Most of us have, at one time or another believed that we were carrying the weight of the world on our shoulders. The reality will always be that unless we are the President of the United States with a decision to be made regarding pressing that red button, those feelings are somewhat exaggerated and unlikely to be borne out in fact.

Most of us have, at one time or another believed that we were carrying the weight of the world on our shoulders. The reality will always be that unless we are the President of the United States with a decision to be made regarding pressing that red button, those feelings are somewhat exaggerated and unlikely to be borne out in fact.

It’s probably not an exaggeration, however, to suggest that in the past week the burden of the world weighed down heavily on the U.S. stock markets.

Slowing growth and questionable economic statistics from China and an unfolding crisis in Crimea were the culprits identified this week that sapped the momentum out of our markets. The complete list of “reasons” for last week’s performance was compiled by Josh Brown, but ultimately it all came down to our shoulders. Perhaps like a regressive tax the individual investor may feel an exaggerated impact as well when the market behaves badly and may also take longer to recover from the heavy load of losses.

In addition to the global issues then there were also issues of regulation, seeing the SEC and FTC weigh in on Herbalife (HLF), dueling words of umbrage from billionaires over eBay (EBAY) and litigation from the New York State Attorney General’s Office over General Motor’s (GM) role in potentially avoidable vehicular deaths.

What there wasn’t was anything positive or optimistic to be said during the week, other than sooner or later Spring will arrive. For the first time since the last real attempt at a correction nearly two years ago the market closed lower in each trading session of the past week.

While the weekend may change my opinion, as additional news may be forthcoming as Russian war games on Ukraine’s borders play themselves out and a Crimean referendum is held, I find myself optimistic for the coming week.

I usually try to find ten potential trades for each coming week. Last week I struggled to find just nine. This week my preliminary list was nearly twenty and I had a difficult time narrowing down to ten stocks.

That hasn’t happened in a while.

Certainly, as has been discussed in previous weeks following a downward moving market, the challenge is discerning between value and value traps. In that regard this past week is no different, but for inspiration, I look to the option seller’s best friend.

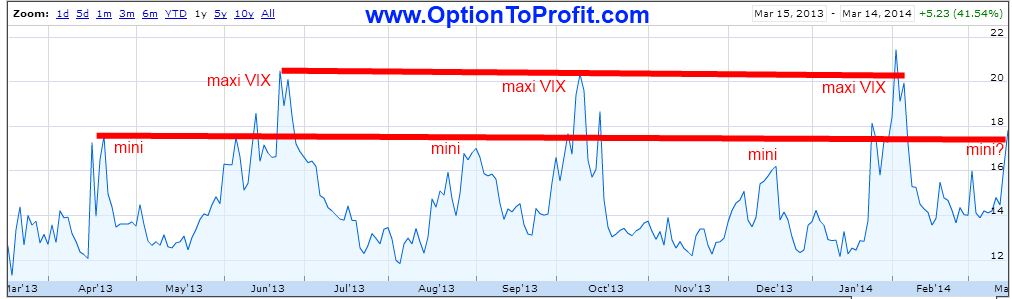

That would be volatility. It creates the kind of premiums that can make me salivate and it is the lack of volatility that makes me wonder whether anyone really cares anymore about the need for stock markets to react appropriately to fundamental factors, as opposed to simply moving higher under all circumstances.

Since late 2011 we’ve been used to seeing historically low levels of volatility with occasional spikes representing market downturns. For those following along you know that there haven’t been many of those downturns in the past 20 months, although we did just recently quickly recover from an equally quick 7% loss. Those downturns saw spikes in volatility.

Suddenly there has been a lot of discussion about increasing volatility and for those that get excited about technical analysis, much is made of the significance of Volatility Index breaking above the 200 Day Moving Average.

What you don’t hear, however, are the video playbacks of all of the times the Volatility Index has surpassed that 200 Day Moving Average and it did not lead to a market breakdown, as suggested by many.

What you don’t hear, however, are the video playbacks of all of the times the Volatility Index has surpassed that 200 Day Moving Average and it did not lead to a market breakdown, as suggested by many.

Instead, a quick look at the past year seems to indicate an alternating current of spikes in volatility between larger spikes and smaller ones. Simply put, I think we’re experiencing a regularly scheduled smaller spike in volatility.

I could be wrong, but that’s what hedging is all about.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend and Momentum categories, with no “PEE” selections this week (see details).

As with last week, despite the uncertainty that may usher in the coming week I see some possibilities even with some higher beta positions, on a selective basis.

While I’ve been trying to emphasize dividend paying positions for the past three months, the only potential such trades that had any appeal for me this week fell into the higher beta category.

While Best Buy (BBY) is probably immune to any direct impact from an overseas crisis, it has had no difficulty in creating its own and has certainly created a crisis of faith before regaining some respectability under new leadership. But for those that have held shares that all seems so long ago after some disappointing earnings reports. Hit especially hard this most recent earnings season, Best Buy has two months left to acquit itself and another two weeks to have their cash registers ring loudly to offset any weather related disappointments. In the meantime shares do go ex-dividend this week and have been trading in a narrow range of late. In the absence of any news it may be expected to keep doing so long enough to capture a dividend and perhaps a premium or two.

Las Vegas Sands (LVS) also goes ex-dividend this week and is also a higher beta stock. While I have traded this stock w

ith some frequency, it’s been a while since doing so as it resists going much lower. While it is at a relative low to its recent high after a 7% decline, it has still had a fairly uninterrupted trajectory. Like Best Buy, there’s not too much reason to suspect that events in Crimea will serve as a direct contagion, the higher beta may be its own heavy weight in the event of a market decline, but like cockroaches, gambling will survive even nuclear holocaust, as may Sheldon Adelson, the Chairman. It may also survive some weakness in China, as there’s no better place to bury your misery than in their Maxao casinos.

It’s usually a fallacy in the making when you use logic to convince yourself of the rationale to buy a stock. That includes the belief that if you liked a stock at one price it must certainly be even more likeable at a lower price. Yet that’s where I find myself with General Electric (GE), whose shares were just assigned from me a week ago and now find themselves priced below that earlier strike price. However, in the case of General Electric, unless there are some horrific surprises around the corner or a complete market meltdown, it’s hard to imagine that it could be classified as being a value trap at this new lower price. Down 4% in the past week and 10% YTD, if the market is heading lower, GE will have been ahead of the curve. While it’s option premium doesn’t reflect much in the way of volatility it does represent a reasonable means to surpass the performance of a flat market.

While retail has been a place that money has gone to die of late, you get a feeling that things may be reversing, at least in the minds of analysts when even Coach (COH), a literal punching leather bag for all, receives an upgrade. While my shares of Coach were assigned this week, as were my shares of Kohls (KSS), I’m ready to repurchase both in their current range, as the long fall down deserves at least a short climb higher.

Coach has shown itself to be able to faithfully defend the $46 level despite so many assaults over the past two years. That ability to consistently bounce back has made it a great covered option position, whether through outright purchase or the sale of puts.

Kohls represents exactly what I like in my stocks. That is a non-descript existence and just happily going along its way without making too much fuss, other than an occas�ional earnings related outburst. Dependable is far more important than being flashy and as a stock and as a company, Kohls hugs that middle lane reliably, but still provides a competitive premium thanks to those occasional outbursts.

If the thesis that retail is ready for a comeback has more of a basis than just as reflected in share price, but also reflects pent up spending from a harsh winter, MasterCard (MA) is a prime beneficiary. While already somewhat protected from the ravages of weather by virtue of being able to spend your money with just a simple mouse click, there are just some things that need to be done in the real world. Trading well below its pre-split price until recently I had not owned shares in years. Now more readily purchased in scale, I look forward to the opportunity to purchase and re-purchase these shares with some degree of regularity, WHile its dividend is paltry, there is certainly room for growth to rise to the levels of Visa (V) and Discover Financial Services (DFS). However, notwithstanding any potential bump in share price along with a dividend hike, the option premiums can make the wait worthwhile.

In a week of no industry specific news, following a flurry of changes in industry dynamics initiated by T-Mobile (TMUS), Verizon (VZ) fell 3% bringing it down to a level from which it has found significant strength.� While General Electric may face some potential liability with events in Crimea or a deteriorating economy in China, I don’t see quite the same �liability for Verizon. Instead, whatever burdens it has to carry will come from an increasingly competitive landscape as it and AT&T (T) are continually pushed by T-Mobile and perhaps Sprint (S). In the meantime, while trading in a range and finding support at $46, there’s always the additional lure of a 4.5% dividend.

While Verizon isn’t terribly exciting it meets its match in Intel (INTC)�. However, the excitement that comes from growth isn’t absolutely necessary to generate predictable profits. Intel is especially well suited when it’s share price is very close to a strike level. If volatility continues to rise the opportunity to purchase Intel expands as the price range at which it may be purchased increases, while still offering an attractive option premium which can be further enhanced by an attractive dividend.

While it was only a matter of time until retail would begin to dig its way out from under the piles of snow, no sector has brutalized me more this past year than the one that requires digging. Freeport McMoRan (FCX) is among that group that hasn’t been terribly kind to me, despite my belief that it would be the “stock of the year” for 2013.

With copper itself being brutalized this past week, despite gold’s relative strength, Freeport McMoRan has itself had the weight of the market’s response to the less than robust Chinese economy to shoulder. But the one thing that you can always count on is that data from China can easily correct reality and that explains the seemingly recurrent see-saw ride that we have been on in those sectors that are tied to their data. The true plunge in copper prices, if sustained, will not be good news for Freeport McMoRan, whose generous dividend payout could conceivably be jeopardized.

On the other hand, shares are now at a level that has repeatedly created substantial returns for those willing to test the waters.

Finally, not many companies, especially those with a newly appointed CEO had as bad a week as General Motors. You might think that having paid its first dividend in years this past Friday there would be reasons to rejoice, but finding yourself at the top of the headlines related to customer deaths isn’t an enviable place, nor one conducive to a thriving share price. When the Attorney General of any state piles on that doesn’t help.

However, with a chorus of those clamoring for General Motors to re-test the $30 level purely on a technical basis there may be reason enough to believe that won’t be the case. Having timed a purchase of shares as inopportunely as possible, I’d like nothing more than to see that position restored to some respect.

As with the recent news that the FTC will b

e investigating allegations that Herbalife was engaged in a Ponzi scheme, the bad news for General Motors, while coming as an acute event, will take a long while to play out, regardless of the merits of the cases or the human tragedies caught up in what is now a story of fines, punishment andperhaps even acquittal.

Traditional Stocks: Coach, General Electric, General Motors, Intel, Kohls, MasterCard, Verizon

Momentum Stocks: Freeport McMoRan

Double Dip Dividend: Best Buy (ex-div 3/18), Las Vegas Sands (ex-div 3/18)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

I’m not entirely certain I understood what happened on Friday.

I’m not entirely certain I understood what happened on Friday. The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story.

The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story. I really didn’t see this past week coming at all.

I really didn’t see this past week coming at all.