Subscribers to Option to Profit received preliminary notification of this week’s stock selections on Friday, September 25th, 8:00 AM EDT and updated at 10:20 AM. The full article was distributed on Saturday, at 11:25 AM)

I doubt that Johnny Cash was thinking about that thin line that distinguishes a market in correction from one that is not.

jhgty

For him, walking the line” was probably a reference to maintaining the correct behavior so that he could ensure holding onto something of great personal value.

Sometimes that line is as clear as the difference between black and white and other times the difference can be fairly arbitrary.

Lately our markets have been walking a line, not necessarily borne out of a clear distinction between right and wrong, but rather dancing around the definition of exactly what constitutes a market correction, going in and out without much regard.

The back and forth dance has, to some degree, been in response to mixed messages coming from the FOMC that have left the impression of a divergence between words and actions.

Regardless, what is at stake can hold some real tangible value, despite a stock portfolio not being known for its ability to keep you warm at night. Indirectly, however, the more healthy that portfolio the less you have to think about cranking up the thermostat on those cold and lonely nights.

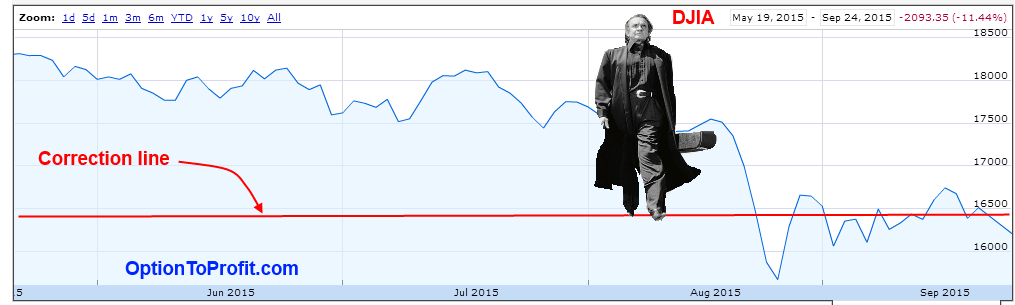

It had been a long, long time since being challenged by that arbitrary 10% definition, but ever since having crossed that line a month ago there’s been lots of indecision about which direction we were heading.

This week was another good example of that, just as the final day of the week was its own good example of the back and forth that has characterized markets.

Depending on your perspective our recent indecision about which side of the line we want to be on is either creating support for a launching pad higher or future resistance to that move higher.

When you think about the quote attributed to Jim Rogers, “I have never met a rich technician,” you can understand, regardless of how ludicrous that may be, just how true it may also be.

While flipping a coin may have predictable odds in the long term, another saying has some real merit when considering the difficulty in trying to interpret charts and chart patterns,

That is “the market can stay irrational far longer than you can stay liquid.” Just a few wrong bets in succession on the direction can have devastating effects.

The single positive from the past 10 days of trading, however, is that the market has started behaving in a rational manner. It finally demonstrated that it understood the true meaning of a potential interest rate hike and then it reacted as a sane person might when their rational expectation was dashed.

Part of the indecision that we’ve been displaying has to be related to what has seemed as a lot of muddled messages coming from the FOMC and from Federal Reserve Governors. One minute there are hawkish sentiments being expressed, yet it’s the doves that seem to be still holding court, leading onlookers to wonder whether the FOMC is capable of making the decision that many believe is increasingly overdue.

In a week where there was little economic news we were all focused on personalities, instead and still stewing over the previous week’s unexpected turn of events.

It was a week when Pope Francis took center stage, then Chinese President Xi trying to cozy up to American business leaders before his less welcoming White House meeting, and then there was finally John Boehner.

The news of John Boehner’s early departure may be the most significant of all news for the week as it probably reduces the chance of another government shutdown and associated headaches for all.

It also marked something rare in Washington politics; a promise kept.

That promise of strict term limits was included in the “Contract with America” and John Boehner was a member of that incoming freshman Congressional Class of 1995 running on that platform, who has now indicated that he will be keeping that promise after only 11 terms in office.

None of that mattered for markets, but what did matter was Janet Yellen’s comments after Thursday’s market close when she said that a rate hike was likely this year and that overseas events were not likely to influence US policy.

That was something that had a semblance of a definitive nature to it and was to the market’s liking, particularly as the coming week may supply new economic information to justify the interest rate hawks gaining control.

Friday’s revised GDP data indicating a 3.9% growth rate for the year is a start, as the coming week also bring Jobless Claims, the Employment Situation Report and lots of Federal Reserve officials making speeches, including more from Janet Yellen, who had been reclusive for a while prior to the September meeting and Vice Chair Stanley Fischer.

As a prelude to the next earnings season that begins in just 2 weeks, the stage could be set for an FOMC affirmation that the economy is growing sufficiently to begin thinking about inflation for the first time in a long time.

After being on the other side of the inflation line for a long time and seeing a lost generation in Japan, it will feel good to cross over even as old codgers still dread the notion.

Both sides of the line can be the right side, but not at the same time. Now is the time to get on the right side and let rising interest rates reflect a market poised to move higher, just as low interest rates subsidized the market for the past 6 years. However, as someone who likes to sell options and take advantage of this increased volatility, I welcome continued trading in large bursts of movement up and down, as long as that line is adhered to.

Since the mean can always be re-calculated based on where you want to start your observations, this reversion to the new mean, that just happens to be 10% below the peaks of the summer, can be a great neighborhood to dance around.

As usual, the week’s potential stock selections are classified as being in the Traditional, Double Dip Dividend, Momentum or “PEE” categories.

Last week I was a little busier than has been the usual case of late with regard to opening new positions. Following the sharp sell offs to end the previous week I had a reasonably good feeling about the upcoming week, but now feel fortunate to have emerged without any damage.

I don’t feel the same level of optimism as the new week is set to begin, but there really is no reason to have much conviction one way or another, although there appears to be a more hawkish tone in the air as Janet Yellen is attempting to give the impression that actions will be aligned with words.

With the good fortune of getting some assignments as the week came to its close and having some cash in hand, I would like to build on those cash reserves but still find lots of temptations that seek to separate me from the cash.

The temptations aren’t just the greatly diminished prices, but also the enhanced premiums that accompany the uncertainty that’s characterizing the market.

That uncertainty is still low by most standards other than for the past couple of years, but taking individual stocks that are either hovering around correction or even bear market declines and adding relatively high premiums, especially if a dividend is also involved, is a difficult combination to walk away from.

The stocks going ex-dividend in the upcoming week that may warrant some attention are EMC Corporation (EMC) and Cisco (CSCO).

I own shares of both and both have recently been disappointing, Cisco, after its most recent earnings report looked as if it was surely going to be assigned away from me, but as so many others got caught up in the sudden downdraft and has fallen 14% since earnings, without any particularly bad news. EMC for its part has dropped nearly 13% in that same time period.

As is also so frequently the case as option premiums are rising, those going ex-dividend may become even more attractive as an increasing portion of the share’s price drop due to the dividend gets subsidized by the option premium.

That is the case for both Cisco and EMC. In the case of EMC, when the ex-dividend is early in the week you could even be excused for writing an in the money call with the hope that the newly purchased shares get assigned, as you could still potentially derive a 1% ROI on such a trade, yet for only a single day of holding.

Cisco, which goes ex-dividend later in the week may be a situation where it is warranted to sell an expanded weekly option for the following week that is also in the money by greater than the amount of the dividend, again in an effort to prompt an early assignment.

Doing so trades off the dividend for additional premium and fewer days of holding so that the cash may potentially be recycled into other income generating positions.

On such position is Comcast (CMCSA) which is ex-dividend the following Monday and if assigned early would have to be done so at the conclusion of this week.

While the entire media landscape in undergoing rapid change and while Comcast has positioned itself as best as it can to withstand the quantum changes, a trade this week is nothing more than an attempt to exploit the shares for the income that it may be able to produce and isn’t a vote of confidence in its strategic initiatives and certainly not of its services.

The intention with Comcast is considering the sale of an in the money October 9 or October 16, 2015 call and as with Cisco or EMC, consider forgoing the dividend.

However, for any of those three dividend related trades, I believe that their prices alone are attractive enough and their option premiums enhanced enough, that even if not assigned early, they are in good position to be candidates for serial sale of call options or even repurchases, if assigned.

As long as considering a Comcast purchase, one of my favorites in the sector is Sinclair Broadcasting (SBGI). I currently own shares and most often consider initiating a new position as an ex-dividend date is approaching.

That won’t be for a while, however, the second criteria that I look at is where its price is relative to its historical trading range and it is currently below the average of my seven previous purchases in the past 16 months.

While little known, it is a major player in the ancient area of terrestrial television broadcasting and has significant family ownership. While owners of Cablevision (CVC) can argue the merits or liabilities of a closely held public company, the only real risk is that of a proposal to take the company private as a result of shares having sunk to ridiculously low levels.

I don’t see that on the horizon, although the old set of rabbit ears may be to blame for any fuzzy forecasting. Instead of relying on high technology and still being available the old fashioned way for free viewing, Sinclair Broadcasting has simply been amassing outlets all over the county and making money the old fashioned way.

As I had done with my current lot of shares, I sold some slightly longer term call options, as Sinclair offers only the monthly variety. Since it reports earnings very early in November and will likely go ex-dividend late that month, I would consider selling out of the money calls, perhaps using the December 2015 options in an effort to capture the dividend, the option premium and some capital gains on shares.

While religious and political luminaries were getting most of the attention this past week, it’s hard to overlook what has unfolded before our eyes at Volkswagen (VLKAY). Regulatory agencies and the courts may be of the belief that you can’t spell “Fahrvergnügen,” Volkswagen’s onetime advertising slogan buzzword, without “Revenge.” Unfortunately, for those owning shares in the major auto manufacturer’s, such as General Motors (GM), last week’s news painted with a very broad brush.

General Motors hasn’t been immune to its own bad news and you do have to wonder if society places greater onus and personal responsibility on the slow deaths that may be promoted by Volkswagen’s falsified diesel emissions testing than by the instantaneous deaths caused by faulty lock mechanisms.

For its part, General Motors appears to really be bargain priced and will likely escape the continued plastering by that broad brush. With an exceptional option premium this week, plumped up by the release of some sales data and a global conference call, GM’s biggest worry after having resolved some significant legal issues will continue to be currency exchange and potential weakness in the Chinese market.

With earnings due to be reported on October 21st, if considering a purchase of General Motors shares, I would think about a weekly or expanded weekly option sale, or simply bypassing the events and going straight to December, in an effort to also collect the generous dividend and possibly some capital gains while having some additional time to recover from any bad news at earnings.

MetLife (MET) is a stock that is beautifully reflective of its dependency on interest rates. As rates were moving higher and the crowd believed that would go even higher, MetLife followed suit.

Of course, the same happened when those interest rate expectations weren’t met.

Now, however, it appears that those rates will be getting a boost sooner, rather than later, as the FOMC seems to be publicly acknowledging its interests in a broad range of matters, including global events and perhaps even stock market events.

With a recently announced share buyback, those shares are now very attractively priced, even after Friday’s nearly 2% gain.

With earnings expected at the end of the month, I would consider the purchase of shares coupled with the sale of some out of the money calls, hoping to capitalize on both capital gains and bigger than usual option premiums. In the event that shares aren’t assigned prior to earnings, I would consider then selling a November 20 call in an effort to bypass earnings risk and perhaps also capture the next dividend.

Finally, I’ve been anxious to once again own eBay (EBAY) and have waited patiently for its price to decline to a more appealing level. While most acknowledge that eBay gave away its growth prospects when it completed the PayPal (PYPL) spin-off, it has actually out-performed the latter since that spin-off, despite being down nearly 12%.

While eBay isn’t expected to be a very exciting stock performer, it hadn’t been one for years, yet was still a very attractive covered option trading vehicle, as it’s share price was punctuated by large moves, usually earnings related. Those moves gave option buyers a reason to demand and a reason for sellers to acquiesce.

That hasn’t changed and the volatility induced premiums are as healthy as they have been in years. As that volatility rises in the stock and in the overall market, there’s more and more benefit to be gained from selling in the money options both for enhanced premium and for downside protection.

It would be good to welcome eBay back into my portfolio. Even if it won’t keep me warm, I could likely buy someone else’s flea bitten blanket at a great price, using its wonderful services.

Traditional Stocks: eBay, General Motors, MetLife, Sinclair Broadcasting

Momentum Stocks: none

Double-Dip Dividend: Comcast (10/5 $0.25), Cisco (10/1 $0.21), EMC Corp (9/29 $0.12)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable – most often coupling a share purchase with call option sales or the sale of covered put contracts – in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week, with reduction of trading risk.

It wasn’t too long ago that China did what it continues to believe that it does best.

It wasn’t too long ago that China did what it continues to believe that it does best.

In an age of rapidly advancing technology, where even Moore’s Law seems inadequate to keep up with the pace of advances, I wonder how many kids are using the same technology that I used when younger.

In an age of rapidly advancing technology, where even Moore’s Law seems inadequate to keep up with the pace of advances, I wonder how many kids are using the same technology that I used when younger. No matter how old you are, people love getting gifts.

No matter how old you are, people love getting gifts.

The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story.

The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story.