What gives me cause for concern that I might be wrong, at least in the near term, is the increasingly vocal sentiment that we are ready for a significant market decline. It doesn’t take much of a contrarian to realize that when it seems that everyone is on board it is the time to get off.

Maybe that’s what explains Thursday’s really irrational market joy ride coming off the heels of a 5% decline in the Nikkei and an early 100 point loss in the pre-opening US futures markets. All of the naysayers came out at once ready to take credit for their impeccable timing in calling the correction.

But a bit more confusing is When omni-present personalities express sentiments that are either to the extreme or counter to their historical sentiment. Especially when bulls become bears and bears become bulls. When that begins to happen it may be time to literally and figuratively “take stock.”

When perma-bear Nouriel Roubini expresses a bullish tone or when Dennis Gartman proclaims that he is “worried” there are direct messages conveyed that can elicit direct responses, but just as easily elicit contrary responses.

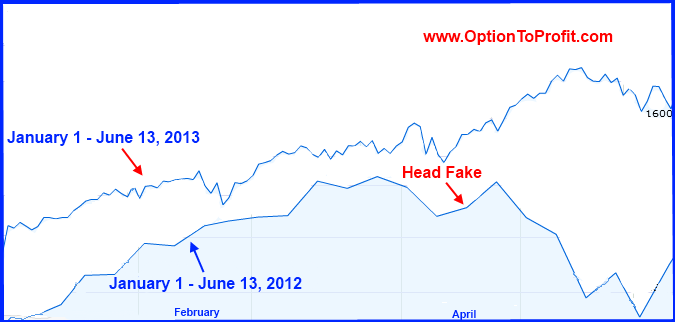

I have been convinced that the melt-up higher in 2013 was going to be a repeat of that seen in 2012 in scope, time and velocity.

But over the past month the coincident time frame has slipped away, as this time last year we were already on the way to a recovery from an abrupt 9% drop after 4 months or higher markets.

While the time frame has been shifted, as the 2013 rally has thus far exceeded that of 2012, my belief that the rallies from the market’s recent drop is simply the same kind of “head fake” that was seen in April 2012, when the market recovered from a 2 week loss. The recovery also recovered everyone’s confidence that the market could now only continue on its upward path.

While the time frame has been shifted, as the 2013 rally has thus far exceeded that of 2012, my belief that the rallies from the market’s recent drop is simply the same kind of “head fake” that was seen in April 2012, when the market recovered from a 2 week loss. The recovery also recovered everyone’s confidence that the market could now only continue on its upward path.

In that case, the proverbial “testing of the highs” resulted in a failing grade.

Back then, the reality was different and sudden. When balloons pop, it’s sudden. The first few months of 2012 was a balloon.

Certainly the sudden spate of triple digit days and ever widening intra-day trading ranges is sending some kind of message. In 2012 triple digit gains were rare, but started increasing right before the plunge. Now, not only are triple digit days a recent common occurrence, but the intra-day trading range, from daily low to high, has nearly doubled, since the market topped on May 21, 2013.

To add some fuel to the mix, this coming week features a Quadruple Witching, which granted is not the big deal that it was a decade or two ago, but also features release of FOMC minutes and a press conference by Federal Reserve Chairman Ben Bernanke.

The constellation of events may have the markets reaching a threshold at which point it may not be able to contain its behavior. Certainly closing the week with another triple digit loss, unable to follow through on Thursday’s nearly 200 point gain doesn’t inspire confidence.

But do balloons under mounting pressure only pop, or is there another path?

I’ve been busily amassing cash in anticipation of a pop and have missed out on a portion of the rally. Instead of making approximately 10 new trades each week, for the past two months there have typically been only five new trades. Additionally, instead of looking for weekly option opportunities, increasingly the search has been for the safety seen in monthly option writing. I simply didn’t want to be shocked by the pop.

But after waiting so long each day begs the question. Is it time to change? What if the decline either doesn’t come or instead is an insidious leaking of value as a result of increased volatility with an overall net decline characterized by alternating large moves in both directions? While the climb higher was slow and steady, could the descent downward be slow and erratic?

Unlike the frog in a slowly heated kettle who never realizes he’s about to be boiled, a slowly depreciating market may still be compatible with continued investing vitality. That kind of market may be best approached by employing more cash from the sidelines and greater use of short term hedging vehicles.

Which is it going to be? As with most things I try not to make abrupt changes, but rather attempt to transition, as long as events allow a methodical approach. The significance of preparing for the possibility of a slow leak is that I may give some more consideration to Momentum stocks and shorter option contract durations, but still looking for positions that have under-performed the S&P 500 since the market top.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details).

The first stock of the week is emblematic of the excesses of an earlier period and reminiscent of a market top in the making. That was a balloon popping, in case you needed an example. Those remembering the frenzy associated with the Blackstone Group IPO (BX) will remember that there were disappointing IPOs long before Facebook (FB) came on the trading scene. Its shares are still far away from its IPO price, in fact, further away than is Facebook and they have had much more time to recover. Granted, along the way there’s been dividends to accrue, but all in all, a disappointing few years. Most recently, its public profile has been raised,as its been increasingly involved in prospective buyouts and has developed a stable of well run companies. The caveat to this position is that earnings are reported just prior to the July 2013 option cycle expiration

Abercrombie and Fitch (ANF) is just one of those companies that people like to hate. Whether it’s the image it portrays or whether it’s the public face of its CEO, it’s just difficult to get a warm and fuzzy feeling about the culture. But when it comes to a reliable and consistent vehicle for generating option premium income, it is always high on my list. Always volatile, especially in the weeks before earnings, when it pre-announces European sales and its currency woes, it can be rewarding as a short term tool, but you have to be prepared for unexpected rides and longer term commitments.

Oracle (ORCL) reports earnings this week. For those that remember the last earnings report, its CEO, Larry Ellison pointedly blamed his sales staff on the very disappointing numbers. There may have been something to that, uncomfortable as it was to hear the vitriol directed toward his employees, as competitors fared very well during the quarter and have continued doing so. It seems very unlikely to me that Ellison would put himself in a position to trail the pack again and for Oracle to be thought of as an industry laggard. Whereas I prefer to consider the sale of puts for most earnings related plays, in this case I’m more likely to consider the purchase of shares and the sale of calls.

Las Vegas Sands (LVS) has certainly had a nice run lately and I’ve been wanting to buy shares back since March, but it hasn’t even given the slightest indication that it was ready to return to the low $50s level. Down nearly 6% from its recent high and going ex-dividend this week may be a good enough combination to entice me this week to purchase shares, but my preference would be for a very short holding period because of over-riding market concerns.

Coach (COH), too, is higher than I would like, but I do want to repurchase shares. I’ve been a serial buyer for the past year and have and now that it offers weekly options it has additional appeal, even at share prices that are at the high end of my comfort level.

Transocean (RIG) was a stock that I had also considered purchasing last week. WIth it’s price decline in the absence of any substantive company or sector specific news, it now looks even more appealing. In the 2013 market, much of the time a stock in the crosshairs that was subsequently not purchased has gone on to create some regret as prices have generally gone higher. There haven’t been as many opportunities for a second chance as in markets that typically alternate moves higher and lower.

Barclays (BCS), like many in the financial sector, had gone up just too much and too fast. It’s now down about 7% since both its peak and the market peak. Although it still may have another few percent on the downside before it hits some support, I don’t believe that there will be any near term events to put it uniquely at risk. As with many positions that offer only monthly options, I am more inclined to consider adding them during the final week of a monthly cycle.

With or without the purchase of Oracle, I’m already over-invested in the technology sector, so I would look cautiously at adding additional technology positions. However, Texas Instruments (TXN) started lagging the market a few weeks before the current lull and has also under-performed since the market top, making it a candidate for consideration. Following its most recent drop in response to guidance last week, I believe it offers some value in return for the risk of about a 4% downside in the event of some market tumult.

Caterpillar (CAT), despite having had a strong week this past week, appears to be a relatively low risk position at these levels, having very successfully defended the $80 level for the past year. Its ability to consistently bounce back and maintain its price levels despite any positive news in quite some time attests to its strength and makes it an ideal covered option position over the longer term. With its announcement of an increased dividend, payable during the July 2013 option cycle, it adds to its appeal. Although increasing a dividend is usually greeted in a positive manner, there were choruses of those finding fault, claiming that it reflects the inability to invest in the growth of the business. My guess is that very few investors will be frightened away by a competitive dividend.

Although Caterpillar reports its earnings during the first week of the August 2013 cycle, which should not effect its price action significantly during the July 2013 cycle, my one concern is that Cummins Engine (CMI) reports earnings on July 30, 2013. Although that, too, is during the August cycle, Cummins frequently provides guidance two to three weeks before its earnings are released. If recent past history is any guide, disappointing guidance from Cummins adversely impacts a number of other stocks, which do have a tendency, however to recover relatively quickly.

Finally, I identified Safeway (SWY) as a possible Double Dip Dividend selection earlier in the week and then expected to toss it into the wastebasket after it announced the sale of its Canadian assets and its shares went up by nearly 40% in the after-hours. Somehow, despite a market that traded up nearly 1.5%, Safeway gave up the vast majority of its gains, still finishing the day at a very respectable 7%. Even after a jump higher, Safeway shares are still about 12% lower than its April 2013 peak.

Traditional Stocks: Barclays, Caterpillar, Texas Instruments, Transocean

Momentum Stocks: Abercrombie and Fitch, Blackstone Group, Coach

Double Dip Dividend: Safeway (ex-div 6/18), Las Vegas Sands (ex-div 6/18)

Premiums Enhanced by Earnings: Oracle (6/20 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

In the weeks since Pfizer’s (PFE) announcement that it was offering the remainder of its 400+ million holding in Zoetis (ZTS) in exchange for Pfizer shares many opinions have been offered regarding the relative merits of the tender offer.

In the weeks since Pfizer’s (PFE) announcement that it was offering the remainder of its 400+ million holding in Zoetis (ZTS) in exchange for Pfizer shares many opinions have been offered regarding the relative merits of the tender offer.

{kind=link}

{kind=link}