This was a good week, every bit as much as it was an odd one.

This was a good week, every bit as much as it was an odd one.

You almost can’t spell “good” without “odd.”

We tend to be creatures that spend a lot of time in hindsight and attempting to dissect out what we believe to be the important components of everything that surrounds us or impacts upon us.

Sometimes what’s really important is beyond our ability to see or understand or is just so counter-intuitive to what we believe to be true. I’m always reminded of the great Ralph Ellison book, “The Invisible Man,” in which it’s revealed that the secret to obtaining the most pure of white paints is the addition of a drop of black paint.

That makes no sense on any level unless you suspend rational thought and simply believe. Rational thought has little role when it calls for the suspension of belief.

This past week there was no reason to believe that anything good would transpire.

Coming on the heels of the previous week, which saw a perfectly good advance evaporate by week’s end there wasn’t a rational case to be made for expecting anything better the following week. That was especially true after the strong sell-off this past Tuesday.

Rational thought would never have taken the antecedent events to signal that the market would alter its typical pattern of behavior on the day of an FOMC statement release. That behavior was to generally trade in a reserved and cautious fashion prior to the 2 PM embargo release and then shift into chaotic knee-jerks and equally chaotic post-kneejerk course corrections.

Instead, the market advanced strongly from the opening bell on that day, erasing the previous day’s losses and had no immediate reaction to the FOMC release and then in an orderly fashion moved mildly higher after the words were parsed and interpreted.

The trading on that day and its timing were entirely irrational. It was odd, but it was good.

Ordinarily it would have also been irrational to expect a rational response to the minutes that offered no new news, as in the past real news was not a necessary factor for irrational buying or selling behavior.

The ensuing rational behavior was also odd, but it, too, was good.

As another new high was set to end the week there should be concern about approaching a tipping point, especially as the number of new highs is on the down trend. However, the market’s odd behavior the past week gives me reason to be optimistic in the short term, despite a belief that the upside reward is now considerably less than the downside risk in the longer term.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories.

This was a week in which those paid to observe such things finally commented on the disappointing results coming from retailers, despite the fact that the past two or three quarters have been similar and certainly not reflective of the kind of increased discretionary spending you might expect with increasing employment statistics.

With some notable exceptions, such as LuLuLemon (LULU) and Family Dollar Store (FDO) I’ve enjoyed being in and out of retailers, although I think I’d rather be maimed than actually be in and out of anyone’s actual store.

This week a number of retailers have appeal, either on their merits or because there may be some earnings related trades seeking to capitalize on their movements. Included for their merits are in the list are Bed Bath and Beyond (BBBY), eBay (EBAY), Nike (NKE) and The Gap (GPS), while Abercrombie and Fitch (ANF) and Kors (KORS) report earnings this week.

After a disappointing earnings report Bed Bath and Beyond has settled into a trading range and gas seemed to establish some support at the $60 level. Along with so many others that have seen their shares punished after earnings the recovery of share price seems delayed as compared to previous markets. For the option seller that kind of listless trading can be precisely the scenario that returns the best results.

eBay has also stagnated. With Carl Icahn still in the picture, but uncharacteristically quiet, especially after the announcement of a repatriation of some $6 billion in cash back to the United States and, therefore, subject to taxes, there doesn’t seem to be a catalyst for a return to its recent highs. That suits me just fine, as I’ve liked eBay at the $52 level for quite a while and it has been one of my more frequent in and out kind of trades. At present, I do own two other lots of shares and three lots is my self imposed limit, but for those considering an initial entry, eBay has been seen as a mediocre performer in the eyes of those expecting upward price movement, but a superstar from those seeking premium income through the serial sale of option contracts week in and out. If you’re the latter kind, eBay can be as rewarding as the very best of the rest.

The Gap reported earnings on Friday and exhibited little movement. It’s currently trading at the high end of where I like to initiate positions, but it, too, has been a very reliable covered option trade. An acceptable dividend and a fair option premium makes it an appealing recurrent trade. The only maddening aspect of The Gap is that it is one of the few remaining retailers that oddly provides monthly same store sales and as a result it is prone to wild price swings on a regular basis. Those price swings, however, tend to be alternating and do help to keep those option premiums elevated.

You simply take the good with the odd in the case of The Gap and shrug your shoulders when the market response is adverse and just await the next opportunity when suddenly all is good again.

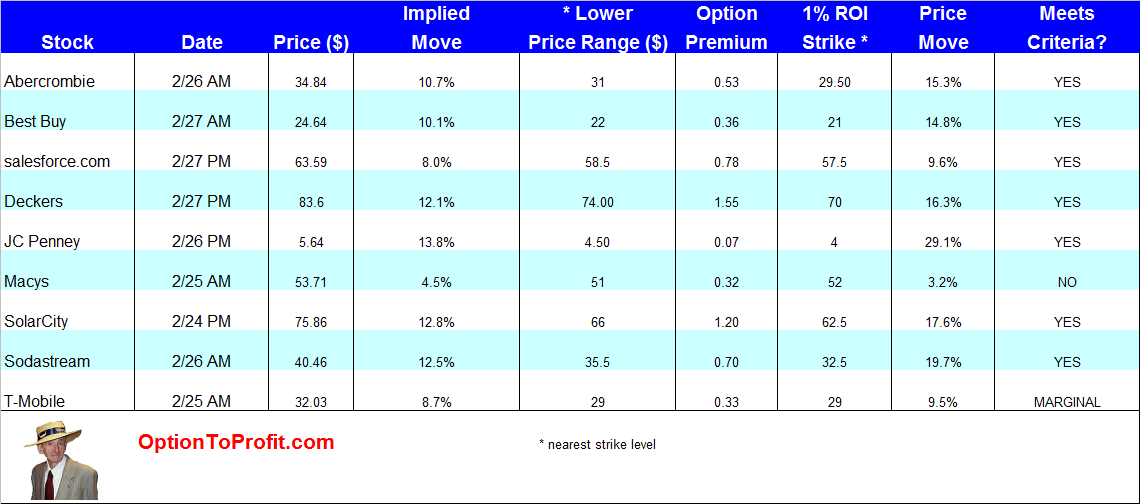

Despite all of the past criticism and predictions of its irrelevance in the marketplace Abercrombie and Fitch continues to be a survivor. This past Friday was the second anniversary of the initial recommendation of taking a position for Option to Profit subscribers, although I haven’t owned shares in nearly 5 months. Since that in

itial purchase there have been 18 such recommendations, with a cumulative 71.5% return, despite shares having barely moved during that time frame.

Always volatile, especially when earnings are due, the options market is currently implying a 10.2% move in price. For me, the availability of a 1% ROI from selling put contracts at a strike level outside of the lower boundary of that implied range gets my interest. In this case shares could fall up to 13.9% before assignment is likely and still deliver that return.

Kors, also known as “Coach (COH) Killer” also reports earnings this week. It has stood out recently because it hasn’t been subject to the same kind of selling pressure as some other “momentum” stocks. The option market is implying a price movement of 7.4%, while a 1% ROI from put sales may be obtained at a strike level currently 8.8% below Friday’s closing price. However, while Abercrombie and Fitch has plenty of experience with disappointing earnings and has experienced drastic price drops, Kors has yet to really face those kinds of challenges. In the current market environment earnings disappointments are being magnified and the risk – reward proposition with an earnings related trade in Kors may not be as favorable as for that with Abercrombie.

In the case of Kors I may be more inclined to consider a trade after earnings, particularly considering the sale of puts if earnings are disappointing and shares plummet.

After last week’s brief ownership of Under Armour (UA) this week it may be time to consider a purchase of Nike, which under-performed Under Armour for the week. Shares also go ex-dividend this week and have been reasonably range-bound of late. It isn’t a terribly exciting trade, but at this stage of life, who really needs excitement? I also don’t need a pair of running shoes and could care less about making a fashion statement, but I do like the idea of its consistency and relatively low risk necessary in order to achieve a modest reward.

Transocean (RIG) is off of its recent lows, but still has quite a way to go to return to its highs of earlier in the year. Going ex-dividend this week, the 5.7% yield has made the waiting on a more expensive lot of shares to recover a bit easier. As with eBay, I already have two lots of shares, but believe that at the current level this is a good time for initial entry, perhaps considering a longer term option contract and seeking capital gains on shares, as well. As with most everything in business and economy, the current oversupply or rigs will soon become an under supply and Transocean will reap the benefits of cyclicality.

Sinclair Broadcasting (SBGI) also goes ex-dividend this week. It is an important player in my area and has become the largest operator of local television stations in the nation, while most people have never heard the name. It is an infrequent purchase for me, but I always consider doing so as it goes ex-dividend, particularly if trading at the mid-point of its recent range. CUrrently shares a little higher than I might prefer, but with only monthly options available and an always healthy premium, I think that even at the current level there is good opportunity, even if shares do migrate to the low end of its current range.

Finally, Joy Global (JOY), one of those companies whose fortunes are closely tied to Chinese economic reports, has seen a recent 5% price drop from its April 2014 highs. While it is still above the price that I usually like to consider for an entry, I may be interested in participating this week with either a put sale of a buy/write.

Among the considerations are events coming the following week, as shares go ex-dividend early in the week and then the company reports earnings later in the week.

While my preference would be for a quick one week period of involvement, there always has to be the expectation of well laid out plans not being realized. In this case the sale of puts that may need to be rolled over would benefit from enhanced earnings related premiums, but would suffer a bit as the price decrease from the dividend may not be entirely reflected in the option premium. That’s similar to what is occasionally seen on the call side, when option premiums may be higher than they rightfully should be, as the dividend is not fully accounted.

Otherwise, if beginning a position with a buy/write and not seeing shares assigned at the end of the week, I might consider a rollover to a deep in the money call, thereby taking advantage of the enhanced premiums and offering a potential exit in the event that shares fall with the guidelines predicted by the implied volatility. Additionally, it might offer the chance of early assignment prior to earnings due to the Monday ex-dividend date, thereby providing a quick exit and the full premium without putting in the additional time and risk.

Traditional Stocks: Bed Bath and Beyond, eBay, The Gap

Momentum: Joy Global

Double Dip Dividend: Nike (5/29 $0.24), Sinclair Broadcasting (5/28 $0.15), Transocean (5/28 $0.75)

Premiums Enhanced by Earnings: Abercrombie and Fitch (5/29 AM), Kors (5/28 AM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

I really didn’t see this past week coming at all.

I really didn’t see this past week coming at all. When this past week was all said and done, it was hard to discern that anything had actually happened.

When this past week was all said and done, it was hard to discern that anything had actually happened. While most of the more meaningful companies in the S&P 500 have already reported earnings and new earnings season is barely 7 weeks away, there’s still time to profit from remaining earnings reports coming this week.

While most of the more meaningful companies in the S&P 500 have already reported earnings and new earnings season is barely 7 weeks away, there’s still time to profit from remaining earnings reports coming this week.