No matter how old you are, people love getting gifts.

No matter how old you are, people love getting gifts.

That may even be the case when you end up paying for them yourself.

Sometimes, that’s the real surprise.

Last year, for example, I received a surprise birthday gift when hitting one of those round numbers. It was a trip to my favorite city, New Orleans, and I was further surprised by friends and family that had assembled there and then individually popped up at totally unexpected times and places.

The real surprise was when I received the hotel bill and then subsequently the other bills. While I’ll be forever remembering the moment a tap on my shoulder at a busy restaurant announced, “Sir, your drinks are here,” only to turn around and see one of my sons unexpectedly turn up holding a platter of shots. Priceless, but as long as we’re talking about price, I think that I would have chosen less costly libations had I known what was to be in store for me.

In hindsight, though, it was a great gift, but I paid the price as many expect will be the case after years of the Federal Reserve injecting liquidity into the system and keeping interest rates at historic lows, much as is now occurring throughout Europe and the world.

Following the FOMC Statement release this past week was Janet Yellen’s press conference and as one person said to me, hers was the “best tightrope walking” he’d ever seen.

Janet Yellenda, has a nice ring to it and she certainly did a great job of staying on course while questions came at her trying their best to throw her off message. Many of those questions were posed to see her lose her tight cling to the carefully nuanced words that served to tantalize, while hinting of what was ahead.

Instead of seeing the gift for what it was, they wanted to know when the bill would be coming due and maybe who was going to end up holding the bag when the celebrations were all over.

Of course, there are those really sick people for whom the gift would be seeing someone else fail or fall off that tightrope wire, but Yellen was better than any gust of wind that could come her way.

For those that had so recently come to expect that perhaps the FOMC would raise interest rates with this past week’s statement release, the market made it clear that they considered the delay as a real gift, even if the celebration and enjoyment lasted just for a day or so.

Sooner or later, there’s also a price that needs to be paid.

That gift, withholding the interest rate increase that just a couple of weeks ago seemed as if it might come this past week, not only was being delayed, but perhaps being delayed all the way to September. As if that gift wasn’t enough, there was a suggestion that any rate increase wasn’t necessarily going to be part of a planned series of regular rate increases, as had been the practice during the Greenspan era.

Could it get any better? At least that was how most heard her words as she delicately balanced them against one another, saying only those things that could be construed by willing ears as “Laissez les bons temps rouler,” as they like to say in New Orleans.

On Thursday, the day after the FOMC Statement release and press conference, it didn’t seem that it could get any better, as the market celebrated what could only be interpreted as a gift for stock investors.

Still, the reality is that while we are winding down a monetary policy era that has likely been to the benefit of our stock markets, the rest of the world is now beginning on that path and may offer stiff winds for us as the bill gets tallied.

The gales coming from Europe were evident this past week as the market was also reacting to the tightrope walk that Greece was doing as it vacillated between being reasonable and unrealistic.

Telling its IMF and ECB safety nets that there were better safety nets out there, while forgetting that neither Russia nor China has ever saved anyone without exacting a price that makes simple interest paid to the IMF and ECB look absolutely charitable, our own markets swayed along with those cross currents of uncertainty.

There may be lots of those cross currents ahead, so that balancing skill may come in very handy while waiting for earnings season to begin again in July and offering the possibility of getting grounded in fundamental reality.

As usual, the week’s potential stock selections are classified as being in Traditional, Double-Dip Dividend, Momentum or “PEE” categories.

Last week marked the second consecutive week in which I didn’t open any new positions, something that would have been unimaginable to me at any point during the past 7 or more years. This coming week I can see more of the same, as there’s very little compelling news ahead to make we want to let go of the cash in my hand. As the bill may be ready to come due soon, I’d like to be ready with that cash on hand to balance the cha

llenge of uncertainty.

Of course, as is usually the case, once the reality of the bill finally settles in, most of the time that represents an opportunity to again start moving forward.

For now, unless there is some further compelling reason to come from upcoming GDP, Retail Sales, Employment Situation and JOLTS reports to believe that the economy is heating up sufficiently to warrant a rate increase in July, the next catalyst may very well come from earnings.

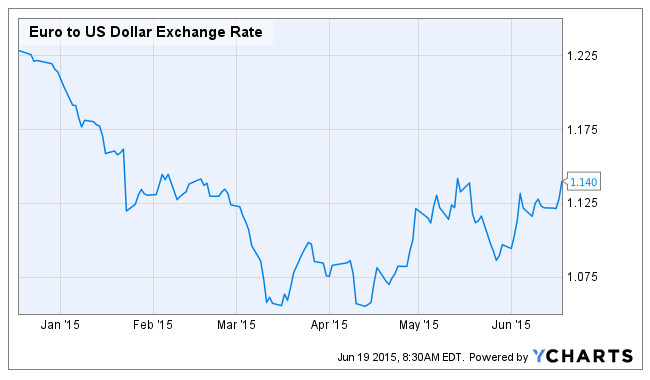

This past week Oracle (NYSE:ORCL) reported earnings. It is among a very small handful of significant companies that report late in the cycle. In fact, their report was almost 3 months following the close of the quarter upon which they reported. While many of those reported soon after earnings season started, less than 2 weeks after the close of that quarter, the expectation for currency related revenue declines was so high at that time, that those companies didn’t see stock prices harshly punished for the dollar’s strength.

Now? Not so much.

Most, in fact, took the previous earnings report opportunity to provide decreased forward guidance as the expectation was that we were headed for US Dollar and Euro parity.

Nearly 3 months later that projection hasn’t become reality, as the US dollar has weakened significantly since March 31, 2015 and that can be expected to show up in the next quarter’s earnings reports. Unfortunately for Oracle share holders, had the company reported in April, there’s a chance that they would have gotten the same free pass as did others at that time.

Sinclair Broadcasting (NASDAQ:SBGI) and Comcast (NASDAQ:CMCSA) are both firmly in the control of their founding families and are on different ends of the spectrum when it comes to their approach to bringing content into the home.

The family nature of Comcast was highlighted this past Friday with the passing of its founder, Ralph Roberts, at age 95. My mother used to say, “they should never go younger,” and while I was never a fan of their product and service, the man was an outlier in many good ways.

With Comcast having recently been extricated from a potential buyout of another cable company, it’s also finding that there are opportunities outside of people’s television sets and streaming devices, as its ownership of Universal Studios makes it the beneficiary of some blockbuster movie releases.

On the downside, it is near its 52 week high as it gets ready to go ex-dividend the week after next. That gives some reason for pause, although neither Greece nor currency headwinds should be an issue, although rising interest rates can be particularly hurtful for a capital intensive company.

However, I especially like Monday ex-dividend dates and like the idea of being assigned early on those positions, as you can get an additional week of premium in exchange for giving up the dividend and holding the stock position for a shorter period of time than planned, while having the opportunity to re-invest the assignment proceeds into another position. With the availability of expanded weekly options on Comcast there are a number of different expiration dates that can be used in an effort to capture additional time premium or try to find the right balance between premium, dividend and time.

Sinclair Broadcasting is in the terrestrial business and just keeps getting larger and larger. It’s not particularly an exciting stock, but does trade with a fairly large price range without any particularly moving news.

It is now at a price that is still above its range mid-point, but that however, has been a reliable launching pad for new positions. With only monthly options available the time commitment is longer as the July 2015 cycle begins this coming week. With earnings coming during the August 2015 cycle any short term price decline necessitating a rollover may look to bypass additional earnings risk and go to a September 2015 expiration, which would also include an upcoming dividend.

Philip Morris (NYSE:PM) and Blackberry (NASDAQ:BBRY) can both elicit some emotional responses, but for very different reasons. Both have upcoming events this week that can offer some opportunity.

Philip Morris is ex-dividend this week and that dividend is very attractive. The company recently stopped its aggressive buyback program as it was feeling the pain of currency exchange and did so, ostensibly, in favor of the dividend. With a history of annual dividend increases coming for the third quarter of each year, there is some question as to wh

ether that will be possible this year, as cash flow is decreased from both currency and declining sales.

Earnings are scheduled to be reported on the day prior to the end of the July 2015 monthly cycle, so in the event that shares haven’t been assigned prior to that, I would consider attempting to rollover any expiring option to a date that may give sufficient time to recover from any price decline.

Blackberry reports earnings this week and is sitting precariously near its yearly lows. The options market is implying an 8% price move when earnings are released on Tuesday morning.

Blackberry usually has released earnings on Friday mornings over the past few years and I’ve generally overlooked it because my preference is to sell a weekly put on most earnings related trades. I further prefer those that report early in the week, so as to have time for some price recovery if at risk for assignment, particularly as some price recovery could ease the ability to rollover the position to delay or avoid assignment.

With a Tuesday morning report and the chance of achieving a 1% ROI at a strike just outside the range implied by the options market, the interest in a short put position is rekindled. However, the greatest likelihood is that I would be more inclined to consider a put sale after earnings, if the price declines, as the premium can really get further enhanced as the price challenges that 52 week low.

I currently own shares of Dow Chemical (NYSE:DOW) and am at risk of having those shares assigned in order to capture the dividend. With those contracts expiring on July 2, 2015 and the ex-dividend date of Friday, June 26th, the $0.42 dividend would require a price of at least $53.92 for the $53.50 options to be assigned early. If that looks like a possibility as trading nears it close on Thursday, I may consider rolling over the option position in order to secure the dividend.

However, with any price decline in shares, particularly if coming early in the week, I would consider adding additional shares and again consider selling call options for the following, holiday shortened week, or even for the week afterward.

Dow Chemical has recently been trading well off its lows that were fueled by decreasing oil prices. CEO Andrew Liveris, who has come under fire on his own for allegedly using his position to finance his lifestyle, did an excellent job in convincing investors that Dow Chemical was a beneficiary of decreasing oil prices, rather than a victim, as it was being treated early in 2015, prior to his going on the offensive.

I think that even if oil prices head moderately higher in the near term, Andrew Liveris would be able to convince people that was also to the benefit of Dow Chemical, just as I expect he’ll be able to convince internal Dow Chemical “watch dogs” that his personal actions were entirely appropriate.

Finally, I had Bank of America (NYSE:BAC) shares assigned this past week, but following weakness among financials on Friday, as well as following the week’s peak in interest rates, shares declined.

That decline, although still leaving shares near a 6 month high, does provide another entry point opportunity. While its shares may continue to be pressured if the bond market bids interest rates lower, the bond market knows exactly where interest rates are going to be headed and financials should be following along.

While the premiums aren’t spectacular, I would look at a potential purchase of shares with an eye toward a longer term holding trying to capitalize on share gains supplemented by option premiums while awaiting the reality of rate increases to come.

Traditional Stocks: Sinclair Broadcasting

Momentum Stocks: Bank of America

Double-Dip Dividend: Comcast (6/29), Dow Chemical (6/26), Philip Morris (6/23)

Premiums Enhanced by Earnings: Blackberry (6/23 AM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.