It seems that almost every week over the past few months have both begun and ended with a quandary of which path to take.

It seems that almost every week over the past few months have both begun and ended with a quandary of which path to take.

Talk about indecision, for the previous seven weeks the market closed in the an alternating direction to the previous week. This past week was the equivalent of landing on the “green” as the S&P 500 was 0.12 higher for the week, but ending the streak.

Like the biology experiment that shows how a frog immersed in water that is slowly brought to a boil never perceives the impending danger to its life, the market has continued to set new closing record high after record high in a slow and methodical fashion.

With all the talk continuing about how money remains on the sidelines from 2008-9, you do have to wonder how getting into the market now is any different from that frog thinking about climbing into that pot as it nears its boiling point.

Unless there’s new money coming in what fuels growth?

That’s not to say that danger awaits or that the slow climb higher will lead to a change in state or a frenzied outburst of energy leading to some calamitous event, but the thought could cross some minds.

Perhaps Friday’s sell off will prompt some to select one path over another, although a single bubble doesn’t mean that as you’re immersed in a bath that it is coming to a boil. It may entirely be due to other reasons, such as your most recent meal, so it’s not always appropriate to jump to conclusions.

While the frog probably doesn’t really comprehend the slowly growing number of bubbles that seem to be arising from the water, investors may begin to notice the rising number of IPO offerings entering the market and particularly their difficulty in achieving pricing objectives.

I wonder what that might signify? The fact that suddenly my discount brokerage seems to be inundating me with IPO offers makes me realize that it does seem to be getting hotter and hotter around me.

This coming week I’ve had cash reserves replenished with a number of assignments, somehow surviving the week ending plunge and I see many prices having come down, even if just a little. That combination often puts me into a spending mood, that would be especially enhanced if Monday begins either on the downside or just tepidly higher.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories.

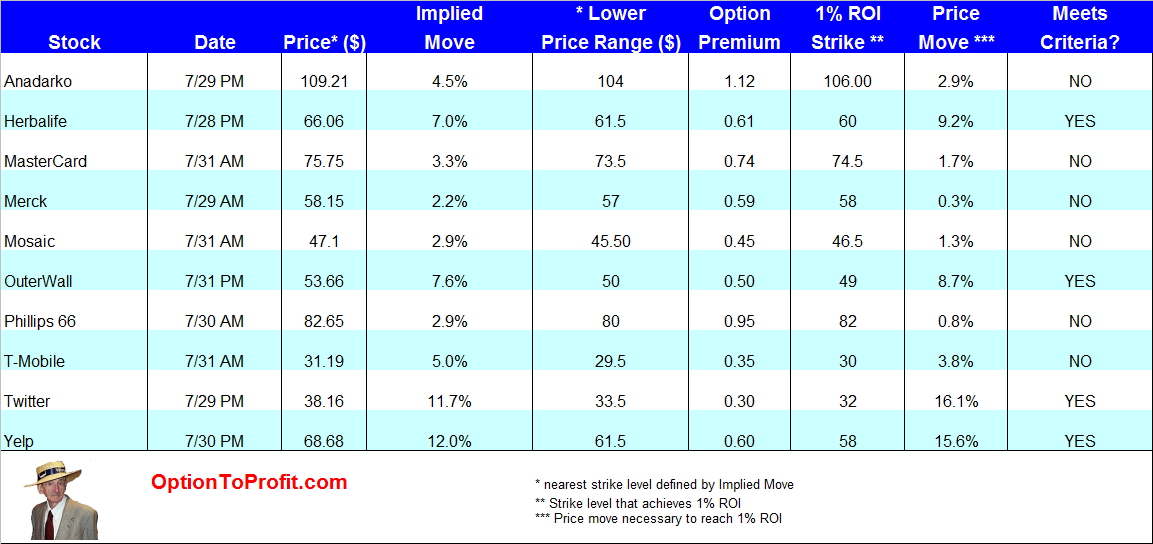

The big news in the markets this week was Facebook (FB) as its earnings report continued to make clear that it has mastered the means to monetize a mobile strategy. While it produces nothing it’s market capitalization is stunning and working its way closer to the top spot. For those in the same or reasonably close sector, the trickle down was appreciated. One of those, Twitter (TWTR) reports earnings this week and the jury is still very much out on whether it has a viable product, a viable management team and even a viable life as an independent entity.

For all of those questions Twitter can be an exciting holding, if you like that sort of thing. I currently hold shares that were assigned to me after having fallen so much that I couldn’t continue the process of rolling over puts any longer. The process to recover has been slow, but speeded a bit by selling calls on the way higher. However, while that has been emotionally rewarding, but as may be the case when puts are sold and potential ownership is something that is shunned, has required lots of maintenance and maneuvering.

With earnings this week the opportunity arises again to consider the sale of new Twitter puts, either before earnings are released or if shares plunge, afterward.

The option market is implying an 11.7% move in shares upon earnings. a 1% weekly ROI may possibly be obtained at a strike price that’s 14.8% below Friday’s close.

While Twitter is filled with uncertainty, Starbucks (SBUX) has some history behind it that gives good reason to have continuing confidence. With the market having looked adversely at Starbucks’ earnings report, Howard Schultz gave an impassioned and wholly rational defense of the company, its operations and prospects.

In the past few years each time Starbucks shares have been pummeled after earnings and Schultz has done as he did on Friday, it has proven itself an excellent entry point for shares. Schultz has repeatedly shown himself to be among the most credible and knowledgeable of CEOs with regard to his own business and business strategy. He has been as bankable as anyone that can be found.

With an upcoming dividend, always competitive option premiums and Schultz standing behind it, the pullback on Friday may be a good time to re-consider adding shares, despite still trading near highs.

While I suppose Yelp (YELP) could tell me all about the nearest Starbucks and the experience that I might expect there, it’s not a site that gets my attention, particularly after seeing some reviews of restaurants that pilloried the businesses of places that my wife and I frequent repeatedly.

Still, there’s clearly something to be had of value through using the site for someone. What does have me interested is the potential opportunity that may exist at earnings. Yelp is no stranger to large moves at earnings and for those who like risk there can be reward in return. However, for those who like smaller dosages of each a 1% ROI for the week can potentially be achieved at a strike price of $58 based on Friday’s $68.68 closing priced and an implied move of 12%. Back in April 2014 I received an almost 3% ROI for the risk taken, but don’t believe that I’m willing to be so daring now that I’m older.

Following the market’s sharp drop on Friday it was difficult to not jump the gun a little bit as some prices looked to be either “too good” or just ready. One of those was General Motors (GM). Having survived earnings last week,

albeit with a sizeable share drop over the course of a few days and wading its way through so much litigation, it is quietly doing what it is supposed to be doing and selling its products. An energized consumer will eventually trade in those cars that have long passed their primes, as for many people what they drive is perceived as the best insight into their true standing in society. General Motors has traded nicely as it has approached $33 and offers a nice premium and attractive dividend, making it fit in nicely with a portfolio that tries to accentuate income streams even while shares my gyrate in price.

I never get tired of thinking about adding shares of eBay (EBAY). With some of my shares assigned this past Friday despite some recent price strength after earnings, I think it is now in that mid-point of its trading range from where it has been relatively easy to manage the position even with some moves lower.

Carl Icahn has remained incredibly quiet on his position in eBay and my guess, based on nothing at all, is that there is some kind of behind the scenes convergence of thought between Icahn and eBay’s CEO, John Donahoe, regarding the PayPal jewel.

With all of the recent talk about “old tech,” there’s reason to consider one of the oldest, Texas Instruments (TXN) which goes ex-dividend this coming week. Having recently traded near its year’s high, shares have come down considerably following earnings, over the course of a few days. While still a little on the high side, it has lots of company in that regard, but at least has the goods to back up its price better than many others. It, too, offers an attractive combination of dividend, premiums and still possibility of share appreciation.

Reporting earnings this week are both MasterCard (MA) and MetLife (MET). Neither are potential trades whose premiums are greatly enhanced by the prospects of earnings related surprises. Both, however, are companies that I would like to once again own, possibly through the sale of put options prior to earnings being announced.

MasterCard suffered on Friday as collateral damage to Visa’s (V) earnings, which helped drag the DJIA down far more than the S&P 500, despite the outsized contribution by Amazon (AMZN) which suffered a % decline after earnings. On top of that are worries again from the Russian market, which earlier in the year had floated the idea of their own credit system. Now new rules impacting payment processors in Russia is of concern.

MasterCard has been able to generate satisfactory option premiums during an otherwise low volatility environment and despite trading in a $72 – $78 range, as it has regular bounces, such as seen this past week.

I have been waiting for MetLife to trade down to about the $52 range for the past two months and perhaps earnings will be the impetus. Fo�r that reason I might be more inclined to consider opening a position through the sale of puts rather than an outright buy/write. However, also incorporated into that decision process is that shares will be going ex-dividend the following week and there is some downside to the sale of puts in the face of such an event, much as their may be advantage to selling calls into an ex-dividend date.

Finally, there hasn’t been much that has been more entertaining of late than the Herbalife (HLF) saga. After this past week’s tremendous alternating plunge and surge and the absolute debacle of a presentation by Bill Ackman that didn’t quite live up to its billing.

While there may certainly be lots of validity to Ackman’s claims, which are increasingly not being nuanced, the opportunity may exist on both sides of the controversy, as earnings are announced next week. Unless some significant news arises in addition to earnings, such as from the SEC or FTC, it is like any other high beta stock about to report earnings.

The availability of expanded weekly options makes the trade more appealing in the event of an adverse move bringing shares below the $61.50 level suggested by the implied volatility, allows some greater flexibility. However, because of the possibility of other events, my preference would be to have this be as short term� of a holding as possible, such that if selling puts and seeing a rise in shares after earnings, I would likely sacrifice remaining value on the options and close the position, being happy with whatever quick profits were achieved.

Traditional Stocks: eBay, General Motors, MasterCard, MetLife, Starbucks

Momentum: none

Double Dip Dividend: Texas Instruments (7/29)

Premiums Enhanced by Earnings: Herbalife (7/28 PM), Twitter (7/29 PM), Yelp (7/30 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.