new year starts off with great promise.

new year starts off with great promise.

If seems so strange that the stock market often takes on a completely different persona from one day to the next.

Often the same holds true for one year to the next. despite there being nothing magical nor mystical about the first trading day of the year to distinguish it from the last trading day of the previous year.

For those that couldn’t wait to be finally done with 2015 out of the expectation conventional wisdom would hold and that the year following a flat performing year would be a well performing year, welcome to an unhappy New Year.

2015 was certainly a year in which there wasn’t much in the way of short term memory and the year was characterized by lots of ups and downs that took us absolutely nowhere as the market ended unchanged for the year.

While finishing unchanged should probably result in neither elation nor disgust, scratching beneath the surface and eliminating the stellar performance of a small handful of stocks could lead to a feeling of disgust.

Or you could simply look at your end of the portfolio year bottom line. Unless you put it all into the NASDAQ 100 (NDX) or the ProShares QQQ (NASDAQ:QQQ), which had no choice but to have positions in those big gainers, it wasn’t a very good year.

You don’t have to scratch very deeply beneath the surface to already have a sense of disgust about the way 2016 has gotten off to its start.

There are no shortage of people pointing out that this first week of 2016 was the worst start ever to a new year.

Ever.

That’s much more meaningful than saying that this is the worst start since 2019.

A nearly 7% decline in the first week of trading doesn’t necessarily mean that 2016 won’t be a good one for investors, but it is a big hole from which to have to emerge.

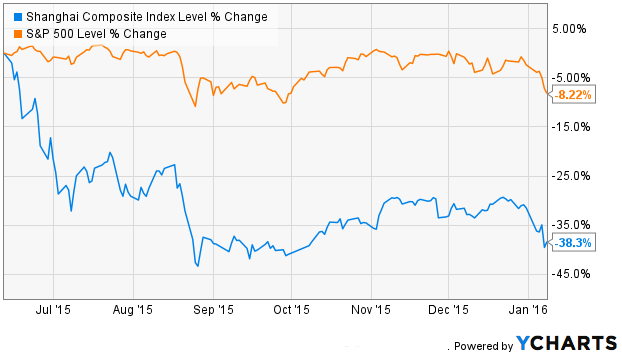

Of course a 7% decline for the week would look wonderful when compared to the situation in Shanghai, when a 7% loss was incurred to 2 different days during the week, as trading curbs were placed, markets closed and then trading curbs eliminated.

If you venture back to the June through August 2015 period, you might recall that our own correction during the latter portion of that period was preceded by two meltdowns in Shanghai that ultimately saw the Chinese government enact a number of policies to abridge the very essence of free markets. Of course, the implicit threat of the death penalty for those who may have knowingly contributed to that meltdown may have set the path for a relative period of calm until this past week when some of those policies and trading restrictions were lifted.

At the time China first attempted to control its markets, I believed that it would take a very short time for the debacle to resume, but these days, the 5 months since then are the equivalent of an eternity.

While China is again facing a crisis, the United States is back to the uncomfortable position of being the dog that is getting wagged by the tail.

US markets actually resisted the June 2015 initial plunge in China, but by the time the second of those plunges occurred in August, there was no further resistance.

For the most part the two markets have been in lock step since then.

Interestingly, when the US market had its August 2015 correction, falling from the S&P 500 2102 level, it had been flat on the year up to that point. Technicians will probably point to the fact that the market then rallied all the way back to 2102 by December 1, 2015 and that it has been nothing but a series of lower highs and lower lows since then, culminating in this week.

The decline from the recent S&P 500 peak at 2102 to 1922 downhill since then is its own 8.5%, putting us easily within a day’s worth of bad performance of another correction.

Having gone years without a traditional 10% correction, we’re now on the doorstep of the second such correction in 5 months.

While it would be easy to thank China for helping our slide, this past week was another of those perfect storms of international bad news ranging from Saudi-Iran conflict, North Korea’s nuclear ambitions and the further declining price of oil, even in the face of Saudi-Iran conflict.

Personally, I think the real kiss of death was news that 2015 saw near term record inflows into mutual funds and that the past 2 months were especially strong.

I’ve never been particularly good at timing, but there may be reason to believe that at the very least those putting their money into mutual funds aren’t very good at it either.

If I still had a shred of optimism left, I might say that the flow into mutual funds might reflect more and more people back in the workforce and contributing to workplace 401k plans.

If that’s true, I’m sure those participants would agree with me that it’s not a very happy start to the year. For those attributing end of the year weakness to the “January Effect” and anticipating some buying at bargain prices to drive stocks higher, that theory may have had yet another nail placed in its coffin.

As usual, the week’s potential stock selections are classified as being in the Traditional, Double Dip Dividend, Momentum or “PEE” categories.

2015 turned out to be my least active year for opening new positions since I’ve been keeping close track. Unfortunately, of those 107 new positions, 29 are still open and 15 of those are non-performing, as they await some opportunity to sell meaningful calls against them.

If you would have told me a year ago that I would not have rushed into to pick up bargains in the face of a precipitous 7% decline, I would have thought you to be insane.

While I did add one position last week, the past 2 months or so have been very tentative with regard to my willingness to ease the grip on cash and for the moment there’s not too much reason to suspect that 2016 will be more active than 2015.

With that said, though, volatility is now at a level that makes a little risk taking somewhat less of a risk.

While volatility has now come back to its October 2015 level, it is still far from its very brief peak in August 2015, despite the recent decline being almost at the same level as the decline seen in August.

Of course that 2% difference in those declines, could easily account for another 10 or so points of volatility. Even then, we would be quite a distance from the peak reached in 2011, when the market started a mid-year decline that saw it finish flat for the year.

The strategy frequently followed during periods of high volatility is to considering rolling over positions even if they are otherwise destined for assignment.

The reason for that is because the increasing uncertainty extends into forward weeks and drives those premiums relatively higher than the current week’s expiring premiums. During periods of low volatility, the further out in time you go to sell a contract, the lower the marginal increase in premium, as a reflection of less uncertainty.

For me, that is an ideal time and the short term outlook taken during a period of accelerating share prices is replaced by a longer term outlook and accumulation of greater premium and less active pursuit of new positions.

The old saying “when you’re a hammer, everything looks like a nail,” has some applicability following last weeks broad and sharp declines. If you have free cash, everything looks like a bargain.

While no one can predict that prices will continue to go lower as they do during the days after the Christmas shopping season, I’m in no rush to run out and pay today’s prices because of a fear that inventory at those prices will be depleted.

The one position that I did open last week was Morgan Stanley (NYSE:MS) and for a brief few hours it looked like a good decision as shares moved higher from its Monday lows when I made the purchase, even as the market went lower.

That didn’t last too long, though, as those shares ultimately were even weaker than the S&P 500 for the week.

While I already own 2 lots of Bank of America (NYSE:BAC), the declines in the financial sector seem extraordinarily overdone, even as the decline in the broader market may still have some more downside.

As is typically the case, that uncertainty brings an enhanced premium.

In Bank of America’s case, the premium for selling a near the money weekly option has been in the 1.1% vicinity of late. However, in the coming week, the ROI, including the potential for share appreciation is an unusually high 3.3%, as the $15.50 strike level offers a $0.19 premium, even as shares closed at $15.19.

With earnings coming up the following week, if those shares are not assigned, I would consider rolling those contracts over to January 29, 2016 or later.

At this point, most everyone expects that Blackstone (NYSE:BX) will have to slash its dividend. As a publicly traded company, it started its life as an over-hyped IPO and then a prolonged disappointment to those who rushed into buy shares in the after-market.

However, up until mid-year in 2015, it had been on a 3 year climb higher and has been a consistently good consideration for a buy/write strategy, if you didn’t mind chasing its price higher.

I generally don’t like to do that, so have only owned it on 3 occasions during that time period.

Since having gone public its dividend has been a consistently moving target, reflecting its operating fortunes. With it’s next ex-dividend date as yet unannounced, but expected sometime in early February, it reports earnings on January 28, 2015.

That presents considerable uncertainty and risk if considering a position. I don’t believe, however, that the announcement of a decreased dividend will be an adverse event, as it is both expected and has been part of the company’s history. WHat will likely be more germane is the health of its operating units and the degree of leverage to which Blackstone is exposed.

If willing to accept the risk, the premium reward can be significant, even if attenuating the risk by either selling deep in the money calls or selling equally out of the money put contracts.

I’m already deep under water with Bed Bath and Beyond (NASDAQ:BBBY), but after what had been characterized as disappointing earnings last week, it actually traded fairly well, despite the overall tone of the market.

It is now trading near a multi-year low and befitting that uncertainty it’s option premiums are extraordinarily generous, despite having a low beta,

As is often the case during periods of heightened volatility, consideration can be given to the sale of puts options rather than executing a buy/write.

However, given its declines, I would be inclined to consider the buy/write approach and utilize an out of the money option in the hopes of accumulating share appreciation and dividend.

If selling puts, I would sell an out of the money put and settle for a lower ROI in return for perhaps being able to sleep more soundly at night.

During downturns, I like to place some additional focus on dividends, but there aren’t very many good prospects in the coming week.

One ex-dividend position that does get my attention is AbbVie (NYSE:ABBV).

As it is, I’m under-invested in the healthcare sector and AbbVie is currently trading right at one support level and has some additional support below that, before being in jeopardy of approaching $46.50, a level to which it gapped down and then gapped higher.

It has a $0.57 dividend, which means that it is greater than the units in which its strike levels are defined. While earnings aren’t due to be reported until the end of the month, its premium is more robust than is usually the case and you can even consider selling a deep in the money call in an effort to see the shares assigned early. For what would amount to a 2 day holding, doing so could result in a 1.2% ROI, based upon Friday’s closing prices and a $55 strike level.

Finally, retail was especially dichotomous last week as there were some very strong days even during overall market weakness and then some very weak days, as well.

For those with a strong stomach, Abercrombie and Fitch (NYSE:ANF) is well off from its recent lows, but it did get hit hard on Friday, along with the retail sector and everything else.

As with AbbVie, the risk is that while shares are now resting at a support level, the next level below represents an area where there was a gap higher, so there is really no place to rest on the way down to $20.

The approach that I would consider for an Abercrombie and Fitch position to sell out of the money puts, where even a 6% decline in share price could still provide a return in excess of 1% for the week.

When selling puts, however, I generally like to avoid or delay assignment, if possible, so it is helpful to be able to watch the position in the event that a rollover is necessary if shares do fall 6% or more as the contract is running out.

Traditional Stocks: Bank of America, Bed Bath and Beyond

Momentum Stocks: Abercrombie and Fitch, Blackstone

Double-Dip Dividend: AbbVie (1/13 $0.57)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable – most often coupling a share purchase with call option sales or the sale of covered put contracts – in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week, with reduction of trading risk.