Volatility is back!

Volatility is back!

That’s all you heard this week as the S&P 500 dropped 0.4% to end the unrequited January Rally that we had all been told was the historical norm.

As a covered option seller I have learned to embrace the uncertainty that ushers in a period of volatility, although I make no pretense of really understanding exactly how “volatility works. Like many things in life sometimes it’s simply easier to take one’s word for it.

Just like when you’re told that volatility is back.

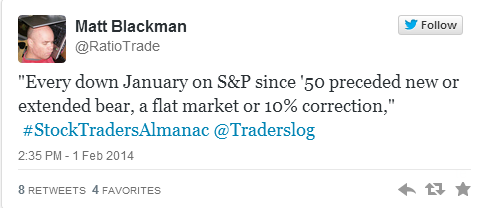

Or when social media suggests a relationship that isn’t borne out in historical fact, such as very notably in 2010 or about 50% of the other times January opened the year with a loss in the past 63 years.

While the expression “greed is good,” may be far more memorable, there’s not much debate for those who follow it that “volatility is good.” Not only does it create enhanced option premiums but it may also be the ultimate portfolio insurance.

For many people hearing that volatility has returned the only reasonable course of action is to head for the exits, because the very mention of the word is associated with wild rides, mostly in the wrong direction. For them volatility is far from good and is something to be feared and avoided.

That picture isn’t entirely accurate. Volatility is simply a measure of uncertainty and size. 2013 was a year of low volatility as there was a high degree of certainty when you arose each morning that the stock market would move higher on any given day. Additionally, it did so in a largely non-dramatic fashion. The movements were small, but consistent and sustained.

Suddenly the movements are now larger and can just as easily go in one direction as in the opposite one. The range has expanded, too. You don’t need a complex formula to have a qualitative sense that something is different. Not necessarily bad, just different.

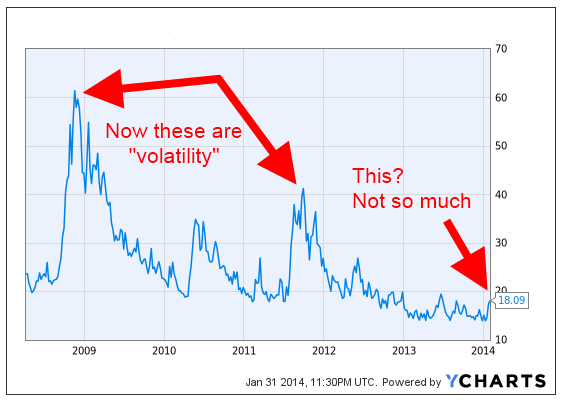

But as long as we were talking about historical norms and how disappointing it was waiting for the historically predicted January Rally that never came, the cries welcoming back volatility may have lost track of what historical levels of volatility have been.

But as long as we were talking about historical norms and how disappointing it was waiting for the historically predicted January Rally that never came, the cries welcoming back volatility may have lost track of what historical levels of volatility have been.

The volatility of this past week hasn’t even reached the levels seen in October 2013 back when the S&P 500 stood at 1655, which represented a loss similar to that currently at hand. The current level of volatility is certainly dwarfed by that seen in 2011, which itself was far smaller than that seen in late 2008.

2011 which was one of my favorite years saw the S&P 500 end the year precisely unchanged. However, during the course of the year there were regular triple digit moves, often in alternating direction and ultimately accomplishing nothing. That was a covered option seller’s greatest fantasy come true.�

Yet the cries of the return of volatility weren’t making the rounds in October and spreading the specter of an imminent collapse of all that has preceded the market’s climb. While so many have spoken of a 5-10% decline being a healthy thing, some began to utter an heretofore unheard 15-20% range correction in the making.

For those that have been counting on an inflow of money that has been said to still reside on the sidelines to continue fueling the market’s rise the past week’s $12 billion in outflows from equity funds represented the highest level in two years. That represents selling that won’t likely be put back at risk very quickly, but it also represents money that won’t contribute to downward pressure on prices any time soon.

While volatility has risen significantly in the past week it has done so from 5 year lows. There is also certainly more upside to volatility than there is downside. It is with an understanding of the mathematical basis for volatility that there comes an appreciation for the manner in which volatility may be quickly magnified far beyond the seeming disruption in the market.

So no. Volatility isn’t back yet, but it can be in an imperceptible instant.

With the uncertainty that awaits low beta stocks may have special value and the sale of options may increasingly become inviting even at out of the money strike levels, something that hasn’t been the case in quite a while. The market may be said to not like uncertainty but it does have its rewards.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

Apple (AAPL) briefly closed below $500 this week. Since not too many stocks occupy that kind of rarefied neighborhood it’s not too surprising that the last couple of times a big fuss was made about a stock falling below $500 it was Apple eliciting the anguish. While there has certainly been lots of debate following Apple’s recent disappointing sales, especially of its iPhone franchise, it does go ex-dividend this week and in its short history of paying a dividend it has generally performed well in its short term aftermath. That alone has me interested in addition to Apple’s low beta and head start on any market inspired drop. Others can debate Apple’s near term future and product cycles and innovations, but the combination of dividend and volatility enhanced premiums makes it look especially good as a choice for this week. The fact that Carl Icahn seems to have made a longer term commitment and has increasingly increased that commitment at least allows for misery to have company if the short term thesis is incorrect.

Another stock that has taken quite a significant fall in the past two weeks has been Starbucks (SBUX) down nearly 10% YTD and even down 4% since its earnings related jump in share price on a day when the market itself tumbled. Perhaps the market is concerned that CEO Howard Schultz may be removing himself more from daily operations, recalling the last time that occurred. However, the root cause of Starbucks’ difficulties earlier last decade, the unbridled expansion during a period of economic contraction, isn’t likely to be repeated. Starbucks is ex-dividend this week and may also be ahead of the curve of any further market declines. It too is showing some enhancement of its option premiums, particularly when dividend capture is also considered.

EMC Corporation (EMC) and its spin off VMWare (VMW) both reported earnings last week. Both declined as a result, with EMC suffering its own disappointment and also bearing some of the VMWare burden, owing to its continuing 80% ownership. While much attention was directed toward Microsoft (MSFT) this week as speculation heated up that an insider, whose own emphasis was on cloud based strategies would be the new CEO, EMC stock continues to languish in relative obscurity and trades in a fairly defined range. A low beta, despite its connection to VMWare,a decent dividend and option premium makes EMC an ever present consideration when seeking to round out the technology sector of my portfolio without wanting to take on undue risk.

On January 8th Transocean (RIG) was cut to “sector perform” from “sector outperform.” A week later it started a decline from the $48 level but without any company specific news, although similar companies, such as Seadrill (SDRL) and ENSCO (ESV) moved in unison. Transocean, after its decline is sitting at an 18 month low which occurred at the time of the temporary suspension of its dividend. With a dividend rate now standing at over 5% and a miniscule payout ratio, combined with its option premium it is one of those few stocks that I would consider owning at this moment without concomitant call sales on shares.

Mondelez (MDLZ) is most everyone’s idea of a lackluster and unexciting company. Because of its perceived mediocrity and uninspired leadership it has gotten the attention of the activist investment community. Unfortunately for pre-existing shareholders the ascension of Nelson Peltz to the Board of Directors was accompanied by the statement that he wouldn’t pursue a deal with PepsiCo (PEP) and subsequently shares significantly under-performed the S&P 500, despite a very low beta. As a result of its recent increased volatility its option premium is beginning to perk up and is getting interesting as it share price is returning to a more manageable level.

Joy Global (JOY) and Las Vegas Sands (LVS) speak to the differing fortunes found in China. While construction and infrastructure projects are slowing, as is the manufacturing index, apparently gaming is alive and well in Macao. After an initial plunge in shares in the after hours as Las Vegas Sands reported its earnings a better understanding of the details behind the report saw a quick reversal.

Las Vegas Sands was frequently owned stock in 2012, but less so in 2013 as I had been waiting for a price retreat that never came. The recent drop from $82 may be the best such drop to be had. While shares do trade at a higher beta than I am interested in pursuing to broadly round out my existing portfolio, indications are that the engines running Las Vegas Sands’ operations aren’t going to slow down in response to Chinese economic woes.

Joy Global on the other hand has engines that literally could be stalled by a faltering Chinese economy. Like many other companies highlighted this week it has greatly underperformed the broad market of late. While doing so shares have returned to near the mid-point of a very comfortable trading range and continues to offer an option premium in line with its volatility.

The coming week is another busy one for earnings. A more detailed look at this week’s earnings related trade considerations is available in an accompanying article. This week more candidates stand out as opportunities by virtue of meeting my ROI and risk criteria in addition to Twitter (TWTR) and Green Mountain Coffee Roasters (GMCR) identified in this article.

Green Mountain Coffee Roasters somehow continues to confound everyone by remaining relevant. While shrouded in controversy it has to be hailed as one of the great share comebacks in recent years, although it is throwing so many concepts into the air these days one has to wonder whether focus is getting dissipated as its core product lines increasingly become commodities and held hostage by agreements with other companies, such as Starbucks.

However, for an earnings related trade those issues may share a lack of relevancy with the company’s future prospects. Always volatile around earnings, with 20% price moves not unusual, the options market is implying an 11% earnings related move. For those content with a 1% ROI for a trade that may last a week or less, a price move of less than 15% lower could fulfill that objective.

Twitter reports its first earnings since its IPO this week.

That thought should be enough to convince people to stay away from shares even had it not had such a surge in share price since a shaky start. Last week it held onto F��acebook’s earnings coattails and rose even higher. This week as it faces its first real scrutiny and potential pressure on shares, the options market is implying a 15.8% move in either direction. Again, for those content with a 1% ROI a strike price 22% below Friday’s close can deliver the reward. With at least one good support level and a couple of additional minor ones below that, the risk appears attenuated enough for at least consideration. That is until the next real challenge in mid-February when the first lock-up period comes to an end.

Finally, what’s a week without owning shares of eBay (EBAY)? After announcing earnings the week before last which were widely expected to be disappointing came the announcement from eBay itself that Carl Icahn had taken a position and was putting forward some ideas. The initial reaction was to propel shares toward the high point of its trading range, but eBay CEO Donahoe was quick to dismiss the idea of separating the PayPal unit from eBay and he seemed to have convinced the world that Icahn offered nothing new. He also convinced the world to give back the knee jerk gains.

While shares fared reasonably well this past week they are back in the range that I like to consider ownership, albeit at the upper end of that range. However, eBay, for all of the reasons people have disparaged its ownership has consistently been an excellent covered option purchase and wouldn’t be expected to melt under the pressure of a market at siege.

In the absence of any market moving international news particularly in the currency or debt markets I don’t expect much in the way of increasing volatility this coming week, but I wouldn’t mind the opportunity to party� like it’s 2011.

Traditional Stocks: eBay, EMC, Mondelez, Transocean

Momentum Stocks: Joy Global, Las Vegas Sands

Double Dip Dividend: Apple (ex-div 2/6), Starbucks (ex-div 2/4)

Premiums Enhanced by Earnings: Green Mountain Coffee Roasters (2/5 PM), Twitter (2/5 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.