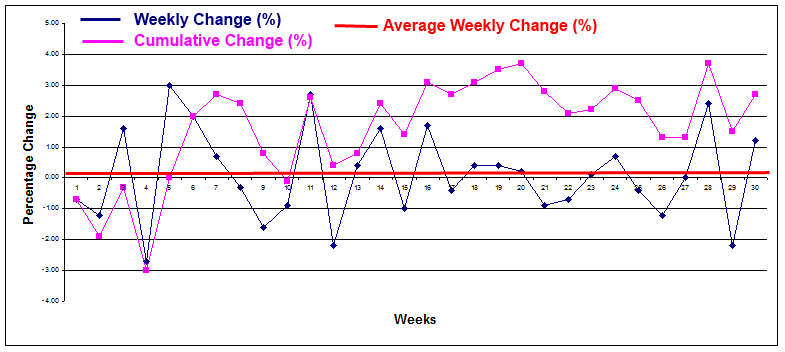

Following the past week’s stealth rally it’s certainly no more clear as to what’s going on and while many are eager to explain what is going on, even a 4 year old knows that it’s best to not even make the attempt, lest you look, sound or read like a babbling idiot.

It’s becoming difficult to recall what our investing ideals and fundamentals used to be. Other than “buy low and sell high,” it’s not clear what we believe in anymore, nor who or what is really in charge of market momentum.

Just as Marvin Gaye’s song recognized change inside and outside of our borders, our own markets have increasingly been influenced by what’s going on outside of those borders.

If you have any idea of what is really going on outside of our borders, especially in China, you may be that 4 year old child that can explain it all to the rest of us.

The shock of the decline in Shanghai has certainly had an influence on us, but once the FOMC finally raises rates, which may come early as this week, we may all come to a very important realization.

That realization may be that what’s really going on is that the United States economy is the best in the world in relative terms and is continuing to improve in absolute terms.

That will be something to sing about.

As usual, the week’s potential stock selections are classified as being in the Traditional, Double Dip Dividend, Momentum or “PEE” categories.

With relatively little interest in wanting to dip too deeply into cash reserves, which themselves are stretched thinner than I would like, I’m more inclined to give some consideration to positions going ex-dividend in the very near future.

Recent past weeks have provided lots of those opportunities, but for me, this week isn’t as welcoming.

The two that have my attention, General Electric (NYSE:GE) and Las Vegas Sands (NYSE:LVS) couldn’t be more different, other than perhaps in the length of tenure of their Chairmen/CEOs.

I currently own shares in both companies and had shares of General Electric assigned this past week.

While most of the week’s attention directed toward General Electric is related to the European Union’s approval of its bid to buy Alstom SA (EPA:ALO), General Electric has rekindled my interest in its shares solely because of its decline along with the rest of the market.

While it has mirrored the performance of the S&P 500 since its high point in July, I would be happy to see it do nothing more than to continue to mirror that performance, as the combination of its dividend and recently volatility enhanced option premium makes it a better than usual candidate for reward relative to risk.

While I also don’t particularly like to re

purchase recently assigned shares at a higher price, that most recent purchase may very well have been at an unrealistically low price relative to the potential to accumulate dividends, premiums and still see capital appreciation of shares.

Las Vegas Sands, on the other hand, is caught in all of the uncertainty surrounding China and the ability of Chinese citizens to part with their dwindling discretionary cash. With highly significant exposure to Macau, Las Vegas Sands has seen its share price bounce fairly violently over the past few months and has certainly reflected the fact that we have no real clue as to what’s going on in China.

As expected, along with that risk, especially in a market with its own increasing uncertainty is an attractive option premium. Since Las Vegas Sands ex-dividend date is on a Friday and it does offer expanded weekly options, there are a number of potential buy/write combinations that can seek to take advantage of the option premium, with or without also capturing the dividend.

The least risk adverse investor might consider the sale of a deep in the money weekly call option with the objective of simply generating an option premium in exchange for 4 days of stock ownership. At Friday’s closing prices that would have been buying shares at $46.88 and selling a weekly $45.50 call option for $1.82. With a $0.65 dividend, shares would very likely be assigned early if Thursday’s closing price was higher than $46.15.

If assigned early, that 4 day venture would yield a return of 0.9%.

However, if shares are not assigned early, the return is 2.3%, if shares are assigned at closing.

Alternatively, a $45.50 September 25, 2015 contract could be sold with the hope that shares are assigned early. In that case the return would be 1.3% for the 4 days of risk.

In keeping with Las Vegas Sand’s main product line, it’s a gamble, no matter which path you may elect to take, but even a 4 year old child knows that some risks are better than others.

Coca Cola (NYSE:KO) was ex-dividend this past week and it’s not sold in Whole Foods (NASDAQ:WFM), which is expected to go ex-dividend at the end of the month.

There’s nothing terribly exciting about an investment in Coca Cola, but if looking for some relative safety during a period of market turmoil, Coca Cola has been just that, paralleling the behavior of General Electric since that market top.

As also with General Electric, its dividend yield is more than 50% higher than for the S&P 500 and its option premium is also reflecting greater market volatility.

Following an 8% decline I would consider looking at longer term options to try and lock in the greater premium, as well as having an opportunity to wait out some chance for a price rebound.

Whole Foods, on the other hand, has just been an unmitigated disaster. As bad as the S&P 500 has performed in the past 2 months, you can triple that loss if looking to describe Whole Foods’ plight.

What makes their performance even more disappointing is that after two years of blaming winter weather and assuming the costs of significant national expansion, it had looked as if Whole Foods had turned the corner and was about to reap the benefits of that expansion.

What wasn’t anticipated was that it would have to start sharing the market that it created and having to sacrifice its rich margins in an industry characterized by razor thin margins.

However, I think that Whole Foods will now be in for another extended period of seeing its share price going nowhere fast. While that might be a reason to avoid the shares for most, that can be just the ideal situation for accumulating income as option premiums very often reflect the volatility that such companies show upon earnings, rather than the treading water they do in the interim.

That was precisely the kind of share price character describing eBay (NASDAQ:EBAY) for years. Even when stuck in a trading range the premiums still reflected its proclivity to surprise investors a few times each year. Unless purchasing shares at a near term top, adding them anywhere near or below the mid-point of the trading range was a very good way to enhance reward while minimizing risk specific to that stock.

While 2015 hasn’t been very kind to Seagate Technology (NASDAQ:STX), compared to so many others since mid-July, it has been a veritable super-star, having gained 3%, including its dividend.

Over the past week, however, Seagate lagged the market during a week when the performance of the technology sector was mixed.

Seagate is a stock that I like to consider for its ability to generate option related income through the sale of puts as it approaches a support level. Having just recovered from testing the $46.50 level, I would consider the sale of

puts and would try to roll those over and over if necessary, until that point that shares are ready to go ex-dividend.

That won’t be for another 2 months, so in the event of an adverse price move there should be sufficient time for some chance of recovery and the ability to close out the position.

In the event that it does become necessary to keep rolling over the put premiums heading into earnings, I would select an expiration a week before the ex-dividend date, taking advantage of either an increased premium that will be available due to earnings or trading down to a lower strike price.

Then, if necessary, assignment can be taken before the ex-dividend date and consideration given to selling calls on the new long position.

Adobe (NASDAQ:ADBE) reports earnings this week and while it offers only monthly option contracts, with earnings coming during the final week of that monthly contract, there is a chance to consider the sale of put options that are effectively the equivalent of a weekly.

Adobe option contracts don’t offer the wide range of strike levels as do many other stocks, so there are some limitations if considering an earnings related trade. The option market is implying a move of approximately 6.7%.

However, a nearly 1% ROI may be achieved if shares fall less than 8.4% next week. Having just fallen that amount in the past 3 weeks I often like that kind of prelude to the sale of puts. More weakness in advance of earnings would be even better.

Finally, good times caught up with LuLuLemon Athletica (NASDAQ:LULU) as it reported earnings. Having gone virtually unchallenged in its price ascent that began near the end of 2014, it took a really large step in returning to those price levels.

While its earnings were in line with expectations, its guidance stretched those expectations for coming quarters thin. If LuLuLemon has learned anything over the past two years is that no one likes things to be stretched too thin.

The last time such a thing happened it took a long time for shares to recover and there was lots of internal turmoil, as well. While its founder is no longer there to discourage investors, the lack of near term growth may be an apt replacement for his poorly chosen words, thoughts and opinions.

However, one thing that LuLuLemon has been good for in the past, when faced with a quantum leap sharply declining stock price is serving as an income production vehicle through the sale of puts options.

I think that opportunity has returned as shares do tend to go through a period of some relative stability after such sharp declines. During those periods, however, the option premiums, befitting the decline and continued uncertainty remain fairly high.

Even though earnings are now behind LuLuLemon, the option market is still implying a price move of % next week. At the same time, the sale of a weekly put option % below Friday’s closing price could still yield a % ROI and offer opportunity to roll over the position in the event that assignment may become likely.

Traditional Stock: Coca Cola, Whole Foods

Momentum Stock: LuLuLemon Athletica, Seagate Technology

Double-Dip Dividend: General Electric (9/17 $0.23), Las Vegas Sands (9/18 $0.65)

Premiums Enhanced by Earnings: Adobe (9/17 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable – most often coupling a share purchase with call option sales or the sale of covered put contracts – in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week, with reduction of trading risk.

Like many people I know who have seen the coming attractions for “Vacation,” I’m anxious to see the film having laughed out loud on the two occasions that I saw the coming attractions.

Like many people I know who have seen the coming attractions for “Vacation,” I’m anxious to see the film having laughed out loud on the two occasions that I saw the coming attractions.

It seems as if it has been a long time since we were at that stage where good economic news was interpreted negatively and bad news was celebrated.

It seems as if it has been a long time since we were at that stage where good economic news was interpreted negatively and bad news was celebrated. You would think that when the market sets record closing highs on the S&P 500 that there would be lots of fireworks after the fact and maybe lots of excited anticipation before the fact.

You would think that when the market sets record closing highs on the S&P 500 that there would be lots of fireworks after the fact and maybe lots of excited anticipation before the fact. Instead of the straight line higher or the “V-shaped” recoveries that so many refer to, and that have characterized upward reversals in the past few months, this most recent reversal has been a stagger stepped one.

Instead of the straight line higher or the “V-shaped” recoveries that so many refer to, and that have characterized upward reversals in the past few months, this most recent reversal has been a stagger stepped one. At first glance there’s not too much to celebrate so far, as the first month of 2015 is now sealed and inscribed in the annals of history.

At first glance there’s not too much to celebrate so far, as the first month of 2015 is now sealed and inscribed in the annals of history. A quick glance at the S&P 500’s behavior over the past month certainly shows that uncertainty as reflected in the number of days with gap openings higher and lower, as well as the significant intra-day reversals seen throughout the month.

A quick glance at the S&P 500’s behavior over the past month certainly shows that uncertainty as reflected in the number of days with gap openings higher and lower, as well as the significant intra-day reversals seen throughout the month.