Things aren’t always as they seem.

Things aren’t always as they seem.

As I listened to Janet Yellen face her Senate inquisitors as the hearing process began for her nomination as our next Federal Reserve Chairman, the inquisitors themselves were reserved. In fact they were completely unrecognizable as they demonstrated behavior that could be described as courteous, demur and respectful. They didn’t act like the partisan megalomaniacs they usually are when the cameras are rolling and sound bites are beckoning.

That can’t last. Genteel or not, we all know that the reality is very different. At some point the true colors bleed through and reality has to take precedence.

Closing my eyes I thought it was Woody Allen’s sister answering softball economic questions. Opening my eyes I thought I was having a flashback to a curiously popular situational comedy from the 1990s, “Suddenly Susan,” co-starring a Janet Yellen look-alike, known as “Nana.” No one could possibly sling arrows at Nana.

These days we seem to go back and forth between trying to decide whether good news is bad news and bad news is good news. Little seems to be interpreted in a consistent fashion or as it really is and as a result reactions aren’t very predictable.

Without much in the way of meaningful news during the course of the week it was easy to draw a conclusion that the genteel hearings and their content was associated with the market’s move to the upside. In this case the news was that the economy wasn’t yet ready to stand on its own without Treasury infusions and that was good for the markets. Bad news, or what would normally be considered bad news was still being considered as good news until some arbitrary point that it is decided that things should return to being as they really seem, or perhaps the other way around..

While there’s no reason to believe that Janet Yellen will do anything other than to follow the accommodative actions of the Federal Reserve led by Ben Bernanke, political appointments and nominations have a long history of holding surprises and didn’t always result in the kind of comfortable predictability envisioned. As it would turn out even Woody Allen wasn’t always what he had seemed to be.

Certainly investing is like that and very little can be taken for granted. With two days left to go until the end of the just ended monthly option cycle and having a very large number of positions poised for assignment or rollover, I had learned the hard way in recent months that you can’t count on anything. In those recent cases it was the release of FOMC minutes two days before monthly expiration that precipitated market slides that snatched assignments away. Everything seemed to be just fine and then it wasn’t suddenly so.

As the markets continue to make new closing highs there is division over whether what we are seeing is real or can be sustained. I’m tired of having been wrong for so long and wonder where I would be had I not grown cash reserves over the past 6 months in the belief that the rising market wasn’t what it really seemed to be.

What gives me comfort is knowing that I would rather be wondering that than wondering why I didn’t have cash in hand to grab the goodies when reality finally came along.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

Sometimes the most appealing purchases are the very stocks that you already own or recently owned. Since I almost exclusively employ a covered option strategy I see lots of rotation of stocks in and out of my portfolio. That’s especially true at the end of a monthly option cycle, particularly if ending in a flourish of rising prices, as was the case this week.

Among shares assigned this past week were Dow Chemical (DOW), International Paper (IP), eBay (EBAY) and Seagate Technology (STX).

eBay just continues to be a model of price mediocrity. It seems stuck in a range but seems to hold out enough of a promise of breaking out of that range that its option premiums continue to be healthy. At a time when good premiums are increasingly difficult to attain because of historically low volatility, eBay has consistently been able to deliver a 1% ROI for its near the money weekly options. I don’t mind wallowing in its mediocrity, I just wonder why Carl Icahn hasn’t placed this one on his radar screen.

International Paper is well down from its recent highs and I’ve now owned and lost it to assignment three times in the past month. While that may seem an inefficient way to own a stock, it has also been a good example of how the sum of the parts can be greater than the whole when tallying the profits that can arise from punctuated ownership versus buy and hold. Having comfortably under-performed the broad market in 2013 it doesn’t appear to have froth built into its current price

Although Dow Chemical is getting near the high end of the range that I would like to own shares it continues to solidify its base at these levels. What gives me some comfort in considering adding shares at this level is that Dow Chemical has still under-performed the S&P 500 YTD and may be more likely to withstand any market downturn, especially when buoyed by dividends, option premiums and some patience, if required.

Unitedhealth Group (UNH) is in a good position as it’s on both sides of the health care equation. Besides being the single largest health care carrier in the United States, its purchase of Quality Software Services last year now sees the company charged with the responsibility of overhauling and repairing the beleaguered Affordable Care Act’s web site. That’s convenient, because it was also chosen to help set up the web site. It too, is below its recent highs and has been slowly working its way back to that level. Any good news regarding ACA, either programmatically or related to the enrollment process, should translate into good news for Unitedhealth

Seagate Technology simply goes up and down. That’s a perfect recipe for a successful covered option holding. It’s moves, in both directions, can however, be disconcerting and is best suited for the speculative portion of a portfolio. While not too far below its high thanks to a 2% drop on Friday, it does have reasonable support levels and the more conservative approach may be through the sale of out of the money put options.

While I always feel a little glow whenever I’m able to repurchase shares after assignment at a lower price, sometimes it can feel right even at a higher price. That’s the case with Microsoft (MSFT). Unlike many late to the party who had for years disparaged Microsoft, I enjoyed it trading with the same mediocrity as eBay. But even better than eBay, Microsoft offered an increasingly attractive dividend. Shares go ex-dividend this week and I’d like to consider adding shares after a moth’s absence and having missed some of the run higher. With all of the talk of Alan Mullally taking over the reins, there is bound to be some let down in price when the news is finally announced, but I think the near term price future for shares is relatively secure and I look forward to having Microsoft serve as a portfolio annuity drawing on its dividends and option premiums.

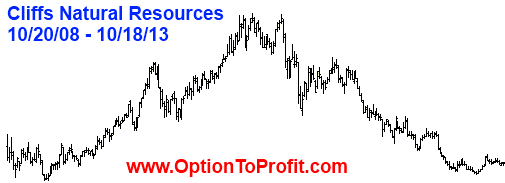

I’m always a little reluctant to recommend a possible trade in Cliffs Natural Resources (CLF). Actually, not always, only since the trades that still have me sitting on much more expensive shares purchased just prior to the dividend cut. Although in the interim I’ve made trades to offset those paper losses, thanks to attractive option premiums reflecting the risk, I believe that the recent sustained increase in this sector is for real and will continue. Despite that, I still wavered about considering the trade again this week, but the dividend pushed me over. Although a fraction of what it had been earlier in the year it still has some allure and increasing iron ore prices may be just the boost needed for a dividend boost which would likely result in a significant rise in shares. I’m not counting on it quite yet, but think that may be a possibility in time for the February 2014 dividend.

While earnings season is winding down there are some potentially interesting trades to consider for those with a little bit of a daring aspect to their investing.

Not too long ago Best Buy (BBY) was derided as simply being Amazon’s (AMZN) showroom and was cited as heralding the death of “brick and mortar.” But, things really aren’t always as they seem, as Best Buy has certainly implemented strategic shifts and has seen its share price surge from its lows under previous management. As with most earnings related trades that I consider undertaking, I’m most likely if earnings are preceded by shares declining in price. Selling puts into price weakness adds to the premium while some of the steam of an earnings related decline may be dissipated by the selling before the actual release.

salesforce.com (CRM) has been a consistent money maker for investors and is at new highs. It is also a company that many like to refer to as a house of cards, yet another way of saying that “things aren’t always as they seem.” As earnings are announced this week there is certainly plenty of room for a fall, even in the face of good news. With a nearly 9% implied volatility, a 1.1% ROI can be attained if less than a 10% price drop occurs, based on Friday’s closing prices through the sale of out of the money put contracts.

Then of course, there’s JC Penney (JCP). What can possibly be added to its story, other than the intrigue that accompanies it relating to the smart money names having taken large positions of late. While the presence of “smart money” isn’t a guarantee of success, it does get people’s attention and JC Penney shares have fared well in the past week in advance of earnings. The real caveat is that the presence of smart money may not be what it seems. With an implied move of 11% the sale of put options has the potential to deliver an ROI of 1.3% even if shares fall nearly 17%.

Finally, even as a one time New York City resident, I don’t fully understand the relationship between its residents and the family that controls Cablevision (CVC), never having used their services. As an occasional share holder, however, I do understand the nature of the feelings that many shareholders have against the Dolan family and the feelings that the publicly traded company has served as a personal fiefdom and that share holders have often been thrown onto the moat in an opportunity to suck assets out for personal gain.

I may be understating some of those feelings, but I harbor none of those, personally. In fact, I learned long ago, thanks to the predominantly short term ownership afforded through the use of covered options, that it should never be personal. It should be about making profits. Cablevision goes ex-dividend this week and is well off of its recent highs. Dividends, option premiums and some upside potential are enough to make even the most hardened of investors get over any personal grudges.

Traditional Stocks: Dow Chemical, eBay, International Paper, Unitedhealth Group

Momentum Stocks: Seagate Technology

Double Dip Dividend: Cablevision (ex-div 11/20), Cliffs Natural (ex-div 11/20), Microsoft (ex-div 11/19)

Premiums Enhanced by Earnings: Best Buy (11/19 AM), salesforce.com (11/18 PM), JC Penney (11/20 AM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

With the S&P 500 having reached an all time high this past week you could certainly draw the conclusion that a government shutdown is a good thing and flirting with default is a constructive strategy. At a reported cost of only $24 Billion associated with closure and nothing more than a symbolic “Fitch slap” credit watch issued, perhaps we should look forward to the next potential round in just a few months.

With the S&P 500 having reached an all time high this past week you could certainly draw the conclusion that a government shutdown is a good thing and flirting with default is a constructive strategy. At a reported cost of only $24 Billion associated with closure and nothing more than a symbolic “Fitch slap” credit watch issued, perhaps we should look forward to the next potential round in just a few months.