Somehow you find the strength.

Somehow you find the strength.

Having spent many years working with children and in children’s hospitals, I often wondered how parents of children with significant medical or developmental disabilities found the strength to go from one day to the next.

When faced with what appear to be insurmountable challenges some people can simply face down the insurmountable and move forward when even treading water seems impossible.

Doubly difficult must be dealing with brief glimmers of hope that can dissolve away. The ascent to emotional highs quickly followed by emotional lows certainly has to take its toll.

My wife has told me on many occasions “you just find the strength.” Ordinary people rise to the occasion to accomplish extraordinary things. Even at its bleakest such people could see positive value from their efforts and see justification in optimism and resolve.

To suggest that the stock market presents challenges similar to those faced by parents faced the most difficult of circumstances trivializes the amazing dedication that people can summon.

But that doesn’t stop me for making the suggestion.

With the market having considerably changed its behavior it’s difficult to know what actions to take and when to temper optimism with remembrances of earlier setbacks. It’s easy to get paralyzed with fear and uncertainty, just as it’s easy to get elated about unexpected good news. But somehow you have to go on as dispassionately as possible even in the face of what may be a relative meltdown, which a month ago might have meant a week where the market only advanced by 1%.

I’m not really certain what the “7 Signs of the Apocalypse” are, but I feel fairly certain that the sudden onset of alternating triple digit gains and losses, in addition to the large intra-day reversals are among the signs of darkness ahead. The trend line may say differently, but that is the perennial battle between darkness and light.

The reaction to today’s Employment Situation Report was fascinating in that the fear of a related market plummet was so prevalent that even the release of numbers that simply met expectations was viewed as incredibly hopeful that the fully anticipated Federal Reserve tapering wouldn’t be coming as soon as some thought. As reviled as Quantitative Easing has been among some circles, the very thought of its withdrawal from the credit markets created seizure like activity in the markets. Once addicted, it’s difficult to accept that fact and you always want more.

As the market began its mid-day ascent on Thursday, reversing a large fall at that point that the cumulative drop from the recent intra-day high on May 21, 2013 was nearly 5%, it had recovered 62% of that fall on an intra-day basis. Is that the same quick head fake that we saw in April 2012 just prior to the market losing 9%?

I will know in hindsight, but whatever awaits, somehow you still have to go on, recognizing that the stock market continues to be the best place to put your faith when it comes to advancing wealth creation. Of course, the across the board rally in prices on Friday increases the difficulty of selecting stocks that may have some unreleased energy within.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details). As opposed to previous week’s I have more “Momentum” possibilities and fewer dividend selections. I’m not entirely comfortable with that breakdown.

Less than a day before the market’s wild ride in response to the Employment Situation Report, a barely 3 days after the disappointing ISM Manufacturing Index report, Fastenal (FAST), a company whose fortunes many consider to be a very basic reflection of manufacturing health, reported some disappointing data, which seemed suggestive of a manufacturing slowdown and certainly a confirmation of the ISM statistics. It’s fall was drastic, but it recovered along with everyone else on Friday. As long as disbelief may be suspended, or at least data may be denied, Fastenal remains a company that has been reliable in maintaining value or returning to it.

With Merck’s (MRK) recent rise higher following the ASCO meeting and speculation that it may split off component pieces, it’s shares don’t fit my recent pattern of looking for companies that have under-performed the S&P 500 since its recent top. It does, however, go ex-dividend this week and the combination of premium and dividend may offer enough of a cushion in the event of some interim correction, particularly if selling monthly options. For those that like to think longer term than I am capable of doing, Merck probably has the best pipeline of all of the major pharmaceutical companies, although my horizon doesn’t usually go much beyond a month.

Certainly not for the faint-hearted, especially at a time that the market itself may be somewhat tenuous, is Apple (AAPL), which hosts the Worldwide Developer’s Conference next week. As it is, this past week was already a busy one for Apple, already fresh off the congressional testimony victory tour over its tax related strategies. Whether it caught attention because of its ongoing e-book publishing battles, its potential entry into the internet radio space, its plan to accept iPhone trade-ins, its patent for electronic payments or its proposed use of advertising on various platforms, it was hard to escape Apple-centric news. As it is, lots more eyes will be on Apple this week. There’s not too much to be gained by adding to the speculation over what will be presented, but I think that it’s very likely shares will out-perform the market for the week. The options market is expecting a nearly 4% move in shares, which to me indicates expectations of a surprise or disappointment. Either way, at a very rich option premium and some resistance at about $395, this seems like a good time to add or buy shares.

Marathon Oil (MRO) requires much less of the ability to withstand outrageous and frequent moves in share price. as with many of the stocks that I’m considering for the coming week, their price movement on Friday made them a little less appealing; sometimes a lot less appealing. In Marathon Oil’s case the move higher still lefty it in the range that still leaves me with some comfort.

Transocean (RIG) is a little more of a nail biter stock on some occasions and is currently among the increasing number of companies that have caught Carl Icahn’s attention. It recently re-instituted its dividend after having gotten out from under the Deepwater Horizon liabilities and has traded well even when eliminating the dividend. It no longer offers weekly contracts so I haven’t been looking toward it quite as much as a potential choice. However, as I’ve been looking increasingly to position myself defensively, the longer term contracts have greater utility during a brief market downturn.

Dow Chemical (DOW) was one of the stocks I was prepared to buy last week, but eventually as the week came to its end, I only followed through on two of the list’s stocks. Following some sector news last week shares fell a bit and that should have been the invitation to add shares, but overall caution was my prevailing theme. Although the caution still continues, I’m more inclined to add shares in reliably performing companies. FOr Dow Chemical, if shares are not assigned, it does go ex-dividend in the first week of the July2013 cycle, which adds some further appeal.

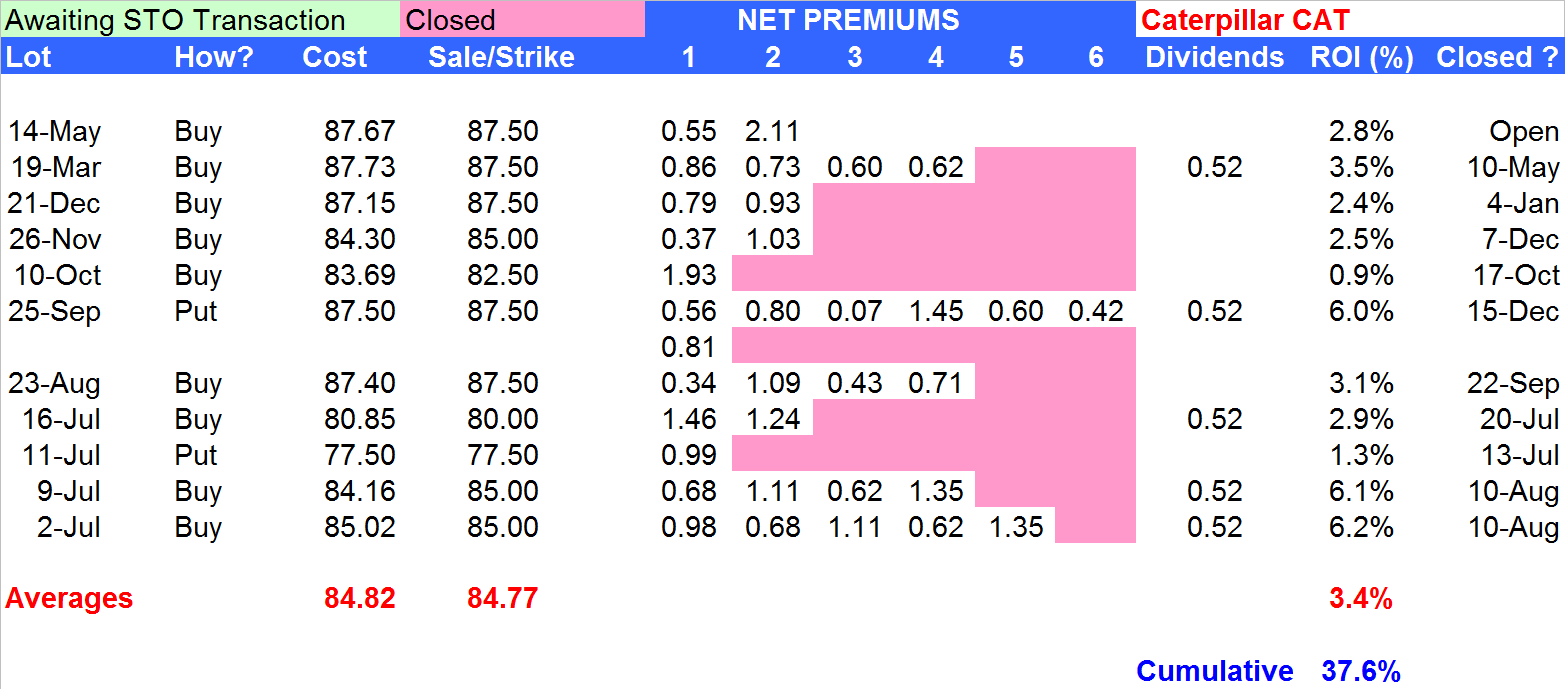

Both Caterpillar (CAT) and Joy Global (JOY) have had their recent ups and downs. Both have also been excellent choices when beginning to test their bottoms. Both levered to some degree to Chinese economic expansion, Joy Global recently gave some reason to believe that its business could do well even if frank expansion didn’t occur, as miners were looking to retire older and more expensive mines while developing newer, more cost efficient ones, thereby requiring heavy machinery products. As much as you can count on any guidance and any interpretation of events that are not within your control both Caterpillar and Joy Global have the ability to withstand economic cycle blips.

Motorola Solutions (MSI) certainly fits within the theme of looking for recent under-performers. In this case, it’s thanks to its large drop following its most recent earnings report in April. While it goes ex-dividend this week it won’t report its next earnings until the August 2013 option cycle and although I’m most likely to sell a June 2013 option, I may also consider looking at the July 2013 option premiums.

LuLu Lemon (LULU) reports earnings this week and certainly will serve as a future case study at business schools around the country for how to effectively deal with a crisis that could potentially imperil brand integrity. The shares are no stranger to big moves in response to news and have appreciated nearly 30% since the product news became known. That’s probably a bit too much for anything other than a speculative kind of trade in advance of earnings, but at the moment anything less than an 8% drop in share price could result in obtaining a 1% ROI if puts are sold.

I’ve never invested in ULTA Salon (ULTA) before, but have begrudgingly gone into its stores. The options market is implying about a 9% move as earnings are due to be announced this week. That certainly wouldn’t be the first time its shares have responded to that degree. The reward profile for selling puts on these shares is marginally within the range that I consider, with the ability to obtain a 1% return in exchange for accepting anything less than a 12% share drop, but unlike the LuLu Lemon case, that return is over a two week period of exposure, as opposed to just one. While there is a possibility of following this trade, I would be much more likely to do so if shares have some significant dips before earnings are released.

Finally, TIVO (TIVO) which was scheduled to start jury selection in its patent infringement case this coming week spiked more than 10% in the final 30 minutes of trading on Thursday, in the absence of any publicly available news. By Friday morning it’s shares fell nearly 20% on the news that it had reached a settlement. Perhaps the amount was less than anticipated, but I interpreted the remainder of the press release as short term bullish for shares which included a doubling of the share buyback and news of continued partner relationships. The money and the contracts may come in handy for a company that is proof that a lost subscriber here and a lost subscriber there begins to add up.

Traditional Stocks: Caterpillar, Dow Chemical, Transocean

Momentum Stocks: Apple, Joy Global, TIVO

Double Dip Dividend: Merck (6/13), Motorola Solutions (6/12)

Premiums Enhanced by Earnings: LuLu Lemon (6/10 PM), Ulta (6/11 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.