This is the time of year that one can start having regrets about the way in which votes were cast in prior elections.

This is the time of year that one can start having regrets about the way in which votes were cast in prior elections.

Season’s Misgivings

The sad likelihood, however, is that officials elected through the good graces of incredibly gerrymandered districts are not likely to ever believe that their homogeneous and single minded neighbors represent thoughts other than what the entire nation shares.

That’s where both parties can at least agree that is the truth about the other side.

Living in the Washington, DC area the impact of a federal government shutdown is perhaps much more immediately tangible than in a “geometric shape not observed in nature” congressional district elsewhere. However, there is no doubt that a shutdown has adverse effect on GDP and that impact is cumulative and wider spreading as the shutdown continues.

It’s unfortunate that elected officials seem to neither notice nor care about direct and indirect impact on individuals and financial institutions. In war that sort of thing is sanitized by referring to it as “collateral damage.” As long as it’s kept out of sight and in someone else’s congressional district it doesn’t really exist.

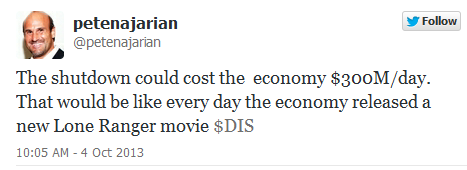

Pete Najarian put it in terms readily understandable, much more so than when some tried expressing the cost of a shutdown in terms of drag on quarterly GDP.

Pete Najarian put it in terms readily understandable, much more so than when some tried expressing the cost of a shutdown in terms of drag on quarterly GDP.

Of course, the real challenge awaits as we once again are faced with the prospect of having insufficient cash to pay debts and obligations. But for what it’s worth at least the rest of the world gets a much needed laugh and boost in national ego, while McGraw Hill Financial (MHFI) and others ponder the price of their calling it as they see it.

At the moment, that’s probably not what the economy needs, but in the perverse world we live in that may mean continued Federal Reserve intervention in Quantitative Easing. While “handouts” are decried by many who don’t see a detriment to a government shutdown, the Federal Reserve handout is one that they are inclined to accept, as long as it helps to fuel the markets.

However, as we are ready to enter into another earnings season this week many are mindful of the fairly lackluster previous earnings season that just ended. While the markets have recently been riding a wave of unexpected good news, such as no US intervention in Syria, continued Quantitative Easing and the disappearance of Lawrence Summers from the landscape, we are ripe for disappointment. We were spared any potential disappointment on Friday morning as the release of the monthly Employment Situation Report fell victim to someone being furloughed.

So what would be more appropriate than to re-introduce the concept of stock fundamentals, such as earnings, into the equation? During this past summer, when our elected officials were on vacation, that’s pretty much where we focused our attention as the world and the nation were largely quiet places. While no one is particularly effusive about what the current stream of reports will offer, a market that truly discounts the future already has its eyes set on the following earnings season that may begin to bear the brunt of any trickle down from a prolonged government shutdown.

At the moment, sitting on cash reserves, I am willing to recycle funds from shares that have been assigned this Friday (October 4, 2013), but am not willing to dip further into the pile until seeing some evidence of a bottoming to the current process that had the S&P 500 drop 2.7% since September 19, 2013 until Friday’s nice showing pared the loss down to 2%. But I need more evidence than a tepid one day respite, just as it will take more than a resolution to the current congressional impasse to believe that we wouldn’t be better served by an unelected algorithm.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

I’m certain many people miss the days when a purchase of shares in Apple (AAPL) was a sure thing. While I like profits as much as the next person, I also enjoy the hunt and from that perspective I think that Apple shares are far more interesting now as we just passed the one year anniversary of having reached its peak price and tax related selling capitalizing on the loss will likely slow. Suddenly it’s becoming like many other stocks and financial engineering is beginning to play a role in attempts to enhance shareholder value.

Without passing judgment on the merits of the role of activist investors it doesn’t hurt to have additional factors that can support share price, particularly at times that the market itself may be facing weakness. Apple has increasingly been providing opportunities for short term gains as its price undulates with the tide that now includes more than just sales statistics and product releases. Capital gains or shares, an attractive dividend and generous option premiums make its ownership easier to consider at current prices. However, with earnings scheduled to be reported on October 22, 2013 I would likely focus on the sale of weekly option contracts as Apple is prone to large earnings related moves.

While Apple has done a reasonable job in price recovery over the past few months amid questions regarding whether its products were still as fashionable as they had been, Abercrombie and Fitch (ANF) hasn’t yet made that recovery from its most recent earnings report that saw a more than 20% price drop. As far as I know, and I don’t get out very much, talks of it no longer being the “cool” place to buy clothes aren’t the first item on people’s conversational agenda. The risk associated with ownership is always present but is subdued when earnings reports are still off in the distance, as they are currently. In the meantime, Abercrombie and Fitch always offers option premiums that help to reduce the stress associated with share ownership.

Ironically, the health care sector hasn’t be treating me terribly well of late, perhaps being whipsawed by the fighting on Capitol Hill over the Affordable Care Act and proposed taxes on medical devices. Additionally, a government shutdown conceivably slows the process whereby regulated products can be brought to the market. Abbott Labs (ABT), whose shares were recently assigned at $35 has subsequently dropped about 5% and will be going ex-dividend this week. Although the dividend isn’t quite as rich as some of the other major pharmaceutical companies after having completed a spin-off earlier in the year, I think the selling is done and overdone.

For me, a purchase of MetLife (MET) is nothing more than replacing shares that were just assigned after Friday’s opportune price surge and that have otherwise been a reliable creator of income streams from dividends and option premiums. At the current price levels MetLife has been an ideal covered call stock having come down in price in response to fears that in a reduced interest rate environment its own earnings will be reduced.

International Paper (IP) is an example of a covered call strategy gone wrong, as the last time I owned it was about a year ago having had shares assigned just prior to its decision to go on a sustained rise higher. While frequently cited by detractors as an argument against a covered option strategy, the reality is that such events don’t happen terribly often, nor does the investor have to eschew greed as share price is escalating or exercise perfect timing. to secure profits before they evaporate. I’ve waited quite a while for its share price to drop, but it is still far from where I last owned them. Still, the current price drop helps to restore the appeal.

Being levered to China or even being perceived as levered to the Chinese economy can either be an asset or a liability, depending on what questionable data is making the rounds at any given moment. Joy Global (JOY) is one of those companies that is heavily levered to China, but even when the macroeconomic news seems to be adverse the shares are still able to maintain itself within a comfortably defined trading range. With Friday’s strong close my shares were assigned, but I would like to re-establish a position, particularly at a price point below $52.50. If it stays true to form it will find that level sooner rather than later making it once again an appealing purchase target and source of option related income.

With the start of a new earnings season one stock that I’ve been longing to own again starts out the season. YUM Brands (YUM) is an always interesting stock to own due to how responsive it is to any news or rumors coming from China. Over the past year it’s been incredibly resilient to a wide range of reports that you would think were being released in an effort to conspire against share price. Food safety issues, poor drink selection during heat waves and Chinese economic slow down have all failed to keep the share price down. While the current price is near the top of its range I think that expectations have been set on the low side. In addition to reporting earnings this week shares also go ex-dividend the following day.

A little less exciting, certainly as compared to Abercrombie and Fitch is The Gap (GPS). In a universe of retailers going through violent price swings, The Gap has been an oasis of calm. It goes ex-dividend this week and if it can maintain that tight trading channel it would be an ideal purchase as part of a covered call strategy.

While The Gap isn’t terribly exciting, Molson Coors (TAP) and Williams Co. (WMB) are even less so. While I usually start thinking about either of them in the period preceding a dividend payment they have each found a price level that has offered some stability, thereby providing some additional appeal in the process that includes sale of near the money calls.

Finally, I have a little bit of a love-hate relationship with Mosaic (MOS). The hate part is only recent as shares that I’ve owned since May 2013 have fallen victim to the collapse of the potash cartel. In a “what have you done for me lately” kind of mentality that kind of performance makes me forget how profitable Mosaic had been as a covered call holding for about 5 years. However, the recent “love” part of the equation has come from the serial purchase of shares at these depressed levels and collecting premiums in alternation with their assignment. I have been following shares higher with such purchases as there is now some reason to believe that the cartel may not be left for dead.

Traditional Stocks: International Paper, Molson Coors, Williams Co.

Momentum Stocks: Apple, Joy Global, MetLife, Mosaic

Double Dip Dividend: Abbott Labs (ex-div 10/10), The Gap (ex-div 10/11), YUM Brands (ex-div 10/9)

Premiums Enhanced by Earnings: YUM Brands (10/8 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

I’ve had a number of people ask about the concept behind “Double Dip Dividends”

I’ve had a number of people ask about the concept behind “Double Dip Dividends”