There’s a lot of confusion over who was responsible for the idea that time is merely an illusion and that it is “nature’s way of preventing everything from happening all at once.”

There’s a lot of confusion over who was responsible for the idea that time is merely an illusion and that it is “nature’s way of preventing everything from happening all at once.”

The first part of the idea is certainly thought provoking and is beyond my ability to understand. The second part may be some attempt at a higher plane of humor in an attempt to explain the significance of what is beyond the capability of most people.

In essence, if you thought that the time frame described during the first seven days of creation was compressed, some physicists would suggest that it all actually happened all at once and if you had the appropriate vehicle traveling at sufficient speed you would know that first hand.

The humorous quip has been attributed to Albert Einstein, Woody Allen and others. It has also been attributed to theoretical physicist John Archibald Wheeler, who was one of Einstein’s last collaborators, which itself indicates a relative time in Einstein’s career, so it may be unlikely that Wheeler would have described himself in those terms, if he was a real believer.

You might believe that Wheeler’s single degree of separation from Einstein would suggest hat perhaps the true source of the concept would then be Einstein himself. However, Wheeler maintained that he actually saw it scrawled on a men’s room wall in an Austin, Texas cafe, that in theory would have occurred at the same time that Einstein saw the famous Theory of Relativity equation scrawled on the men’s room wall of a Dusseldorf beer garden.

The idea, though, flows from Einstein’s earlier works on time, space and travel and may have been an inspiration to some well read patron while making room for the next idea inducing purchase of a large quantity of beer, wine or spirits.

This past week may have been an example of time forgetting its role, as we saw an avalanche of important news and events that came upon us in quick succession to begin the week. The news of an apparent agreement to the resolution of the Greek debt crisis and the announcement of a deal on Iran’s march toward developing a nuclear weapon came in tandem with the non-event of a melt down of the Chinese stock market.

The majority of the 2.4% weekly gain seen in the S&P 500 was over by the time we could blink, as the rest of the week offered little of anything, but saw a continuing successful test of support in the S&P 500, nearly 5% lower, as it moved to be in a position to now test resistance.

With the near simultaneous occurrence of those important events, the real question may be whether or not they themselves are illusory or at least short-lived.

Time may be the key to tell whether the events of this week were justifiable in creating a market embrace of a rosy future.

We’ve lived through past Greek debt crises before, so there is probably little reason to suspect that this will be the last of them for Greece or even the last we’ll see in the Eurozone. When and where the next flash point occurs is anyone’s guess, but German Finance Minister Wolfgang Schäuble’s comments regarding Greece’s place in the EU continues to leave some uncertainty over the sanctity of that union and their currency.

With an Iranian deal now comes the effort to block it, which itself has a 60 day time limit for Congressional opponents to do their best to defeat the proposal and then overcome a Presidential veto. While it’s not too likely that the latter will become reality, there will be no shortage of attempts to undermine the agreement that probably contributed to continuing weakness in the energy sector in fears that Iranian oil would begin flooding markets sooner than is plausible.

The Chinese attempts at manipulating their stock markets have actually worked far longer than I would have predicted. Here too, time is in play, as there is a 6 month moratorium on the sale of some stocks and by some key individuals. That’s a long time to try and hold off real market dynamics and those forces could very well yet undermine the Chinese government’s “patriotic fight” to save its stock market.

The role that those three may have played in moving the market higher last week may now become potential liabilities until they have stood the test of time.

As usual, the week’s potential stock selections are classified as being in the Traditional, Double Dip Dividend, Momentum or “PEE” categories.

The coming week is very short on scheduled economic news, but will be a very busy one as we focus on fundamentals and earnings.

While there are lots of earnings reports coming this week the incredibly low volatility, after flirting with higher levels just 2 weeks ago, has resulted in few opportunities to try and exploit those earnings reports.

As again approaching all time highs and being very reluctant to chase new positions, I would normally focus on relatively safe choices, perhaps offering a dividend to accompany a premium from having sold call options.

This week, the only new position that may fulfill those requirements is Fastenal (NASDAQ:FAST) which offers only monthly options and reported earnings last week.

It has been mired in a narrow price range since its January 2015 earnings report and is currently trading at the low end of that range. Having just reported earnings in line with estimates is actually quite an achievement when considering that Fastenal has been on a hiring spree in 2015 and has significantly added costs, while revenues have held steady, being only minimally impacted by currency exchange rates.

Their business is a very good reflector of the state of the economy and encompasses both professional construction and weekend warrior customers. They clearly believe that their fortunes are poised to follow an upswing in economic activity and have prepared for its arrival in a tangible way.

At the current price, I think this may be a good time to add shares, capture a dividend and an option premium. I may even consider going out a bit further in time, perhaps to the November 2014 option that will take in the next earnings report and an additional dividend payment, while seeking to use a strike price that might also provide some capital gains on shares, such as the $45 strike.

DuPont (NYSE:DD) isn’t offering a dividend this week, although it will do so later in the August 2015 option cycle. However, before getting to that point, earnings are scheduled to be announced on July 28th.

Following what many shareholders may derisively refer to as the “successful” effort to defeat Nelson Peltz’s bid for a board seat, shares have plummeted. The lesson is that sometimes victories can be pyrrhic in nature.

Since that shareholder vote, which was quite close by most proxy fight standards, shares have fallen about 15%, after correcting for a spin-off, as compared to a virtually unchanged S&P 500.

However, if not a shareholder at the time, the current price may just be too great to pass up, particularly as Peltz has recently indicated that he has no intention of selling his position. While DuPont does offer weekly and expanded weekly option contracts, I may consider the sale of the August monthly contract in an attempt to capture the dividend and perhaps some capital gains on the shares, in addition to the premium that will be a little enhanced by the risk associated with earnings.

The remainder of this week’s limited selection is a bit more speculative and hopefully offers quick opportunities to capitalize by seeing assignment of weekly call options or expiration of weekly puts sold and the ability to recycle that cash into new positions for the following week.

eBay (NASDAQ:EBAY), of course, will be in everyone’s sights as it begins trading without PayPal (Pending:PYPL) as an integral part. Much has been made of the fact that the market capitalization of the now independent PayPal will be greater than that of eBay and that the former is where the growth potential will exist.

The argument of following growth in the event of a spin-off is the commonly made one, but isn’t necessarily one that is ordained to be the correct path.

I’ve been looking forward to owning shares of eBay, as it was a very regular holding when it was an absolutely mediocre performer that happened to offer very good option premiums while it tended to trade in a narrow and predictable range.

What I won’t do is to rush in and purchase shares in the newly trimmed down company as there may be some selling pressure from those who added shares just to get the PayPal spin-off. For them, Monday and Tuesday may be the time to extricate themselves from eBay, the parent, as they either embrace PayPal the one time child, if they haven’t already sold their “when issued” shares.

However, on any weakness, I would be happy to see the prospects of an eBay again trading as a mediocre performer if it can continue to have an attractive premium. Historically, that premium had been attractive even long before murmurings or demands for a PayPal spin-off became part of the daily discussion.

Following a downgrade of Best Buy (NYSE:BBY), which is no stranger to falling in and out of favor with analysts, the opportunity looks timely to consider either the sale of slightly in the money puts or the purchase of shares and sale of slightly out of the money calls.

The $2 decline on Friday allowed Best Buy shares to test a support level and is now trading near a 9 month low. With earnings still a month away, shares offer reasonable premiums for the interim risk and sufficient liquidity of options if rollovers may be required, particularly in the event of put sales.

The arguments for and against Best Buy’s business model have waxed and waned over the past 2 years and will likely continue for a while longer. As it does so, it offers attractive premiums as the 2 sides of the argument take turns in being correct.

Seagate Technology (NASDAQ:STX) will report earnings on July 31st. In the meantime, that gives some opportunity to consider the sale of out of the money puts.

While I generally prefer not to be in a position to take assignment in the event of an adverse price reaction and would attempt to rollover the puts, in this case with an upcoming ex-dividend date likely to be the week after earnings are released, I might consider taking the assignment if faced with that possibility and then subsequently selling calls, perhaps for the week after the ex-dividend date in an effort to capture that dividend and also attempt to wait out any price recovery.

Like Best Buy, Seagate Technology has been in and out of favor as its legitimacy as a continuing viable company is periodically questioned. Analysts pretend to understand where technology and consumer preferences are headed, but as is the case with most who are in the “futurist” business, hindsight often offers a very punishing report card.

Finally, GoPro (NASDAQ:GPRO) reports earnings this week. During its brief time as a publicly traded company it has seen plenty of ups and downs and some controversy regarding its lock-up provisions for insiders.

It is also a company whose main product may be peaking in sales and it has long made a case for seeking to re-invent itself as a media company, in an effort to diversify itself from dependence on consumer cycles or from its product going the commodity route.

The option market is implying a 9.9% movement in shares next week as earnings are reported. However, a 1% ROI may possibly be achieved if selling a weekly put at a strike that is 13.3% below this past Friday’s closing price.

As usual, the week’s potential stock selections are classified as being in the Traditional, Double-Dip Dividend, Momentum or “PEE” categories.

Traditional Stocks: DuPont, eBay

Momentum Stocks: Best Buy, Seagate Technology

Double-Dip Dividend: Fastenal (7/29)

Premiums Enhanced by Earnings: GoPro (7/21 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story.

The one thing that’s been pretty clear as this earnings season is winding down is that the market hasn’t been very tolerant unless the bad news was somehow wrapped in a currency exchange story. Many years ago people were fascinated by the movie “The Three Faces of Eve.”

Many years ago people were fascinated by the movie “The Three Faces of Eve.”

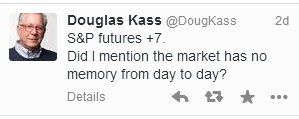

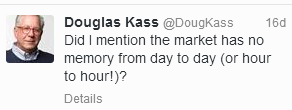

The problem is that which just don’t know which market will be showing up from day to day and sometimes from hour to hour.

The problem is that which just don’t know which market will be showing up from day to day and sometimes from hour to hour. The past week has to be one to make most people pause and try to understand the basis for what we just experienced.

The past week has to be one to make most people pause and try to understand the basis for what we just experienced.